Financial market report for the week ending June 28, 2013

1) … Introduction

With the rise in the Interest Rate On The US Ten Year Treasury Note …. Democratic nation state governance and its monetary policy of stimulus and easing is failing … In God’s Economy, Ephesians, 1:10, Daniel 2:25, Revelation 13:1-4, new regional governance and its economic policy of diktat as well as schemes of debt servitude are rising to rule mankind

1A) …The jump in the Interest Rate on the US Ten Year Note to 2.01% on May 24, 2013, constituted an “extinction event”, terminating nation state governance as well as investment choice. The rise in the Interest Rate on the US Government Note, ^TNX, has been so fast, and the steepening of the 10 30 US Sovereign Debt Yield Curve, $TNX:$TYX, has been so vertical, that credit and money literally died instantaneously. Fiat money is now longer trustworthy. People will increasing be placing their confidence in diktat money.

Specifically stated, the jump on the Interest Rate on the US Ten Year Note to 2.01% on May 24, 2013, constituted an “extinction event”, that is a cataclysm, which literally destroyed the investment choice offered by bankers as the way of life, and terminated the paradigm of Liberalism. Jesus Christ is operating at the helm of the Economy of God, Ephesians 1:10, and has pivoting the world into Authoritarianism, where the diktat of nannycrats is the way of life. Fiat money died, and diktat money has been coming to life.

Extinction Protocol tweets earthchanges news and geological events enroute to the New Earth foretold by prophets, sages, and scriptures. And I, in similar vain, as a Dispensational Economist, one who believes in Dispensational Economics, and being a Reformed Christian, that is one who has the like precious faith of the Apostles of Jesus Christ, believe that the “mass extinction of investors” commenced on the failure of Credit, AGG, and Major Currencies, DBV, and Emerging Market Currencies, CEW, in May 2013. Debasement of the Dollar by the US Central Banks has finally turned all “money good” investments bad, as is seen in M2 Money Weekly Not Seasonally Adjusted WM2NS failing on 04-15-2013, when it turned lower from 10681.4, to 10571.8 on 04-22-2013.

The world has pivoted from inflationism to destructionism, as Jesus Christ has now fully unleashed the Four Horsemen of the Apocalypse presented in Revelation 6:1-8, who will within ten years totally terminate all existing economic and political life as it currently is known, as the Rider on the White Horse is transferring sovereignty from democratic nation states to regional governance, the Rider on the Red Horse is increasing violence, the Rider on the Black Horse is increasing famine and economic death, and the Rider on the Pale Green Horse is increasing chaos. As a result, people no longer exist as residents of nation states, but rather as debt serfs under the authority of regional governance, totalitarian collectivism, debt servitude and austerity, as the Beast Regime of Revelation 13:1-4, rises in power to replace the Banker Regime.

I am not being a date setter, but believe that within fourteen years, the world will see the Advent of Jesus Christ, which will a global ecological cataclysm, which will end all existing physical and plant life processes on planet earth, as Jesus Christ returns to set up His Millennial Kingdom, where he reigns globally in glory, peace, and abundance, for a thousand years, from His Temple in Jerusalem, Revelation 20:1-6.

Libealism’s monetary policies of stimulus and easing were Banker regime schemes of the bygone era of inflationism. Nick Beams writes in WSWS Share selloff points to new crisis. Since the global financial crisis erupted in 2008, central banks around the world, with the US Fed leading the way, are estimated to have shovelled at least $10 trillion into financial markets. The initial assistance took the form of bailouts. Now it is being delivered in the form of quantitative easing, in which hundreds of billions of dollars at ultra-cheap rates is made available to banks and finance houses through central bank purchases of bonds. The official rationale for this policy is that purchasing bonds and driving down the yields on the safest financial assets will eventually lead to greater risk-taking by investors, including the injection of money into the real economy. That has not taken place. Rather, quantitative easing has promoted unprecedented financial speculation, leading to a situation in which share markets have risen sharply while the real economy has either grown very slowly, stagnated or contracted.

In contrast to Liberalism’s monetary policies, Authoritarianism’s policies of economic regional governance are the Beast’s regime schemes of today’s era of destructionism.

With that as a premise, there is an ever increasing integration of banks, government, industry, commerce and trade, establishing statist private partnerships in new governance, which will be working in mandates of nannycrats for regional security, stability and sustainability.

In the North American continent, governance, providing economic policy of diktat, will be called the North American Union, that is the NAU, or what I call CanMexAmerica, that being the amalgamation of Canada, Mexico, and the United States of America.

In Europe, governance will be what some call the EU Superstate, or what Angela Merkel has called the New Europe, or what Robert Wenzel of Economic Policy Journal once termed the One Euro Government.

The Economy of God, Ephesians 1:10, is powered by the many grand economic promises of God. The Apostle John presents God’s promised dynamo of regionalism, which replaces crony capitalism, European Socialsm and Greek Socialism, in Revelation 17:12.; Jesus Christ, God’s agent of economy, is bringing forth ten regional kingdoms: “The ten horns of the beast are ten kings who have not yet risen to power. They will be appointed to their kingdoms for one brief moment to reign with the beast.”

1B) … Greece is the beachead for the rise of the Beast Regime of Revelation 13:1-4. European Countries have participated in US Dollar Hegemony throughout the world, such as Iraq, Libya, Mali, and now in Jordan. Such coordination of power between the EU and the US, has been the fateful working of Bible Prophecy of Daniel 2:25-45.

God’s will for mankind is to experience Empire. God promised a succession of empires which is seen in the Statue of Empire dream given to King Nebuchadnezzar in Daniel 2:25-45, where two kingdoms of iron rule will fall from preeminence, and a ten toed kingdom of regional governance will form to rule mankind, with toes of iron diktat and clay democracy.

This global system of regionalism has replace the interventionism of the two iron legs seen in the Statue, where the first iron leg was the British Empire, and the second iron leg is/was the US Dollar Hegemonic Empire, that commenced with the establishment of the US Fed in 1910 to 1913.

The very linchpin in the Economy of God, Ephesians, 1:10, is the nation of Greece, GREK, as the sovereign Lord God, has designed it and a collection of Mediterranean Sea states, known as the PIGS, for their profligacy, to be the beachhead for the rise of the Beast Regime of Revelation 13:1-4.

The National Bank of Greece, NBG, continued strongly lower, taking Greece, GREK, strongly lower as Zero Hedge reports Greek bonds plunge as ruling coalition partner pulls out, withdrawing ministers.

And FT reports IMF to suspend aid payments to Greece unless bailout hole plugged. And Robert Stevens of WSWS reports New Democracy and PASOK form new crisis-ridden government in Greece. A crisis-ridden Greek government, composed of New Democracy and PASOK, announced a new cabinet following the resignation of the Democratic Left from the coalition. PASOK, which implemented the first raft of austerity measures after taking power in October 2009, was almost wiped out as a political force in the last elections and is now polling at 6.5 percent in opinion polls. However, it will play a much more leading role than previously and acquire key ministerial positions for the first time in this coalition government. PASOK party leader Evangelos Venizelos becomes the new deputy prime minister, a position he held from June 2011 to March 2012. He will also be the foreign minister. PASOK’s Michalis Chrysochoidis becomes transport minister, while Yiannis Maniatis takes over as environment minister. The positions of administrative reform minister and health minister are taken by Kyriakos Mitsotakis and Adonis Georgiadis, both members of ND. Georgiadis was a former member of the far-right LAOS party who was expelled last year and defected to ND, after voting for the second austerity package in defiance of his party’s line. He recently downplayed the emergence of the fascist Golden Dawn, saying that “in the crisis some people become a little bit extremist.” The cabinet reshuffle also brings ND and PASOK, the two main parties of big business, closer. Venizelos commented, “there is no ground in our country anymore for small, party or personal options,” adding that “National interest comes before every party objective.” In nine ministries, ND and PASOK officials will work together to impose further austerity. Pantelis Kapsis, a former government spokesman under the technocratic government of Lucas Papademos (2011-2012), is to run a new ministry specifically charged with dissolving ERT and carrying out massive job losses.

The government is tasked with carrying out further attacks demanded by the troika (European Union, International Monetary Fund and European Central Bank), which will return to Athens next week to review the implementation of austerity policies. Mitsotakis’s first job is to confirm to the troika that 2,000 public sector sackings are in place, as well as moving 12,500 civil servants into a labour mobility scheme over the next few weeks. Without these measures, the troika will withhold the release of the next €8.1 billion tranche of the total loan agreement. Following the first cabinet meeting, Samaras said that accelerating the troika programme was now “more crucial than ever.” Referring to the ERT crisis and the resignation of DIMAR, Stournaras told reporters, “We have to make up for lost time.”

The Greek government is now led by the very parties of big business that were principally responsible for plunging millions of people into poverty, in the process losing the support of the majority of Greeks. In the last election, PASOK and ND were only able to win the support of 40 percent of those who voted.

