Introduction

The recent fall in the Euro, FXE, from its November 2009 value of 149 strengthened exports from Germany and strengthened European manufacturing and service economic activity as a whole.

But a large y-o-y decline in Taiwanese export data, and a decline in the number of job opening in the US for a second straight month, a rise in the Ten Year Interest Rate above 3.4% portend a global economic downturn is at hand.

And now today a failure of quantitative easing, communicates that the world has passed from the Age of Leverage …. and into the Age of Deleveraging.

Financial market report for February 22, 2011

1) … EuroIntelligence reports the purchasing managers index for the eurozone has reached new heights.

The composite purchasing managers index in the eurozone, including manufacturing and services, expanded strongly during February to a level of 58.4, the highest since July 2006. The German sub-index rose to 62.6, the highest level since the beginning of the series in 1996. Germany’s Ifo index rose to the dizzy heights of 111.2, the highest level since German unification. Frankfurter Allgemeine quotes Chris Williamson, chief economist of Markit, as saying that the eurozone periphery was also growing, which would reduce the growth gap. The FT writes that inflation is very likely to have risen further in February.

2) … Quantitative easing continued to exhaust today, a process that began with the formal announcement of QE 2 in November 2010.

Michael Pento, senior economist at Euro Pacific Capital Inc. in New York, who correctly predicted the 2008 commodity-market collapse, relates: “Bernanke is not only off base with regard to inflation he’s off the entire planet” … “Inflation will go much higher … You can’t continue to have a reckless monetary policy and a government issuing endless quantities of debt and also have the supposition that you have the world’s reserve currency and low interest rates.”

Exhaustion of quantative easing has turned the World Financials, IXG, lower. The Brazilian Financials, BRAF, Australian Bank, Westpac Banking, WBK, India Bank, HDFC Bank, HDB, the European Financials, EUFN, led by Banco Santender, STD, and the Emerging Market Financials, EMFN, all fell lower, communicating an end to the seigniorage, that is moneyness provided by quantitative easing and the seigniorage of central banks globally. Seigniorage failed February 22, 2011.

Confirmation of the failure of seigniorage comes from the fall lower in distressed investments like those in mutual fund, FAGIX, which constitute a large part of the US Federal Reserve’s balance sheet, and which served to underwrite the recovery of the last two years. Also the turn lower in junk bonds, JNK, from its recent high, and a topping out in world government bonds, BWX, serves as evidence to the end of US central bank seigniorage. Without seigniorage, stocks will fall precipitously world wide. And economic expansion will turn to economic contraction.

Quantitative Easing Exhaustion has its epicenter first the airlines, FAA, struck by high oil prices, then the once red hot emerging markets, EEM, then coal, KOL, and now in the banks, KBE, and the too big to fail banks, RWW, then the basic material shares, XLB, and then the agricultural shares, MOO, and then the industrial, IPN, shares, The countries and stocks which first benefited from QE, are now falling, like dominoes all falling one upon another.

The fall in the European Oil Companies ENI, E, and Repsol, REP, gives stark testimony that the once inflationary quantitative easing is now acting to deleverage profitable investments. In addition to the basic material late bloomers of the past rally, integrated circuit manufacturer, Jabil Circuits, JBL, which received a late dose of the QE cool aid, fell sharply. Diversified equipment manufacturer, CMI, fell sharply as well. And Design and Build leaders, Foster Wheeler, FWLT, and Fluor, FLR, fell sharply too.

Gold, GLD, and Silver, SLV, and Precious Metal, JJP, exploded higher, as the US Federal Reserve’s monetary policies monetize the US Sovereign Debt and create an investment demand for gold.

Oil, USO, and Brent Oil, BNO, and Gasoline, UGA, exploded higher on turmoil in Libya.

Base metal prices, DBB, turned 3.4% lower, turning basic material stock, XLB, 3.2% lower with Aluminum, JJU, Copper, JJC, Lead, LD, Tin, JJT, and Nickel, JJN all turning lower.

Timer, CUT, turned lower. Historically timber has been a fast faller.

Food commodities, FUD, agricultural commodity prices, JJA, and, DAG, cooking oils, FUE, turned lower, with grains, GRU, and corn, CORN, seeing significant losses. These turned agricultural stocks, MOO, such as Monsanto, MON, lower

Falling commodity prices, DJP, turned 1.0% lower, turning world stocks, ACWI, 2.7% lower.

Countries falling strongly today included

Gulf States, MES, 5.6%

Italy, EWI, 5.6%, and Spain, EWP, 4.5% are once again deflationary leaders

Africa, AFK, 5.2%

Brazil Small Caps, BRF, 4.0%, Brazil, EWZ, 3.0%, and Brazil Financials, BRAF, 4.0%.

