Financial Market Report for June 23, 2011

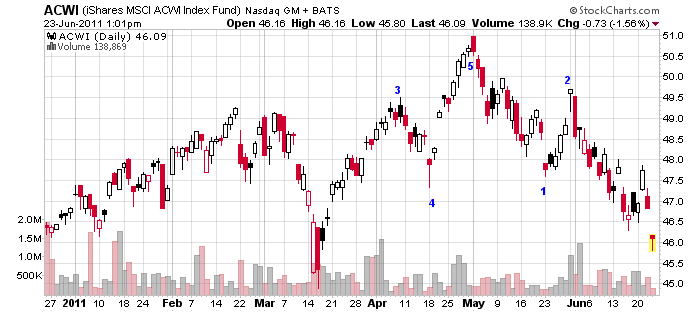

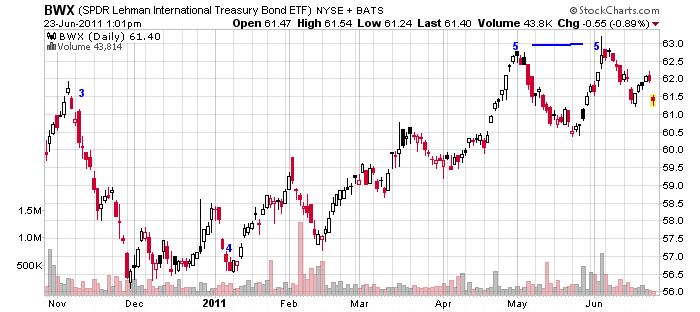

1) … World Stocks and World Government Bonds, fell lower after Ben Bernanke spoke from the Federal Reserve; Mike Mish Shedlock writes the Fed has lowered (yet again) its economic forecast. It also lowered its inflation expectations, primarily because of falling gasoline prices … Chart of ACWI

BWX,

Harvard University Professor Martin Feldstein wrote in the Financial Times expressing the growing awareness that the rating agencies will downgrade Greek to default status as Germany pushes plans for a rollover of Greek sovereign debt.

In Sovereignty News, Martin Wolf of the Financial Times writes in Open Europe, A more efficient Union will be less democratic

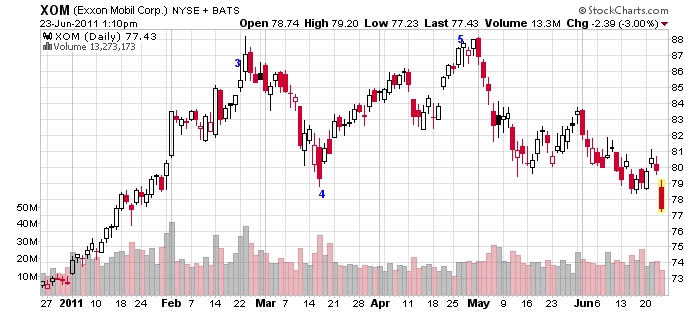

2) … Stocks falling lower included Exxon Mobil, XOM

3) … Stock ETFs falling lower included

GDXJ

EUFN

GDX

REM

PSCE

SIL

COPX

XLE

4) … Country ETFs falling lower included

NORW,

EWD,

EWY

EWO

EWL

CNDA

KROO

VGK

5) … Commodities, DJP, fell lower on sharply lower oil BNO, USO, and DBC as the Asscoiated Press reports The International Energy Agency, which includes the U.S. and 27 other countries, said Thursday it would release 60 million barrels of oil from emergency stocks in an effort to stave off a possible spike in energy prices that could strain the global economic recovery. This marks only the third time in its history that the Paris-based agency has released oil onto the markets. Half of the 60 million barrels will come from the U.S.’s emergency stocks. The oil will be released over the next 30 days.

6) … The US Dollar, $USD, UUP, rose as the world’s currencies, DBV, Commodity Currencies, CCX, and Emerging Market Currencies, CEW, were taken lower on collapsing Euro, FXE, South African Rand, SZR, and Swedish Krona, FXS, as is seen in this Finviz screener of FXA, FXE, FXM, FXC, ICN, FXB, FXS, SZR, FXF, CYB, BZF, XRU, FXY, BNZ, DBV, CEW, and CCX. Only the Swiss Franc, FXF, rose; it remains near its all time high. Exhaustion of quantitative easing, and sovereign crisis is inducing competitive currency devaluation, that is competitive currency deflation. The Milton Friedman, Free To Choose, floating currency regime, is history as the world’s currencies are following the US dollar into the Pit of Financial Abandon.