Despite DIMAR’s departure, the government can still count on the party’s support as it forces through deeper austerity. On Tuesday, party leader Kouvelis said the “Democratic Left…will continue to support the European course of the country and the need to continue reforms in order for Greece to overcome the deep crisis.” Thus DIMAR will continue to play its role as a critical “left” prop of the government. It began life as a right-wing split off from Syriza, the main pseudo-left opposition party. DIMAR entered the government after winning 14 seats in last year’s election. Last October, Kouvelis made a candid statement about DIMAR’s role, saying that in the face of growing hostility to austerity, “If the country today faces heightened pressure, and we as a leftist party participating in the government receive a portion of this pressure, you can image what would have happened if we had not provided it after the second general elections.”

Syriza, which has served, in its own words, as the “loyal opposition” to the ND/PASOK/DIMAR government, has done nothing to oppose the government. Instead it has positioned itself ever further to the right in recent months, in the hope of joining a future government of “national salvation.”

Syriza was lauded in an op-ed piece June 23 in the New York Times, headed, “Only Syriza Can Save Greece” written by economists James K. Galbraith and Yanis Varoufakis.

The authors argued that the crisis over ERT could “take down the Greek government and bring the left-wing opposition to power.” However, they said, “This wouldn’t be a bad thing for Europe or the United States.” They wrote that if Syriza leader Alexis Tsipras becomes the next prime minister, “nothing vital would change for the United States. Syriza doesn’t intend to leave NATO or close American military bases.” The coalition government has routinely used the full force of the state to impose austerity, including breaking up workers’ strikes with riot police. The government is now utilising the Council of State’s order to reopen ERT as the means of removing the workers who have occupied its Athens headquarters. The aim is to establish a new broadcaster employing just 1,000 workers, about a third of the current workforce.

On June 21, the Finance Ministry demanded that the workers “evacuate the premises…to allow for the unhindered and immediate implementation of the Council of State’s decision.” In response, a statement from the ERT workers read, “We shall not stop the struggle unless all of ERT opens as if it did not close for even a day, without any layoffs, without the circumvention of labour rights.” It added, “Come and get us. The orders for the evacuation of the broadcaster building by those who are acting illegally are violating every meaning of constitutional law, who are afraid of democracy, who are afraid of legality, it is force for us to give up. It is force to bring us to our knees. It is force to intimidate us.” While the workers are fighting defiantly to defend their jobs and livelihoods, the trade unions are once again ready to work with the government in pushing through the required austerity. Panagiotis Kalfagiannis, the leader of the broadcast workers’ union Pospert, supported the position of DIMAR and PASOK saying, “If the government wants to restructure ERT we agree. We want restructuring. Not a padlocked ERT.”

And Ambrose Evans Pritchard communicates that the EU has become a diktat union imprisoning the periphery PIIGS in a debt union by mandaiting bailins and by bearing the onerous burden of bank recapitalization stating, Another shameful day for Europe as EMU creditor states betray the south; the Cyprus “template” for banking crises is to be eurozone policy for other countries after all..

It is clearly evident that during the week ending June 22, 2013, God’s word of prophecy of Revelation 13:1-4, is being fulfilled, as the political governance and economic viability of Greece has collapsed.

Greece is a failed democratic nation state and has no national sovereignty to obtain seigniorage for its fiscal needs; it is a beggar nation receiving seigniorage aid from northern EU lords. It is a client state of Eurozone regional governance headed by nannycrats in the Brussels and Berlin. Those living in Greece are debt serfs, living in Euro debt land.

AP reports Greece vows faster reforms after political crisis. Greek Prime Minister Antonis Samaras promised Tuesday to speed up austerity reforms a day after being forced to reshuffle his cabinet due to a political crisis triggered by the closure of state broadcaster ERT. Samaras’ year-old coalition government narrowly avoided collapse after he ordered the sudden closure of ERT on June 11, firing all 2,656 employees. Greece has promised to axe 15,000 public sector jobs by the end of next year as part of cuts demanded by bailout creditors, the IMF, and other euro countries. Apart from the ERT crisis, Samaras is faced with a host of acute problems including shortages in health care and staggering unemployment, which has topped 27 percent. Socialist party leader Evangelos Venizelos, who led tough financial negotiations with Greece’s creditors during his term as finance minister in 2011 but who has seen his party’s popularity plummet, was named deputy prime minister and foreign minister. New ministers were also appointed for the posts of justice, administrative reform, transport and defense, among others, while Finance Minister Yannis Stournaras remained in the position.

Credit was a way of life under Liberalism, but now as is seen in the above AP report, under Authoritarianism, debt servitude is the way of life.

According to God’s Providence, Greece is rapidly leading the way forward in regionalization, where a EU Federal Superstate will be the example and standard for regional governance, totalitarian collectivism, and debt servitude.

EU ‘competitiveness’ is rapidly privatising public services and downgrading the democratic rights of citizens, argues Martin Konecny a researcher at the Corporate Europe Observatory campaign group, who relates in Worthy News, Authoritarian EU’ privatising states and attacking democracy. The June European council will see further debates on Europe’s competitiveness. Prominent among the different proposals is the idea of a so -called competitiveness pact. The plan of the European Commission, big business and of the German government in particular is to establish a set of ‘contracts’ for member states that will impel them to weaken labour laws, and to implement business-friendly legislation to promote competitiveness.

With support and encouragement from the business world, Merkel recently issued a joint statement together with Hollande where they set the timeframe for the final design of the competitiveness pact for the end of this year. But why is it that political and economic elites are pushing for such a deal? A political programme to undermine democracy in a very serious way, even while the formal institutions stay intact. To force every member state into contracts with the commission in such important policy areas as the labour market, in reality means to extend the kind of rule-by-Troika from the crisis-hit south to the rest of Europe. The undemocratic commission, or more precisely its neoliberal vanguard represented by Oli Rehn and his DG-ECFIN, (the Eurozone Finance Ministers) will decide, together with national executives, on the political and economic course of each country.

National parliaments will be sidelined and reduced to the function of rubber stamp legitimising, not coincidentally, a word used more and more often to depict the future role of national parliaments in debates at the European Council. The European competitiveness agenda has become a key tool to undermine democracy. Competitiveness becomes a value in itself for which we have to sacrifice basic democratic rights if, as is the commission tells us, we ever want to see jobs again.

The question of being able to democratically decide what kind of society we want to live in vanishes while the technocratic, in reality, highly political, rule of competitiveness takes its place. Instead of politicians, citizens are degraded to shareholders who can elect the best management of the competitiveness agenda decided on the European level. It seems that to political and economic elites, the main obstacle to the competitiveness agenda is increasingly seen as democracy itself.

1C) … Democratic nation state governance and its monetary policy of stimulus and quantative easing is failing … new regional governance and statist economic policies to rule mankind. Demcratic governance no more! New governance is coming in the form of regional governance. First, to provide the new policy of diktat and secondly to provide new debt servitude schemes, such as where the Fed encourages banks to place their resources into excesss reserves at the Fed., and where the Fed contracts with property management firms to actively manage and oversee the Fed’s mortgage backed bonds, MBB, by strong-arming the debtors to make payment on the loans.

Liberalism provided the policy of investment choice consisting of credit schemes such as free trade agreements, financial deregulation, leveraged buyouts, and dollarization.

Authoritarianism provides the policy of diktat based upon debt servitude schemes, consisting of such things as regional framework agreements, bank deposits bailins, new taxes, privatizations, sale of a country’s central bank’s gold reserves, capital controls, austerity measures,

Beginning in 1931, with the rise of the Creature from Jekyll Island, that is the US Federal Reserve, society was governed by the policy of investment choice and credit schemes. But beginning in May 2013, with the rise in the Interest Rate on the US Ten Year Note, society is increasingly governed by the policy of diktat and schemes of debt servitude..

Please consider the severity of money breakdown that occurred in May 2013: fiat money died. Just like in a hard freeze, where a plant’s life element perishes with a quick and hard snap, so in financial life, the money’s life element has perished by a sharp rise in the Interest Rate on the US Ten Year Note, ^TNX, and has perished by a vertical rise in the 10 30 US Sovereign Debt Yield Curve, $TNX:$TYX. as is seen in the Steepner ETF, STPP, steepening vertically.

The element of financial life, that being credit, has perished. With Liberalism’s financial life element of credit dead, Authoritarianism’s life element of diktat is rising to rule mankind.

What Doug Noland terms the global government finance bubble, has popped, it has been this bubble, that has underwritten, and swelled financial asset bubbles worldwide. This popping of bubbles, is seen in the ongoing Yahoo Finance chart of closed end funds AWP, EIM, PFL, PTY, RCS and CSQ, where the most interest rate sensitive bubble has suffered the greatest explosion. When fiat money died, it exploded the most interest reate sensitive asset classes with the greatest gusto.