China Technology, CQQQ, 6.0, Shanghai, CAF, 4.1%, China All Caps, YAO, 3.7%, China Small Caps, HAO, 4.5%, China Materials, CHIM, 3.7%, China Financial, CHIX, 4.0%, and China Real Estate, TAO, 4.1%.

Korea, EWY, 4.0%, and South Korea, SKOR, 4.0%, fell lower on less export growth. Korea is a fallen Asian Tiger.

Turkey, TUR, 4.5%, Turkey had seen tremendous inflationary money flows coming from QE 1 and the anticipation of QE 2, now Turkey is a quantitative easing inflationary loss leader along with Indonesia, IDX, India, INP, and China, YAO. Inflation drove up stocks in these countries, and now Quantitative Easing Exhaustion is rapidly deleveraging investment in these once hot countries as is seen in the chart of TUR, IDX, INP, and YAO

Australia Small Caps, KROO, 4.4%, and Australia, EWA, 3.6% fell lower on falling basic material prices.

Taiwan, EWT 4.5%

New Zealand, ENZL, 4.0%

Emerging Market Small Caps, EWX, 3.4%, Like Airlines, FAA, the Emerging Market Small Caps, EWX, were deleveraged by the announcement of quantitative easing in November; today these are seeing more disinvestment as inflation gains are being taken out of these shares.

Latin America, LATM, 3.3%

Emerging Markets, EEM, 3.2%

Mexico, EWW, 3.1%

Europe, VGK, 3.0%

Indonesia, IDX, 2.8%

World Small Caps, VSS, 2.8%

Thailand, THD, 2.8%

Indices fell lower today.

Russell 20000, IWM, 2.6%

S&P, SPY, 2.0% The weekly chart of the S&P, SPY Weekly, communicates that the S&P entered into an Elliott Wave 3 Down today February 22, 2011. This is not only the chart of the day, but it is the chart of one’s lifetime.

Sectors falling strongly today included:

China Technology, CQQQ, 6.0%

Uranium Mining, URA, 5.5%

Airlines, FAA, 5.2%, Airlines were the first sector to be delverage on exhaustion of quantitative easing, their deleveraging came with higher oil prices; now with the higher price of oil, USO, deleverages them more.

Copper Mining, KOL, 4.8%. The coal mining stocks experienced deleveraging with the emerging markets, EEM, at the first of the year. Now they have fallen lower in an Elliott Wave 3 of 3 Down.

Steel, SLX, 4.6%

Home Building, ITB, 4.1%

Metal Manufacturing, XME, 4.1%

Copper Mining, COPX, 4.0%

Transportation, IYT, 3.9%

Leisure and Entertainment, PEJ, 3.8%

Clean Energy, QCLN, 3.8%

Shipping, SEA, 3.8%

Basic Materials, IYM, 3.5%

Banks, KBE, 3.5%

Small Cap Information Technology, XLKS, 3.3%

Gaming, BJK, 3.3%

Design Build, PKB, 3.3%

International Industrial, IPN,

Basic Materials, XLB, 3.2%

Solar, KWT, 3.2%

Networking, IGN, 3.2%

Design Build, PKB, 2.3%

Clean Energy, ICLN 3.1%

Global Financial Firms, IXG, 3.1%

Too Big To Fail, RWW, 3.1%

Financial, XLF, 3.1%

Coal, KOL, 2.9%

Intenet Retail, HHH, 2.9%

Leveraged Buyouts, PSP, 2.9%

Water, FIW, 2.8%

Transportation, IYJ, 2.8%

Small Cap Industrial, XLIS, 2.8%

Timber Producers, WOOD, 2.7%

Small Cap Pure Value, RZV 2.7%

Small Cap Revenues, RWJ, 2.7%

Insurance, KIE, 2.7%

Internet Software, ICGE, 2.6%

A sample listing of leading companies falling lower:

NVIDIA, NVDA, -9.4%

Quality Distribution, QLTY, -8.6%

Foster Wheeler, FWLT, -8.2

CEVA Inc, CEVA, -8.0%

Terex, TEX, -7.2

CNH Global, CHN, -6.9%

US Steel, X, -9.6%

Micron Technology, MU, -6.7%

The Morgan Stanley Cyclical Index, Transportation Component, Goodyear Tire, GT -6.6%