The Age of Leverage is over and the Age of Deleveraging is over now that the Seigniorage of Liberalism has failed; this being seen in the world banks falling lower; thes include

South Korea Bank, KB Financial, KB

European Bank: Paraibas France, BNPQY,

European Bank: Switzerland, UBS Bank, UBS,

Australian Bank: Westpac Banking, WBK,

Brazil Financials, BRAF,

Chile Banco de Chile, BCH,

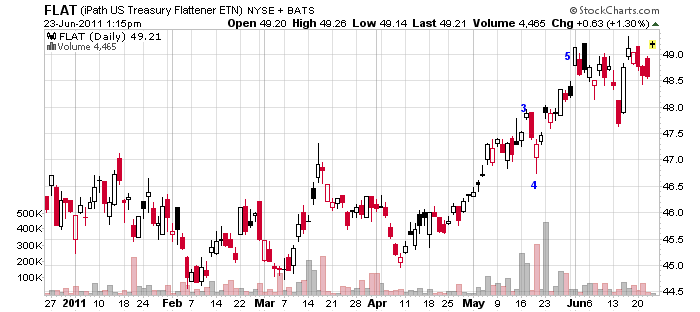

7) … The longer out US Treasuries, such as ZROZ, EDV and TLT increased more than the shorter duration ones such as IEF, as is seen in the Flattner ETF, FLAT, rising to a double high.

8) … Europeans Doubts Greece’s Ability To Enforce Its Austerity Plan, NYT Reports … Rachael Donadio of the New York Times Europe doubts Greece’s ability to enforce its austerity plan …

In the year since Greece received its first financial bailout, many things have changed. The country has reduced its budget deficit by 5 percent of gross domestic product. Workers have been hit by wage freezes and pension cuts, prompting a growing popular outcry. The state has revealed for the first time how many people it employs, and tax collectors can now cross-reference swimming pool ownership with declared income to help determine wealth and cut down on rampant tax dodging

But some things are harder to change. Asked if the state had the means, let alone the will, to properly collect taxes, Froso Stavraki, the head of the collectors’ union, took a long drag from a cigarette. “Huge efforts have been made,” she said in an interview in a cafe here last week. “But no, I don’t think people are afraid of us.”

A year ago, Prime Minister George Papandreou hammered out a $155 billion loan agreement with the European Union, European Central Bank and the International Monetary Fund. In return, Athens pledged a range of structural reforms: cracking down on tax evasion, raising the retirement age to 63 and a half from 61 and a half, limiting early retirement and opening the so-called closed professions whose guilds grant limited access to newcomers.

Now, as he comes back to Greece’s foreign creditors asking for the next $16.8 billion installment of aid — predicated on persuading Greeks to accept more tax hikes, wage cuts and the privatization of more than $71 billion in state assets before 2015 — doubts have emerged about the government’s ability to implement and enforce the measures it has already passed.

“The main problem is that he’s only been able to deliver on the parts of the austerity package that are easily enforceable and transparent and irrevocable,” such as cuts to public sector salaries and pensions, said Spyros Economides, a political scientist who co-directs the Hellenic Observatory at the London School of Economics. “Unfortunately, the rest of it is a complete mess.”

“It’s very easy to legislate,” Mr. Economides added. “The problem is to enforce legislation. There’s no enforcement mechanism. It’s all done for the eyes of the public.”

On Sunday, finance ministers from the euro zone will meet in Luxembourg and are expected to approve the next dispersal of aid. But if Mr. Papandreou fails to push through the new austerity measures that Parliament is expected to begin debating next week — with a confidence vote scheduled for Tuesday following a cabinet reshuffle last week — it could jeopardize the second rescue package that Greece needs in order to carry it through next year. A default would send the euro zone and world markets into a tailspin.

In March, Greece fired its top tax official on the grounds that he had not increased tax revenues enough. In 2010, Greece brought in 52.5 billion euros in tax revenue, up only marginally from 50 billion euros in 2009. The country failed to collect on another 40 billion euros in back taxes owed in 2010, Ms. Stavraki said. “The problem is that most usually pay 20 percent of what they owe, and then they disappear,” she said.

To try to break what Ms. Stavraki described as a “personal, human” rapport that many Greeks have with their tax collectors, the state is reducing the number of collection offices to 72 from more than 200, and introducing a centralized electronic database system. But it has also cut the salaries of tax collectors, a move some say could encourage corruption. “Morale is low,” Ms. Stavraki said.