Please comprehend the desperate nature of financial system death that is taking place: the balance sheet of the US Federal Reserve is been stuffed with US Treasuries, TLT, and Mortgage Backed Bonds, MBB, and is largely based upon the most toxic of debt, that is the “assets” taken in under QE1, these are largely illiquid debts like those traded in Fidelity Mutual Fund FAGIX.

As opposed to the previous rounds of central bank actions featuring Global ZIRP, the next round of central bank actions will be something entirely new. Look for things such as capital controls, and central banks working together in un-dollar regional currency initiatives, such as regional commerce trading platforms, like that of the Hangzhou-based company Alibaba Group. Thor’s Hammer writes in Naked Capitalism “China is forming alliances, engaging in non-dollar denominated energy trade arrangements, and actively working to replace the US dollar as the world reserve currency.” And Thor’s Hammer goes on to relate “When the US loses its reserve currency status that will signal the end of its reign as the world’s only great power. The USA is dependent upon its ability to print dollars to sustain its worldwide imperial military system.”

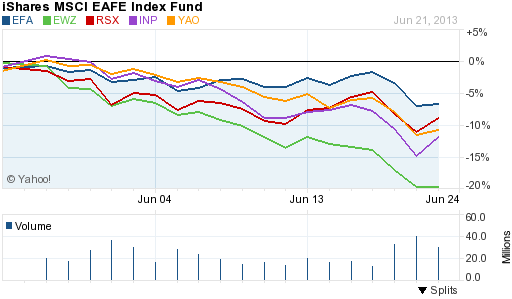

Global bond markets determine the fate of equity markets. The principle of debt deflation presents falling bond prices, which then cause currency sell-offs, and then stimulate derisking out of nation investment, and in particular financial institutions. This has been the case in the Emerging Markets, EEM, where Emerging Market Bonds, EMB, have plummeted on the sharp rise in the Interest Rate on the 10 Year Note, ^TNX, and then Emerging Market Currencies, CEW, have given way, and then, Nation Investment, EFA, in particular the banks of the countries under stress. A case in point is Brazil, where the Brazilian Real BZF, has fallen, driving Brazil, EWZ, EWZS, and its Banks, BRAF, lower, as is seen in the ongoing Yahoo Finance Chart of EFA, EWZ, RSX, INP, and YAO. Business Insider reports The Brazilian bond market massacre in one huge slide.

It’s the rapid pace of the rises on the Interest Rate on the US Treasury, ^TNX, from 1.75% on April 29, 2013, that is destroying stock values.

2) … Financial trading activity of week

2A) … Monday June 24, 2013

Robert Wenzel reports Bank Of China declares moratorium on transfers … Via Google translation, Customer service said, now silver futures transfer service has been fully suspended, online banking, the counter can not be handled, and now has the background system response, recovery time is not yet known. The ICBC bank system failure comes trouble “money shortage”, inevitably lead to speculation that many people guess the bank is not money. To solve this problem, ICBC relevant person in charge told reporters that morning, business process slow, the analysis on the host software upgrade, emergency treatment, 11:27 various businesses all returned to normal. As for speculation that the crash might be the last two days the inter-bank “money shortage” relevant, ICBC has denied. Shanghai Shenzen CSI 300 Index -6.3% today.

And Clement Tan of Reuters reports China shares suffer worst day in almost four years The CSI300 of the top listings plunged 6.2 percent; the Shanghai Composite Index, dived 5.2 percent as volumes spiked to the highest in about a month. Monday’s losses were their worst since August 31, 2009.

Commentary said the latest spike in money market rates was a result of market distortions caused by widespread speculative trading and shadow financing. The central bank, in its quarterly report on Sunday, pledged to “fine tune” existing “prudent” monetary policy. “I think the market is expecting ‘fine-tuning’ to mean a tightening of liquidity moving forward, especially after the way official media talked about shadow financing over the weekend,” said Cao Xuefeng, Chengdu-based head of research at Huaxi Securities. “People are quite jittery ahead of the first of two (PBOC) open-market operations for the week on Tuesday. In this market environment, it’s tough to call a bottom, fears could spread about funding for companies,” Cao added.

Banks hammered. Monday’s plunge came despite the overnight repo rate, a key measure of funding costs in China’s interbank market, falling by more than two percentage points to 6.64 percent on a weighted-average basis, its lowest since last Tuesday. It had peaked near 12 percent last Thursday.

Among the biggest losers were smaller banks seen as more reliant on short-term interbank funding. The Shanghai financial sub-index skidded 7.3 percent in its worst day since November 2008, during the financial crisis that started that year. Shanghai-listed China Minsheng Bank and Industrial Bank, along with Shenzhen-listed Ping An Bank all plunged by 10 percent. Minsheng’s Hong Kong listing skidded 8 percent in its worst day since October 2011. Minsheng shares, some of the most popular in both markets earlier this year, are now down 40 percent from a peak in January. They are down 19.4 percent on the year, compared to the 22 percent slide for the H-share index. Among the “Big Four” Chinese banks listed in Hong Kong, Agricultural Bank of China (AgBank) (1288.HK) and Industrial Bank of China (ICBC) (1398.HK) had the biggest percentage losses, 2.9 and 3 percent, respectively.

John Rubino reports During the night, emerging market stocks tanked again, led, ominously, by China. This morning the carnage has shifted to the US, where stocks are down hard but, more important, interest rates are still rising. 10-year Treasuries, the key to mortgage rates and pretty much everything else, now yield nearly twice what they did a year ago. That means massive losses for a whole world of risk-averse investors who thought they were parking their money in the safest-possible asset. Presumably the rest of their capital is in riskier places like stocks and junk bonds, which means they’re losing big across the board.

This is a global story, since Treasuries have been everyone’s safe haven of choice for decades. But painful as a 40% haircut for the world’s pension funds might be, it pales next to the impact on growth. US interest rates are, with a few notable exceptions like Japan, the base of the global yield curve. Everything else, being riskier, has to have a higher yield. So a doubling of US rates means a commensurate ratcheting up of everyone else’s rates.

Since equities are valued in part in relation to the yield on available bonds, rising interest rates mean lower stock prices, everywhere. And real estate, which is generally leveraged, has just gotten a lot more expensive (which means the other group obsessively staring at screens these days is the new generation of flippers who recently joined the Southern California and Florida bubbles). This is the nightmare scenario that keeps central bankers and institutional investors up at night because, based on Japan’s experience with hyper-aggressive monetary ease, there might not be a fix. If even easier money is met with dramatically higher bond yields, as in Japan, then there’s nothing left to do but to let the system unravel.

Market Watch reports China’s alarming credit crunch

Elaine Meinel Supkis writes Bond markets rocked by panic. The biggest part of the bond market trading is the ETF guys on Wall Street. Exchange traded funds which didn’t exist before 1993 and which is an elemental part of the Derivatives Beast’s operational system for lurching in various directions very suddenly Only authorized participants, which are large broker-dealers that have entered into agreements with the ETF’s distributor, actually buy or sell shares of an ETF directly from or to the ETF, and then only in creation units, which are large blocks of tens of thousands of ETF shares, usually exchanged in-kind with baskets of the underlying securities. Authorized participants may wish to invest in the ETF shares for the long-term, but they usually act as market makers on the open market, using their ability to exchange creation units with their underlying securities to provide liquidity of the ETF shares and help ensure that their intraday market price approximates to the net asset value of the underlying assets.[4] Other investors, such as individuals using a retail broker, trade ETF shares on this secondary market. These authorized creatures are mainly computers, not humans. The humans are lazy bastards. They hire geeky guys to write elaborate programs and then sit back and let the money pour into their bank accounts after firing the geeks.

Mike Mish Shedlock writes Curve Watchers Anonymous note the yield on the 10-year treasury note hit as high as 2.7% today, up a whopping 104 basis points since the early May low in yield of 1.6%.

Bespoke Investment Group reports 10-Year Yield most extended in 50 years. The yield on the 10-Year Treasury Note, ^TNX, has jumped another 13 basis points today up to 2.6%. This has pushed the 10-Year yield up to 33.3% above its 50-day moving average; this is the farthest the 10-Year yield has been above its 50-day in at least 50 years. Talk about extended! At what point does this see at least a short-term turnaround?

Well today, there is no turnaround in the 10-Year yield whatsoever; credit traded lower as follows:

EMB -1.7, UJB -1.6, JNK -1.1, MUB -0.9 and AGG -0.4 as CNBC reports Bond fund outflows hit record level on tapering fears.

Credit, that is trust in the ability of the debtor to repay the lender, no longer exists. And as a result investors are rapdily derisking out of finanical stocks, IXG, which in turn destorys nation investment, EFA.

With the seigniorage of democracies destroyed by higher treasury rates, their currencies are plummenting, and their sovereignty is waining. Said another way, failed seigniorage means failed sovereignty.