Cummins, CMI, -6.3%

Weatherford, WFT, -6.0%

Saks, Inc, SKS, 5.6%

Regions Financial, RF, -5.2%

Lennar, LEN, -5.2

BE Aerospace, BEAV, -4.5%

Flash Memory Storage Manufacturer, San Disk, SNDK, -4.8%

Blackrock, BLK -4.0%

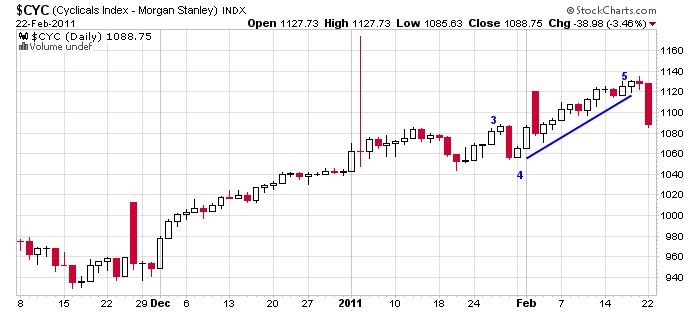

The Morgan Stanley Cyclical Index, $CYC, fell lower; its fall communicates an end to the current growth cycle. Given that this growth cycle, and the rise in the Morgan Stanley Cyclical Index, came via the extreme use of the seigniorage of QE, its reasonable to believe that there will be a dramatic fall lower in stock value, and then “in delayed time” a downturn in economic reports such as Capitol Goods Orders, Industrial Production, Exports, and Bloomberg Financial Conditions Index, as quantitative easing continues to exhaust, effecting deleveraging both in stock market value and in economic activity as well.

The investors barometer, the Nasdaq 100, QTEC, fell a massive 3.3%; its fall communicates a trend reversal from bull to bear for stocks globally.

The 2.8% fall lower in the Industrial stocks, IYJ, comes at the same time as the 3.9% fall lower in the Transportation stocks, IYT, and communicates the Dow Theory principle that a bear market has commenced — as industrial stocks and transportation stocks make market turns together.

This bear market will be the bear market of all bear markets, as the seigniorage of the Milton Friedman Free To Choose Currency Regime, that being the distressed investments held by the US Federal Reserve, FAGIX, and, the 30 Year US Government Bonds, EDV, and 10 Year US Government Notes, TLT, is no longer providing moneyness, to world stocks, VT, and world small cap stocks, VSS. There will be a follow on effect whereby “in delayed time”, there will come a downturn in economic reports such as Capitol Goods Orders, Industrial Production, Exports, and Bloomberg Financial Conditions Index, as quantitative easing continues to exhaust.

The US Dollar, $USD, rose a tiny amount as world currencies, DBV, fell sharply, and the emerging market currencies, CEW, traded lower by a small amount today.

Commodity currencies, CCX, such as the New Zealand Dollar, BNZ, the Russian Ruble, XRU, the Australian Dollar, FXA, fell lower today. The British Pound Sterling, FXB, the India Rupe, ICN, turned lower. The South African Rand, SZR, a commodity currency traded slightly lower, as did the Swedish Krona, FXS, and the Brazilian Real, BZF. The Euro, FXE. the Mexico Peso, FXM, the Canadian Dollar, FXC, and the India Rupe, ICN, traded unchanged. The Swiss Franc, FXF, rose. Those long carry Swiss Franc carry trades profited, such as the Swiss Franc and Euro carry trade, FXF:FXE.

The chart of the Optimized Carry ETN, ICI, fell significantly lower in an Elliott Wave 3 Down, suggesting that investing long via borrowed funds is no longer a profitable endeavor. With the failure of QE 2 today, and the failure of carry trade investment as well, the spigots of financial liquidity have run dry as well as toxic. The only way for stocks to go is down, and down. Debt deflation is the way of the future. Debt deflation is the contraction and crisis that follows credit expansion. One of the most famous quotations of Austrian economist Ludwig von Mises is from page 572 of Human Action: “There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of a voluntary abandonment of further credit expansion or later as a final and total catastrophe of the currency involved.” The world entered into Kondratieff Winter today February 22, 2011.

The currency traders commenced a global currency war against the world’s central bankers by selling the US Dollar, $USD, at the beginning of 2011 from 81.00, as the purchase of US Treasuries by Ben Bernanke under QE 2 constitutes monetization of debt and debases the currency.

It was at this time that the emerging market currencies, CEW, also were successfully sold by the currency traders, effecting competitive currency devaluation, that is competitive currency deflation, and caused the emerging market currencies to fall into an Elliot Wave 3 Decline.

The world major currencies, DBV, double topped: first with the announcement of QE 2 and then on February 8, 2010; they commenced their decline today February, 22, 2011.

Its reasonable that the major currencies, DBV, would start to fall lower today, more than the emerging market currencies, CEW, as they have more sovereign debt burden …. this accelerated fall of the major currencies is seen in the chart of DBV:CEW Daily.

The fall was reflected in flattening of the currency yield curve, the ratio of the small cap value share, RZV, relative to the small cap growth shares, RZG, ….. RZV:RZG,

Bonds, BND, rose,

Summary

The failure of the QE rally and the EFSF rally in stocks, is the consequence of the false stimulation that has come via quantitative easing and unrealistic values for European Financial Institutions.

The misery of Ben Bernanke’s inflation that has come to hundreds of millions in higher food costs, and loss through cultural revolution is incalculable; but those owning gold and silver bullion can count their gains quite well.