Adding to the difficulties, as the panic and uncertainty spreads, Greeks continue to take their money out of local banks. According to data from the European Central Bank, Greek banks lost 4 billion euros in deposits in May, following 2.4 billion in losses in April — part of a bank run that has seen an estimated 60 billion euros, a quarter of Greece’s gross domestic product, leave the country since the crisis began.

In February, the government passed a much-publicized law that removed the barriers to some of the so-called “closed professions, which range from truck drivers to pharmacists to engineers.

Powerful guilds essentially control who can get a license to practice in those professions, a system critics say rewards connections over merit.

In late May, the Finance Ministry listed the 136 professions to be opened up starting in July. It includes taxi drivers and beauticians, but does not include three of the most powerful groups in Greece — notaries, lawyers and civil engineers. Their guilds are slated for liberalization “at a later date,” the ministry said, without specifying when.

Antonios Avgerinos, 60, a retired army pharmacist, said the new measures had still not helped him realize his dream of opening his own pharmacy. “Nothing has changed,” he said in a telephone interview. “Qualified pharmacists still can’t open their own businesses unless they have connections.”

As a Socialist elected with union support, Mr. Papandreou also faces resistance to the privatization of state assets, slated to be part of the next round of austerity measures.

Greece’s public power company union has called for rolling power cutoffs starting Monday to protest the government’s plan to sell 17 percent of the state’s stake in the Public Power Corporation, which is listed on the Athens stock exchange.

Costas Koutsodimas, the vice president of the union, known as Genop, called the plan a win for the banks and a loss to Greek patrimony, questioning how selling state assets, perhaps to foreign utilities that are reportedly interested in buying stakes, would be good for Greece.

“It’s a prefixed game, and it’s being played at the expense of the biggest state enterprises in Greece,” he said in an interview.

Yet even as austerity measures have brought pain to thousands of state workers, many Greeks, especially in the private sector, remain angry at a public workforce they view as an untouchable caste with the luxury of a guaranteed salary.

“Nobody’s accountable,” said Leo Apostolou, a Greek-Australian who owns two upscale delicatessens in Athens, echoing a widespread sentiment. He described his dealings with local officials as he tried to set up his second store in a wealthy northern suburb of Athens earlier this year. “I was never told directly that they wanted money,” he said. “But I was told that if I helped them in some way it would be quicker.”

Some analysts say it is unrealistic to expect Greece to transform such entrenched parts of its social fabric in so short a time, with the financial markets spinning far more quickly than the wheels of government or society.

“It is the most any developed economy has ever done in such a short space of time,” said Simon Tilford, the chief economist for the Center for European Reform in London. “And they have been pilloried for not having done enough.”

For others, the very prospect of foreign aid has hindered reform.

Today, the government and much of Greek society “sense that they can get away with all sorts of things because the euro zone partners are petrified of default,” said Mr. Economics of the London School of conomics. “They sense that at every turn, some form of bailout will be found.”

9) … G-Pap selects rival Evangelos Venizelos to move forward with privatization and austerity as London Thomas of the New York Times reports Tapped by a Rival, Greece’s New Finance Minister Faces Daunting Task. The article communicates that the Socialist Parties in Greece have stymied past deficit reduction programs but now the elites have settled their differences now that seigniorage aid is thretened.

10) … Bloomberg reports Trichet Says Risk Signals ‘Red’ as Debt Crisis Threatens Banks. European Central Bank President Jean-Claude Trichet said risk signals for financial stability in the euro area are flashing “red” as the debt crisis threatens to infect banks. “On a personal basis I would say ‘yes, it is red’,” Trichet said late yesterday in Frankfurt after a meeting of the European Systemic Risk Board, referring to the group’s planned “dashboard” to monitor risks. BNP Paribas (BNP) SA, France’s biggest bank, and rivals Societe Generale (GLE) SA and Credit Agricole SA (ACA), may have their credit ratings cut by Moody’s Investors Service because of their investments in Greece, the ratings company said on June 15. German banks could also be at risk from contagion, Fitch Ratings said last month. “The most serious threat to financial stability in the EU stems from the interplay between the vulnerabilities of public finances in certain EU member states and the banking system,” Trichet said. There are “potential contagion effects across the union and beyond.”

11) … Open Europe relates the author of the book “Democracy in Europe” Larry Siedentop looks at the lack of a European demos and argues: “[Europeans] have come to feel that integration is not something they are doing, but rather something that is happening to them. This is not bleak nationalism, but a concern for self-government.” Prospect: Siedentop

Leave a comment