In apocalyptic vision, the Aposlte John, foretells in Revealtion 13:1-4, that out of a soon coming credit bust, global currency crisis, and world wide stock market meltdown, new sovereignty will emerge, that being the sovereignty of regional governance, as leaders meet in summits and workgoups to renounce national sovereignty, and announce pooled sovereignty.

With ever increasing power, regional nannycrats will rule in statist public private partnerships, mandating debt servitude schemes such as capital controls, new taxes and bank deposit bailins, as the former credit schemes of democratic states featuring financial deregulation, POMO, Quantitative Easing, and dollarization no longer work.

Lyrics Freak provides John The Revelator Lyrics. The Lord’s Apostle John foretold that the diktat money system is rising to replace the fiat money system, where today’s citizens of democratic countries, will be tomorrow’s residents of regional governance. God’s Apocalyptic Word written 2,000 years ago, rings clear in excellent tone today. God is calling, and only the elect understand and value His communication.

Credit is totally toxic, that which was once financial life’s element, is now a zombie, inducing investors to derisk out of stocks world wide; wealth overall traded as follows World Stocks, VT -2.1%, Nation Investment, EFA -1.6%, VGK -3.4%, as Zero Hedge Collapsing European imports crush current account recovery cravings, Emerging Markets, EEM -2.0%, Asia Excluding Japan, EPP -1.2%, and US Stocks VTI -1.7%, with Russell 2000, IWM, -1.3%, and the S&P 500, SPY, -1.3%.

With trust in fiat money eroded,the Emerging Market Financials, the Chinese Financials, and the European Financials are leading stocks lower. Financials traded lower as follows:

IXG -1.5 … EFA -1.6

EUFN -2.3 … VGK -3.4 … SF Gate EU faces renewed bond-market slump as bank talks sputter

CHIX -2.3 … ECNS -4.2

EMFN -1.3 … EEM -2.0

EPI -2.6 … SCIN -2.8

BRAF -1.4 … EWZ -2.0

RWW -1.2 … IWM -1.3

Nick Beams of WSWS reports Share selloff points to new crisis. The renewed turmoil on global financial markets underscores the fact that none of the problems that erupted in the 2008 meltdown have been overcome. I comment that the crack up boom that came via Global ZIRP, is over; countries traded lower as follows:

CAF -5.3

IDXJ -5.2

EPHE -4.3 Benton te reports the yields of 10 year Philippine bonds jumped 10 bps from 3.94 to 4.04 today, the same yields soared by 23 bps or 5.71%, details presented in chart from Investing.com and asks Will the BSP begin to raise rates or will they fight the bond vigilantes by conducting the domestic version of QE or do both ala Indonesia? Rioting local bond markets only contradicts the premises of the recent credit upgrades. Will the credit rating agencies the Fitch and the S&P reverse their position soon? As I have been saying, credit rating upgrades signify as the allegorical “kiss of death” or a “curse in disguise”. Oh by the way the crashing Philippine equity markets has been relentless. Today, the Phisix tumbled by another whopping 3.05% (chart from Technistock.com). Interesting times indeed. Nonetheless the gullible and vulnerable public whom has misread, and or has been deceived or brainwashed by what has been promoted and propagandized by the political spectrum and their media accomplices as “strong economic fundamentals” will soon be faced with harsh reality. They will realize that “strong economic fundamentals” is the metaphorical equivalent of the “emperor has no clothes” or a phony statistical economic boom that has been cosmetically spruced and pumped up by easy money policies via credit expansion. At the end of the day the lesson is: social policies that promotes quasi permanent booms eventually morphs into economic/financial busts. This time is no different.

ECNS, -4.1

EWHS -3.9

SCIN -2.8

EWSS -2.8

SCIN -2.8

KROO -2.6

THD -2.5

NKY -2.5

EWY -2.2 Business Week reports South Korean bonds extend biggest weekly slump as demand falls.

TUR -3.9

ARGT, -3.5

EWZ -2.0

EWW -1.9

EPU -2.0

ECH -1.5

The WSJ reports Bottom is falling out of copper prices. Copper’s world is coming apart. The price has fallen 16% so far this year and is 34% below February 2011’s all-time closing high. This isn’t just a case of slowing economic growth. The global forces propelling the metal’s stunning rise over the past decade are shifting. Copper’s supercycle is entering its downhill run

NORW, -3.6

EWD -3.3

EWO -3.2

EIRL -3.1

EFNL -3.0

EWP -2.1

EWQ -1.8

EWN -1.7

Mike Mish Shedlock writes Yields creep up in Spain, Italy, France (Actual and also relative to Germany). I comment that they be sovereigns no more, as debt deflation comes to the Euro currency nations. As the yields on Eurozone nation sovereign debt rises, nation investment in Germany, EWG, Italy EWI, Spain, EWP, France, EWQ, as well as Austria, EWO, Netherlands, EWN, and Finland, EFNL, tumbles, as is seen in the ongoing Yahoo Finance Chart of EWG, EWI, EWP, EWQ, EWO, EWN, EFNL. It is sovereignty that begets seigniroage, that is moneyness. The loss of seigniorage seen in the EU country ETFs trading lower, communciates a loss of sovereignty.

Sectors traded lower as follows:

COPX -5.2

SIL -4.6

GDX -4.6

KOL -3.9 US steelmaking coal manufactuer, Cliff Natural Resources, CLF, fell sharply as Bloomberg reports Steelmaking coal slides to four year low after Billiton deal. A key contract that determines prices of coal used in the $1.3 trillion market for steel slid to a four-year low amid a global supply glut. The coking-coal benchmark contract for the third quarter was settled at $145 a metric ton in quarterly negotiations between BHP Billiton Ltd., the world’s biggest coking coal exporter, and Nippon Steel & Sumitomo Metal Corp., Doyle Trading Consultants LLC said today in a report. That compares with $172 in the second quarter

CHIM -3.8

CHII, -3.7

PICK -3.5

BJK -3.2

PBD -2.9

REMX -2.0

XOP -1.6

XLI -1.6

Yield bearing sectors traded lower as follows:

DRW -5.6

ROOF -3.3

REM -2.7

DLS -5.1

DGS -3.5

SEA -3.7

DBU -3.0

Commodities traded lower as follows:

DBC -0.4

JJC, -2.2

SLV -2.1

DBB -1.7

GLD -0.9

JJA -0.8

2B) … Tuesday June 25, 2013

Reuters reports Stocks and bonds recover footing as liquidity fears ease. Market Watch reports China’s PBoC pledges to address the cash crunch. And Bloomberg reports PBOC Ling says rise in China money market rates temporary. China will keep money-market rates at a “reasonable” level and seasonal forces that have driven them up will fade, a People’s Bank of China official said. This as The WSJ reports China’s shadow banks fan debt bubble fears. In a 52-story office tower overlooking the leafy streets of this city’s embassy district, some 400 deal makers at Citic Trust Co. arrange financing for property developers, steel mills and other businesses starved for cash and shunned by China’s traditional banks. The lenders at Citic and other institutions that make up China’s “shadow banks” have created the closest thing China has to the culture of Wall Street. They take risks that traditional banks won’t, going so far as to create investment funds for assets like top-shelf liquor and mahogany furniture. Their top executives drive luxury cars and frequent expensive clubs. Now, China’s shadow banks, a mélange of trust companies, insurance firms, leasing companies, pawnbrokers and other informal lenders subject to limited oversight, are at the center of mounting concerns over whether the country’s slowing economy could trigger a debt crisis.

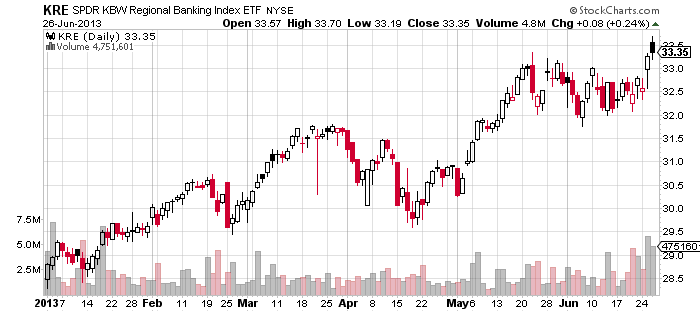

The safe haven in small cap stocks is Regional Banks,.KRE, as the ratio of these to the Russell 2000, KRE:IWM, is at rally highs; and likewise,the safe haven in large cap stocks is the Too Big To Fail Banks, RWW, as the ratio of these to the S&P 500, RWW:SPY, is at its rally high.