The gold mining stocks, GDX, and the junior gold mining stocks, GDXJ, manifested bearish engulfing an traded lower, whereas gold, GLD, rose, establishing that the gold mining stocks have disconnected from the price of gold, and that the contagion of quantitative easing exhaustion has caught up with these as well. The HUI Precious Metal Mining Stocks, ^HUI, have been the great swing trade of the last ten years, riding a flattening 10 30 US Sovereign Debt yield curve for tremendous gain. But now, with exhausting quantitative easing, the gold mining stocks are loosing their tremendous leverage. Presented below is the 30 10 US Sovereign Leverage Curve, $TYX:$TNX, which is the inverse of the 10 30 US Sovereign Debt yield curve. It communicates that investors in the 30 Year US Government Bond, EDV, suffered loss, compared to investors in the 10 Year US Government Note, TLT, on announcement of QE 2 at Jackson Hole, and then again with the formal announcement of QE2 in November 2010.

Today the gold mining stocks disconnected from the price of gold, as is seen in the chart of GDX:GLD. And of note, the gold mining stocks are now turning lower with the 30 Year US Government Bond, as is seen in the chart of $HUI:$USB.

It just is non productive for capitalists to risk their capital digging around in the ground for new gold. Risk appetite turned to risk avoidance today. The price of existing gold will become more and more dear all the time, as is communicated in the chart of the gold relative to the Australian Dollar, GLD:FXA.

Gold has arisen to be sovereign wealth and the sovereign currency. Stocks, bonds and and now fiat currencies, are falling into the pit of financial abandon together “as the where-with-all for investment has been undone by the bond traders calling the interest rate higher on soveign debt across the board”. that is higher on the 30 Year US Government Bond, $TYX, on the 10 Year US Government Note, $TNX, on emerging market bonds, and on world government bonds. The destruction of seigniorage, that is the destruction of moneyness, is seen in the fall in value of the 30 Year US Government Bond, EDV, the US Government Note, TLT, Emerging Market Bond, EMB, and World Government Bonds, BWX.

The where-with-all since the last financial collapse has come via quantitative easing and quantitative easing 2. The seigniorage, that is the moneyness, came via an asset swap, where Ben Bernanke, traded out money good US Treasuries for distressed securities, like those traded by mutual fund FAGIX. For the most part, then the banks placed the US Treasuries into Excess Reserve with the Fed. The distressed investments, and the Excess Reserves have been the great springboard of investment growth, that is they have been the seigniorage for the stock expansion of the last two years.

Today February 22, 2011, was a day that will live in financial and economic infamy, as quantitative easing failed, and the seigniorage of the US Federal Reserve failed, as the mutual fund FAGIX, and Junk Bonds, JNK, both turned down today, in accompaniment of falling stock values worldwide, ACWI. The United States, has lost totally lost its debt sovereignty, that is its debt and currency seigniorage.

Soon there will come Gotterdammerung, an investment flameout, as US Government Treasuries, EDV, the US Government Ten Year Note, TLT, and World Stocks, ACWI, loose more and more value, Then out of the ensuing chaos a global Chancellor, that is a Sovereign, and a global Banker, that is a Seignior, will arise to establish global order, a new and universal Seigniorage with austerity for all.

In Today’s News

Mother Mags of Daily KOS Education relates Arizona will consider SB 1519, which will eliminate Arizona’s Medicaid program, and create a severely underfunded version within the Department of Health Services. Quoting Sinema again, Lemons points out the insanity of this policy, not that any of these bills make economic or humane sense: “According to state Senator Kyrsten Sinema, this will result in “savings” to the state of $900 million, and a resulting loss of $7.6 billion in federal aid.”

I comment that if Medicaid is cut, then there will be a flood of Medicaid refugees to other states.

Joe Weisenthal of Business Insider relates: The year-over-year decline in home prices, as measured by the Case-Shiller, accelerated to 2.4% from over 1.5% in November … Eleven of the markets hit their lowest point since the housing bubble burst in 2006 and 2007: Atlanta, Charlotte, N.C., Chicago, Detroit, Las Vegas, Miami, New York, Phoenix, Seattle, Tampa, Fla., and Portland, Ore

CBS News reports Michigan’s Flanagan orders Detroit to close half its schools … And I say thank God. Close all failing schools immediately.

Gotterdammerung, Currency Yield Curve, Sovereign Debt Leverage Curve, Morgan Stanley Cyclical Index, Global Currency War, Competitive Currency Deflation, Competitive Currency Devaluation, Seigniorage, The Sovereign, The Seignior, IFO, Exhaustion of QE, QE Exhaustion, Quantitative Easing Exhaustion, Age of Deleveraging, Exhaustion of Quantitative Easing,

Leave a comment