US Regional Banks, KRE, rose 2.1%, and The Too Big To Fail Banks, RWW, rose 1.5, drawmg World Stock VT, 1.0% higher

Yield bearing stocks rose as follows

DRW 2.7

REZ 2.0

REM 1.9

IYR 1.8

ROOF 1.5

Sectors rose as follows

KRE 2.1

BJK 2.0

SMH 2.0

KCE 1.8

CSD 1.6

FLM 1.5

PKB 1.5

PBD 1.5

PSP 1.5

IBB 1.5

In news of regional governance, Reuters Exclusive reports China Mobile, Etisalat weighing bids for PakistanTelco. Pakistan mobile operator Warid Telecom has been put up for sale by its Abu Dhabi owners and is likely to draw interest from China Mobile and Etisalat, sources familiar with the matter said on Tuesday.

Bloomberg reports Berlusconi’s sex conviction raises tension in Letta’s government. Italian Prime Minister Enrico Letta is facing discord among parliamentary supporters after his coalition partner, Silvio Berlusconi, was convicted of paying a minor for sex and sentenced to seven years in prison. The verdict, announced yesterday by Judge Giulia Turri in Milan, was criticized by Deputy Prime Minister Angelino Alfano and Renato Brunetta, chief whip of the second-biggest party in the lower house of parliament. Letta’s own Democratic Party said it would respect the judge’s decision. Berlusconi, a 76-year-old billionaire and former premier, has said he is innocent and remains free as he prepares his appeal

Heesun Wee of CNBC reports The best and the worst American cities for small business workers. CardHub, a website for credit card, financial and jobs advice, has released a new ranking of the best and the worst American cities for small-business workers and job seekers.

Denver, Boston, Minneapolis, Seattle, and San Francisco are rated the best cities for small business workers.

Denver: The Mile High City tops the list in part because it has a high concentration of smaller employers. About 97 percent of Colorado employers are classified as small businesses, according to CardHub’s study. Denver’s workforce is also growing at the second-fastest rate in the country, and ranks fifth for highest wages for new earners.

Detroit and Riverside are rated the worst cities for small business workers.

Detroit: Bailouts helped prop up the Motor City. But Detroit’s small-business community continues to be hit by one of the lowest number of small businesses per capita-22 among the study’s list of 30 cities. Detroit’s net small-business job growth came in at 27 out of 30; and 26 out of 30 for industry variety.

Riverside: This Southern California community experienced a massive run-up and collapse in housing prices over the past several years. Among the 30 cities CardHub evaluated, Riverside ranked last in terms of number of small businesses per capita, small-business vitality and unemployment rate.

New small-business hires make the most money in Washington, D.C., San Francisco, and New York, where cost of living is high, according to the study. New earners make the least in Riverside, Sacramento, St. Louis-all in the bottom half for cost of living.

The opportunity to make new commerical real estate deals is now greatly diminished as is seen in the ongoing Yahoo Finance Chart of Commercial Office REITS, FNIO, Mortgage REITS, REM, and Small Cap Real Estate, ROOF. Bloomberg reports Wall Street’s $8 billion CMBS in limbo as bulls retreat. Wall Street firms spent the past six months increasing commercial mortgage origination as investors bought the most debt in six years. That’s now backfiring as banks prepare to market $7.5 billion of loans earmarked to be sold as bonds before credit markets took a dive this month. Investors demanded 1.03 percentage point more than the benchmark swap rate to buy new commercial mortgage backed securities tied to shopping malls, skyscrapers, hotels and apartment buildings on June 14, according to data compiled by Bloomberg. That’s up from 72 basis points in February, the narrowest spread since sales revived in 2009, the data show. Lenders’ profits are eroded when values of the securities fall. The CMBS market is poised for its worst month in almost two years after the Federal Reserve signaled it may curb stimulus efforts as the economy shows sign of improvement. That’s complicating efforts by banks to sell new deals and making it more expensive for landlords to refinance loans backed by everything from Manhattan office space to suburban grocery stores.

Ambrose Evans Pritchard reports Italy could need EU rescue within six months, warns Mediobanca. Italy is likely to need an EU rescue within six months as the country slides into deeper economic crisis and a credit crunch spreads to large companies, a top Italian bank has warned privately. Mediobanca, Italy’s second biggest bank, said its “index of solvency risk” for Italy was already flashing warning signs as the worldwide bond rout continued into a second week, pushing up borrowing costs. “Time is running out fast,” said Mediobanca’s top analyst, Antonio Guglielmi, in a confidential client note. “The Italian macro situation has not improved over the last quarter, rather the contrary. Some 160 large corporates in Italy are now in special crisis administration.” The report warned that Italy will “inevitably end up in an EU bail-out request” over the next six months, unless it can count on low borrowing costs and a broader recovery. Emphasising the gravity of the situation, it compared the crisis with when the country was blown out of the Exchange Rate Mechanism in 1992 despite drastic austerity measures.

Debt deflation, that is currency deflation, has come to China, as Bloomberg reports Yuan declines for fifth day on concern over China’s growth. China’s yuan declined for a fifth day on concerns the worst cash crunch in a decade will worsen a slowing economy. I comment that the chart of the Chinese Yuan, CYB, shows a definite downturn. Mike Mish Shedlock writes China’s credit bubble has popped, and growth going forward will plunge as China rebalances. I comment that nation investment in China is tumbling as is seen in the ongoing Yahoo Finance Chart … http://tinyurl.com/o74b7bx … of Shanghai, CAF, China Industrials, CHII, China Real Estate, TAO, China Financials, CHIX, China Small Caps, ECNS, and China, YAO.

US steelmaking coal manufactuer, Cliff Natural Resources, CLF, fell sharply as Bloomberg reports Steelmaking coal slides to four year low after Billiton deal. A key contract that determines prices of coal used in the $1.3 trillion market for steel slid to a four-year low amid a global supply glut. The coking-coal benchmark contract for the third quarter was settled at $145 a metric ton in quarterly negotiations between BHP Billiton Ltd., the world’s biggest coking coal exporter, and Nippon Steel & Sumitomo Metal Corp., Doyle Trading Consultants LLC said today in a report. That compares with $172 in the second quarter

Ethics is defined as economic regard for the property and person of another. This morning at 5:00 AM, I came across a woman laying on the apartment lobby floor. So I went over and gently pressed my toe against her calf and she stirred; she spoke coherently, saying she was resting there; so in spiritual economic regard, I told encouraged her to rest. Another person, one of more carnal regard, came along and helped her get up and go down the hall way into her room; and locked her in and left. I do not intervene in the life of others, as whatever economics they have comes from God, and I do not want to and will not be a busy body in another person’s affairs.

2C) … Wednesday June 26, 2013

Both Aggregate Credit, AGG, and World Stocks, VT, rose, vertically, after having fallen vertically.

Market Watch reports Most Asian stocks rise as Shanghai falls again. And Market Watch reports European stocks climb for second straight day. Benton te writes Phisix stages monster rally as Philippine bonds tank Philippine asset markets today can be described as the strange case of Dr. Jekyll and Mr Hyde. That’s because the domestic bond and the stock market went in opposite ways. This post-trading report from the Wall Street Journal has been a lot less sanguine about today’s “biggest gain since 2008″. Nonetheless, expert sentiments appear as in denial about the true grizzly nature of bear markets.

There is one single force that will prove to be a key obstacle to any real recovery of Phisix: this is if the drubbing of the domestic bond market continues. Today 10 year yields surged by another 11 bps or 2.57% (chart from investing.com). This is the 3rd day for the sharp climb which nears 50 bps.

It would be a mistake for some to think that this represents a sign of “shifting” (from bonds to stocks). There are really no “flows” on the financial markets. For every buyer there is a seller. For every transaction, cash transfers from buyer to the seller in exchange for securities. What drives prices is the aggressiveness of either the buyer or the seller. Today’s actions means that stock market bulls aggressively bid up the stock markets, while bond vigilantes continue to harass the Philippine bond markets regardless of the reasons behind them. Again a sustained rise in yields will eventually force the BSP’s hand to raise rates, as explained yesterday. And higher rates amidst rapidly growing of systemic leverage only increases credit risks. The Dr. Jekyll and Mr Hyde syndrome hasn’t been a Philippine only characteristic. As of this writing Indonesia’s equity bellwether the JCI has been significantly up even as 10 year bond yields today soared by 31 bps or 4.42%

I comment that the Finviz chart of the Philippines, EPHE, shows a vertical rise, after having fallen vertically. We are witnessing a “sew saw” destruction of fiat wealth, credit investments, equity investments and currencies are literally being sawed asunder, as credit, that is trust, dissipates on the rise of the Interest Rate on the US Ten Year Note, ^TNX.

Reuters reports Stocks advanced for a second straight day on Wednesday as GDP was revised down. World Stocks, VT, traded 0.9% higher. Gold Mining Stocks, GDX, GDXJ, and Silver Mining Stocks, SIL, SILJ, SSRI, traded lower as is seen in their ongoing Yahoo Finance Chart. Silver Standard Resources, SSRI, which likely as been the most heavily carry traded stocks of all time, lost 4.5%, HL lost 6.6%, and SLW, 7.7%. Talking Numbers writes This metal is worse than gold. Silver investors are feeling the pain more than gold investors. With the metal falling is there a silver lining? Silver, SLV, fell 5.5%, and Gold, GLD, fell 4.2%. Spot Gold, $GOLD, closed at 1,225.

Sectors trading higher included

IBB 3.0

PJP 1.8

PDB 1.7

BJK 1.7

PPA 1.5

PJP 1,.4

IGV 1.3

IXG 1.2

FDN 1.1

SMH 0.7

IBB 0.7

RWW 0.7 and KRE 0.6, and includes GBCI, FMER, PBCT, and ZION

Yield bearing sectors trading higher included

AMJ 3.7

EMLP 1.8

DGS 1.8

EDIV 1.0

DRW 1.7

FNIO 1.6

XLU 1.6

Countries trading higher included

EPHE 6.8

IDX 6.0

THD 4.2

TUR 3.6

EWZS 3.2

EWW 2.7

ECH 2.6

EWW 2.5

EZA 2.4

ENZL 2.4

EWP 2.0

YAO 1.8

ECNS 1.7

India Small Caps, SCIN, traded lower on a strongly lower India Rupe, ICN, and IBT reports India’s RBI restricts lending against gold.

Action Forex shows the chart of the Euro Yen Currency Carry Trade, that is the EUR/JPY, seen also as FXE:FXY, with close at 127.44. The Finviz chart of the Euro, FXE, shows a close lower at 128.86. The Stockcharts.com chart of the US Dollar, $USD, shows a close at 82.85; just above $82.50, its 50 day moving averge. The US Dollar is trading in the middle of a broadening top pattern, which is best seen in the Finviz chart of its 200% ETF, UUP; it’s as Street Authority relates, when you see the broadening top the market wll eventually drop.

When the Bretton Woods system, synomous with the Milton Friedman Free To Choose floating currency system, really gives way, America’s Dollar Empire, that is the US Dollar Hegemonic Empire, and its globe-spanning archipelago of mililtary bases, will collapse, and the Ten Toed Kingdom of Regional Governance of Daniel 2:25-45, will emerge, where ten regional zones of increasing iron diktat will emerge out of today’s clay democracy. The additional bible prophecy of Revelation 13:1-4 presents the ten zones of regional governance, as ten horns on a beast, that also has seven heads, suggesting totalitarian collectivism. The seven heads symbolize mankind’s seven institutions: 1) Education, 2) Finance, Commerce and Trade, 3) Body Politic, 4) Military, 5) Religion, 6) Media, 7) Science and Technology.

In regimes, policies and schemes govern to establish and define life until terminated by an “extinction event”. When a person is born again, he becomes a New Person in Christ, and comes to have life in Christ, which can never be extinguished, yet Christians are nevertheless influenced by “extinction events”, which include the Advent of Christ, as an example, which will terminate the Beasts regime’s rule, as well as terminate all plant and animal life on planet earth, as well as all physical processes, as presently known.

The rise of the Interest Rate on the US Ten Year Note, ^TNX, to 2.01% on May 24, 2013, was an “extinction event” that terminated Liberalism’s age of investment choice and commenced Authoritarianism’s age of diktat. The word economy is defined as the household administration of things physical, spiritual, philosophical, monetary, and political. The Apostle Paul communicates in Ephesians 1:10, that Jesus Christ is at the helm of the Economy of God. He being sovereign in all things, terminated the Banker regime and commenced the Beast regime. God desires that Christ be one’s all inclusive life experience, Colossians 3:11.

The fiat, those of religious and philosophical ideology, pursue will worship, Colossians 2:23, that is they worship their own will, and have identity and experience in the mandates of their ideology. In contrast, the elect, those of God’s choosing, pursue God’s will, and have identity and experience in Christ.

Liberalism’s policies and schemes ended May 24, 2013, and Authoritarianism’s policies and schemes commenced when the Interest Rate on the US Ten Year Note, ^TNX, rose to 2.01%.

Please consider the Dispensation Economics Manifest concept that the Fed is dead; an organism, having no life, that is no vitality; and as such has no authority or power. The US Federal Reserve, and other central banks, and their agents, that is investment institutions, IXG, such as the Too Big To Fail Banks, RWW, BAC, C, Asset Managers, BLK, Investment Bankers, KCE, JPM, Stockbrokers, IAI, TROW, Regional Banks, KRE, GBCI, European Financials, EUFN, SAN, Far East Financials, FEFN, NMR, Emerging Market Financials, EMFN, ITUB, Chinese Financials, CHIX, SHG, are the Banker regime’s monetary institutions, put in the grave by the failure of Credit, AGG, with the bond vigilantes calling the Interest Rate on the 10 Year Note, TNX, higher. to 2.01% on May 24, 2013. These institutions are seen as tombstones in Liberalism’s graveyard, as one looks in one’s rear view mirror. The Fed is as dead as dead can be, terminated by the “extinction event” of the rise in ^TNX.

Now, regional governance institutions, such as the European Finance Ministers, the IMF, and the Troika, are the enlivened monetary authorities of the Beast regime. The “extinction event” of the rise in the Interest Rate on the US Ten Year Note, ^TNX, terminated all of the authority of Liberalism’s policies and schemes, thereby ending Liberalism’s life experience. Now, Authoritarianism’s policies and schemes, have authority, and ever increaing power, providing monetary and political life experience.

Through the Economy of God, that is the household administration of all things, for the completion of every age, epoch, era, and time period, Ephesians 1:10, Jesus Christ, is powering up Authoritarianism’s dynamo of regionalism, which replaces crony capitalism, European Socialism and Greek Socialism, as foretold in Revelation 17:12. He is bring forth ten reigonal kingdoms: “The ten horns of the beast are ten kings who have not yet risen to power. They will be appointed to their kingdoms for one brief moment to reign with the beast.”

Yes, yes, yes, The Fed is dead. Jesus Christ did what Ron Paul could not do, He ended the Fed. He slayed it by turning the bond vigilantes and the currency traders loose on the markets. But wait a New Monster is replacing it. While the Free To Choose Monster is indeed history, the Regional Governance and Totalitarian Collectivism Monster is coming as the North American Union, or what I call Can Mex America, a Continental Behemoth featuring totalitarian collectivism integrating mankind’s seven institutions: 1) Education, 2) Finance, Commerce and Trade, 3) Body Politic, 4) Military, 5) Religion, 6) Media, 7) Science and Technology. Public private partnerships will oversee the factors of production and manage commerce and trade.

Robert Wenzel of Economic Policy Journal writes Crony Rahmaland billionaire Queen joins Obama Cabinet. The Senate has confirmed Chicago-based billionaire Penny Pritzker as new Commerce Secretary. She was an early and important source of money in Obama’s first presidential campaign. Pritzker is also on the Board of Directors of the Council on Foreign Relations. She serves as trustee of Stanford University. She’s an advisory board member of Robert Rubin’s Brookings Institution’s Hamilton Project. This, folks, is a major insider. Forbes lists her wealth at $1.7 billion. Her father co-founded the Hyatt Hotel chain. She apparently is of the view that only little people pay taxes. NyTi: reports: Pritzker’s family is renowned for finding ways to avoid paying taxes on its wealth. The Pritzkers were pioneers in using tax loopholes to shelter their holdings from the Internal Revenue Service. Nothing wrong with tax loopholes. Mises, afterall, pointed out that capitalism breathes through loopholes, but don’t expect Pritzker spending time at Cabinet meetings advocating tax loopholes for “the little people.” The confirmation vote was 97-1, with only Senator Bernie Sanders voting against.

2D) … Thursday June 27, 2013

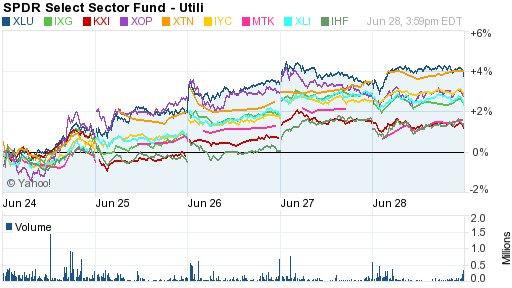

World Stocks, VT, rose 1.0%, US Stocks VTI, 0.8% and European Stocks VGK, 0.7%, on a rally in the current bear market; sectors rising included,

ITB 2.4

PKB 1.9

IGV 1.7

PBD 1.7

PSCI 1.6

PPA 1.5

IGN 1.4

RXI 1.3

PSP 1.1

Yield bearing real estate rising included

ROOF 2.7

FNIO 2.4

REZ 1.9

IYR 1.7

REM 1.7

DRW 1.3

Other yield bearing sectors rising included

AMJ 2.2

SEA 1.3

DGS 1.3

IST 1.2

DLS 1.1

Financials rising included

IXG 1.6

KRE 1.6

RWW 1.3

EUFN 1.4

EMFN 1.4

Jason Ditz of Antiwar reports Federal Judge throws out Abu Ghraib torture lawsuit. US District Court Judge Gerald Bruce Lee has thrown out the lawsuit brought by four Iraqi torture victims against CACI International, the company that tortured them, saying the US courts lacked jurisdiction over the matter. Lee went on to reject the notion of lawsuits based on things that happened during the US occupation of Iraq in general, saying that there was “inconclusive” evidence to conclude that the US had “de facto sovereignty.”

Mike Mish Shedlock posts the Dr Eric Dor, Directeur IESEG School of Management, Université Catholique de Lille report The consequences of monetary union on the destruction of French manufacturing industry, stating the Euro has been more like an anchor to most of the economies in the eurozone. I tried to open the PDF, but could not.

Under the Euro, Germany, that is the north, exercised ingenuity, discipline, and conservative economics, such as resistance to anticompetitiveness practices, insistence on low unit labor costs, rejection of clientelism, as well as municipal indebtedness, and cajas indebtedness, which established Germany as a manufacturing superpower and generated the enormous TARGET related claim of the Bundesbank on the rest of the Eurosystem. Said another way Germany pursued crony capitalism, while France and the periphery South pursued European Socialism, and Greek Socialism, which featured Club Med, undisciplined, libertine, and taxation resistant, liberal economics.

The Euro currency union was fathered, that is created, by the CIA, Wall Street Investment Bankers, and the Council on Foreign Relations, CFR, community, to create a strong NATO, as well as to create a sovereign debt investment carry trade opportunity, profiting from the decline in southern, that is PIIGS, Treasury Debt Interest Rates, as the Euro was introduced.

Now out of periphery sovereign insolvency of Greece, GREK, and Spain, EWP, and banking insolvency, National Bank of Greece, NBG, Banco Santander, SAN, as well as the European Financials, EUFN, a global credit bust, currency crisis, and worldwide financial system breakdown, as prophecied in Revelation 13:3-4, is imminent.

The Beast regime, of Revelation 13:1-4, is already rising out of a rise in Interest Rate on the US Ten Year Treasury Note, ^TNX, and soon will make its beachhead out of the periphery, that is south, profligacy.

The development and use of the Euro, FXE, exasperated the north south divide, to become a nordic latin chasm. The periphery, that is south, will revolve as hollow moons, about planet Berlin and planet Brussels. While the Greeks, the Spanish, and the French, cannot be Germans, all will be one, living in debt servitude in a diktat union, specifically a debt union, a fiscal union, and a banking union, as leaders meet in summits and workgroups, to renounce national sovereignty, and announce pooled sovereignty for regional security, stability and sustainability, where nannycrats call out Authoritarian policy and Authoritarian schemes, establishing regional governance and totalitarian collectivism, in a One Euro Government, that is in a Federal Eurozone Super State.

Choice and credit was the basis of Liberalism. But diktat and debt servitude is the basis of Authoritarianism all of mankind’s seven institutions 1) Education, 2) Finance, Commerce and Trade, 3) Body Politic, 4) Military, 5) Religion, 6) Media, 7) Science and Technology, are integrated into one. The WSJ reports China cash crunch spreads. Businesses Turn to Alternatives Such as Bankers’ Acceptances to Pay Their Bills. Even as Chinese officials indicate a softening of their tight grip on cash, some businesses are reporting liquidity is increasingly hard to find in some places and that customers are turning to alternatives. It isn’t clear how deep the liquidity issues have trickled down from the financial sector, which has been gripped this month by a cash crunch widely believed to be aimed at deflating ballooning credit in the Chinese economy. But it suggests the pain could spread to other areas if cash borrowing rates for banks remain stubbornly high. Over the past couple of weeks companies have increasingly used bankers’ acceptances, a type of short-term guarantee issued by banks to finance trade, to pay their bills instead of cash, according to people in a range of industries around the country.

2E) ,… Friday June 28, 2013

This week Aggregate Credit, AGG, and US Goverment Bonds, GOVT, rose weakly, as the Interest Rate on the US Ten Year Note, ^TNX, traded slightly lower to 2.48% from 2.51%, and the 10 30 US Sovereign Debt Yield Curve, $TNX:$TYX, flattened somewhat as is seen in the Steepner ETF, STPP, flattening slightly

Of note, Gold Miners, GDX, and Silver Miners, SIL, rose for the second day, despite, Gold, GLD, and Silver, SLV, traded higher. Gold Mining Stocks, such as AUY, had fallen 60% since October 2012; AUY, rose 8% on the day. The chart of Spot Gold, $GOLD, closed the week at $1,232.

For the day, and for the week

World Stocks, VT, -4. and +1.1

US Stocks, VTI -.5 and +0.9

Asia Excluding Japan, EPP -1.4 and +1.6

Europe, VGK, -.6 and +0.3.

Nikkei, NKY, 1.2 and +1.2

Emerging Markets, EEM 4.2

Mexico, EWW 9.8

South Africa, EZA 6.8

Philippines, EPHE, 6.5

Taiwan, EWT, 3.9

The chart of S&P 500, $SPX, shows a close up 0.9%, higher at 1606.

For the week the chart of the US Dollar, $USD, close at 83.41, up 1.0%; individual currenies traded lower:

the Japanese Yen, FXY -1.5

the British Pound Sterling, FXB -1.4

the Australian Dollar, FXA -1.3

the Swiss Franc, FXF -1.0

the Euro, FXE -.8

the Indian Rupe, ICN -.7

the Swedish Krona, FXS -.5

Reuters reports Consumer sentiment ends June to near six-year high. I comment that the sentiment comes from Liberalism’s policy of monetary expansion and schemes of Quantitative Eassing, Stimulus, and Global ZIRP. Retailers Macy’s, M, and Pacific Sunswear, PSUN, are outstanding retail stock market performers, as is seen in their combine ongoing Yahoo Finance Chart, having benefited from credit liquidity, and as Doug Noland relates M2 (narrow) “money” supply rose $3.9bn to a record $10.594 TN. “Narrow money” expanded 6.6% ($661bn) over the past year

Doug Noland writes Uninsurable risks. More than a decade ago, Dr. Bernanke, with his “helicopter money” and “government printing press,” arrived on the scene with academic theories to fight the scourge of deflation. Well, the tech Bubble had burst – but I argued strongly at the time that THE greater Credit Bubble was very much alive and well. Extraordinary Fed stimulus was poised to inflate the fledgling mortgage finance Bubble. I argued in 2009 that THE Bubble hadn’t burst, instead unmatched global fiscal and monetary stimulus had unleashed the “granddaddy of them all” – the global government finance Bubble.

I have in past CBBs noted key differences between the traditional government currency printing press and today’s newfangled electronic version. Traditional monetary inflations created government currency – purchasing power that worked to bid up prices throughout the real economy. The contemporary “printing press” creates electronic debit and credit entries that predominantly provide new purchasing power that bids up prices of financial assets. I have argued that this mechanism has been fueling dangerous securities markets and asset Bubbles around the globe. I have further argued that the Fed and central banks had unwittingly nurtured acute Bubble fragility to any potential reduction in central bank liquidity.

How does one reconcile massive ongoing “money printing” with deflating commodities prices and generally contained consumer price inflation? Well, perhaps the commodities market is the proverbial “canary in the coalmine” warning that QE has indeed fueled increasingly vulnerable Credit and asset Bubbles. The backdrop is increasingly reminiscent of the late-1920s, when many (including the Fed) believed weak commodity prices were a call for further monetary accommodation. I am today playing the role of the “old codgers” from the Roaring Twenties that warned of the dangers (and utter futility) of trying to sustain a deeply maladjusted system and historic financial Bubbles. While they were correct in their analysis, history has been unkind to these “liquidationists” and Bernanke “Bubble poppers.”

Dr. Bernanke (and conventional thinking) is convinced the issue during the late-twenties and thirties was deflation and the Fed’s negligence in failing to print sufficient money supply. I am convinced that Bernanke’s analysis is flawed: the key issue was the Fed repeatedly placed “coins in the fusebox” during the twenties – in the process accommodating precarious financial and economic Bubbles.

Quantifying current Bubble risk is an impossible task. Global debt and securities markets easily surpass a hundred Trillion. Gross derivative exposures are in the many hundreds of Trillions. The now enormous Chinese and EM financials systems, in particular, lack transparency. The amount of global speculative leverage is unknown. The degree of global financial distortion and economic maladjustment will not become apparent until the next major period of market risk aversion and resulting tightened global financial conditions. For now, recent market gyrations support my view of precarious Latent Market Bubble Risks.

I’ll attempt to use some data to illustrate how Fed policymaking has greatly exacerbated already outsized market risks. As a crude proxy for “market risk,” I’ll combine outstanding Treasury debt, Agency debt/MBS, Corporate bonds, municipal debt and the value of U.S. equities – securities that fluctuate in the marketplace based upon perceptions of value, liquidity and risk. It is worth noting that “market risk” had inflated to $33 TN during the booming nineties, after beginning the decade at $10 TN. Importantly, the nineties saw a fundamental shift to market-based Credit instruments, with the proliferation of ABS, MBS, the GSEs and “Wall Street Finance” more generally.

I have over the years argued that Credit is inherently unstable. The move to market-based debt instruments created an acutely unstable Credit system, instability that provoked a change at the Federal Reserve to a policy regime committed to backstopping the securities markets. For more than twenty years now, this new policy regime has led to an unending series of Bubbles, booms and busts, even more aggressive policy responses and only bigger, more precarious Bubbles. This is critical analysis that remains completely outside of mainstream economic thinking.

When Dr. Bernanke began his crusade against deflation risk back in 2002, “market risk” was at $29.7 TN. Extraordinary monetary stimulus (and resulting mortgage finance Bubble excess) was instrumental in market risk surging to $53 TN by the end of 2007, before dropping abruptly to $44.8 TN in 2008. During the past four years, “market risk” has inflated $16.7 TN, or 37%, to a record $61.5 TN. Perhaps more illuminating, as a percentage of GDP, “market risk” began the 1990’s at 182% and closed the decade at 323%. While conventional thinking subscribes to the deleveraging viewpoint, I believe the data strongly support my re-leveraging and historic Bubble thesis.

I will posit that years of central bank intrusion and market domination have made global risk markets “Uninsurable.” “Market risk” has ballooned precariously higher, with massive issuance of non-productive government debt and other late-cycle private-sector Credit excesses. Meanwhile, central bank liquidity injections have inflated global asset market prices, while inciting speculation along with a manic global search for yield. Maladjusted global economies are increasingly succumbing to the debt and maladjustment overhang, while Financial Euphoria has seen securities markets inflate into dangerous speculative Bubbles.

There is a great flaw in the Bernanke doctrine of inflating the Fed’s balance sheet to both accommodate massive fiscal deficits and inflate securities markets, while using zero rates to force savers into the risk markets. This has led to an unprecedented (and problematic) mispricing of debt and securities prices globally, while incentivizing leveraging and speculation. Trillions of risk-conscious “money” has flowed into global markets (through ETFs, hedge funds, mutual funds, etc.) with little appreciation for the true risk-profile of global financial markets. One could say a Bubble in perceived low-risk “investing” evolved into a key facet of the overall global market risk Bubble.

Importantly, at least segments of the “global leveraged speculating community” must by now be increasingly impaired. The gold, precious metals and commodities “reflation trade” has been an unmitigated disaster. While not yet a full-fledged disaster, the popular emerging market (EM) trade is unraveling. The currencies and global leveraged “carry trades” have become a perilous minefield. Global fixed income markets, more generally, are increasingly unstable and illiquid.

Above I mentioned how Federal Reserve doctrine changed during the nineties to support the proliferation of market-based Credit. The market for derivatives and myriad types of risk insurance ballooned right along with Credit and market risk during the 1990s. I’ve argued over the years that Credit and financial market risk were actually Uninsurable – in that they are neither random nor independent events such as car accidents and house fires. Actually, it is the nature of market risks to come in particularly non-random and non-independent waves. Somehow the lessons of 2008 were quickly unlearned.

Global central banks have unwittingly inflated risk and grossly distorted the risk “insurance” landscape across global risk markets. We’ll see how long “capital” continues to flock to global securities markets. Early indications of how global risk markets will function in the face of a reversal of flows is anything but encouraging.

FT reports Greece faces collapse of second key privatization. Greece is struggling to avoid the collapse of a second big privatisation, amid pressure from bidders for the state gaming monopoly to change terms of a deal agreed last month. The problems with the €700m sale of OPAP threaten to add to tension with Greece’s international creditors, who fear the slow pace of privatisations will require further more cuts to keep the country’s bailout programme on track. Emma Delta, a bid vehicle backed by Greek oil tycoon Dimitris Melissanidis and Czech billionaire Jiri Smejc, made the only offer for the Greek state’s 33 per cent holding in OPAP. According to documents seen by the Financial Times, Emma Delta now wants to cancel two elements of the deal: a three-year, €110m contract with Intralot, OPAP’s Athens-based technology supplier; and a 12-year concession to operate the Greek state lottery in return for a €190m down payment and €50m annually.

The lottery was awarded last year to a consortium including OPAP, Intralot and Scientific Games of the US, the world’s largest lottery software provider. Neither contract has been signed. Greece’s privatisation agency, Taiped, has rejected formal complaints by Emma Delta threatening to pull out of the deal and take legal action if its demands are not met.

Costas Louropoulos, OPAP’s chief executive, complained in an email seen by the FT that he felt put under pressure by Mr Melissanidis in a series of telephone calls. “He insulted me, as on many previous occasion. You dare to sign [the Intralot and lottery contracts] and I will take your head off,” Mr Louropoulos quoted Mr Melissanidis as telling him on May 20. Taiped failed to deliver one flagship privatisation this month when Gazprom unexpectedly pulled out of the bidding for the state natural gas supplier Depa. If the OPAP sale falls through, Greece’s privatisation programme will be in disarray, raising the possibility that the “troika” of international lenders – the International Monetary Fund, European Central Bank and EU Commission – could appoint international managers to replace Greek executives hired by the Athens government to sell €15bn of state assets by 2016.

A review of Greece’s bailout by the IMF this month found that income lost through slippage of the privatisation programme would contribute to a hole in Athens’ budget and “additional financing will need to be identified”. The disposals of Depa and OPAP were expected to cover about half this year’s €2.6bn target for privatisation revenues agreed with the EU and IMF but failure to sell OPAP would probably to see income from disposals this year fall below €1bn. The target has already been revised downwards twice because of the risks associated with investing in recession-mired, politically unstable Greece. Taiped has pulled off only one sizeable deal this year: the €400m sale of Desfa, the natural gas grid operator to Socar, the state gas operator of Azerbaijan.

Stelios Stavridis, Taiped’s chairman, insists that the OPAP deal must not be changed. “The country’s credibility is at stake,” he said. “We’ve made clear that we’re responsible people [at Taiped] and that no one can interfere with our work.”

Mr Melissanidis controls Aegean Marine Petroleum Network, a global supplier of marine fuel listed on the New York Stock Exchange. Mr Smejc is the owner of Emma Capital, an investment company, and is one of the largest shareholders in Greece’s Piraeus Bank.

The other partners in the vehicle are also financial investors: Russia’s ICT group, J&T Finance of Slovakia, Czech-based KKCG and Christos Copelouzos, a Greek businessman with ties to Gazprom. Lottomatica, the Italian gaming operator, is also a participant.

Critics of Greek privatisation say the OPAP dispute illustrates how Taiped’s mandate to “sell to the highest bidder” without giving priority to qualitative criteria or operational experience has undermined the programme. “The programme has suffered overall because of a lack of interest from globally recognised players,” said one consultant who declined to be named.

Mr Stavridis, Taiped’s third chairman in less than a year, said he was “cautiously optimistic” about persuading Emma Delta to drop its demands. “We negotiated the OPAP deal in a transparent way and in line with international practice. Now we have to make it stick,” he says.

Bloomberg reports China bad loan alarm sounded by record bank spread jump. Borrowing costs for Chinese banks have surged the most in at least six years this month as rating companies say a cash crunch threatens to swell bad loans. The yield spread for one-year AAA bank bonds over similar maturity sovereign notes jumped 56 basis points so far this month to 163 basis points, the most in ChinaBond records going back to 2007. The similar AA gap widened 59 basis points to 188. Even as China Construction Bank Corp President Zhang Jianguo said yesterday cash conditions have normalized, the benchmark seven-day repurchase rate was fixed at 6.85 percent, almost twice the 3.84 percent average for this year.

The PBOC is seeking to wring speculative lending out of the system after total credit approached 200 percent of gross domestic product, according to Fitch Ratings. “There could be unintended consequences from the central bank’s approach,” said Liao Qiang, a Beijing-based director at Standard & Poor’s. “We expect some deleveraging at banks’ interbank and wealth management businesses to unfold. Credit growth would slow. This could pressure banks’ asset quality.”

The one-year interest-rate swap, the fixed cost needed to receive the floating seven-day repurchase rate, touched an all-time high of 5.06 percent on June 20, according to data compiled by Bloomberg. The one-day repo rate surged to a record 12.85 percent the same day, according to a daily fixing announced by the National Interbank Funding Center.

The yield on 10-year government bonds rose 13 basis points to 3.60 percent last week, while the one-year borrowing cost jumped 51 basis points to 3.61 percent, inverting the so-called yield curve for the first time in ChinaBond data going back to 2007. The 2023 yield closed at 3.53 percent yesterday.

Bad loans at banks including Industrial & Commercial Bank of China Ltd. have increased for six straight quarters through March 31, the longest streak in at least nine years.