I) … Charts Reveal Peak Credit

Global debt deflation commenced on April 26, 2010 when the currency traders sold the worlds currencies, DBV, off against the Yen, FXY. This was just weeks after the Federal Reserve QE ended, and as the European Sovereign Debt Crisis was coming to a head.

Debt deflation is the contraction and crisis that follows credit expansion. One of the most famous quotations of Austrian economist Ludwig von Mises is from page 572 of Human Action: “There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of a voluntary abandonment of further credit expansion or later as a final and total catastrophe of the currency involved.”

The greatest debt deflation came to the Russell 2000 shares, IWM and the European shares, FEZ.

As stocks, VT, rapidly fell in value, aggregate bonds, AGG, rose as a commonly perceived “safe haven” investment.

The apex in the chart of aggregate bonds, AGG, communicates” peak credit”; and that the “end of credit” will commence soon.

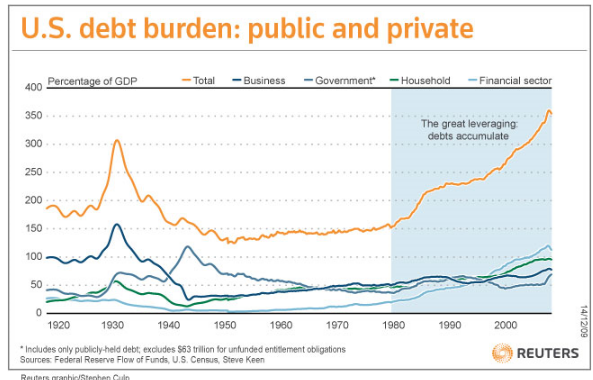

Dr. Housing Bubble in article Don’t Bet On A 2010 Recovery provides the Reuters chart of Total U.S. Debt Public And Private showing US Debt to be 350% of GDP. This is debt that can never be repaid. The chart shows a significant rise in financial sector debt especially since 2000 which when Wall Street financialization and securitization really took off due to the repeal of the Glass Steagall Act by a vote of 92 to 8 in the US Senate.

The US Ten Year note, IEF, is just now peaking; while the 30 year US Government Bonds, TLT, has peaked and is turning lower.

The yield curve, $TYX:$TNX, has been INCREASING, since April 26, 2010, because the 10 year rate has been falling faster than the 30 year rate.

The downturn in the 30 year US Government Bonds, TLT, should encourage institutional investors to go short the US Government bonds with the 300 percent inverse, TMV. When US Treasuries fail to auction, which will be soon, this will take off like a rocket greatly rewarding those who have invested in it.

Build America Bonds, BAB, show a topping out pattern.

Emerging Market Bonds, EMB, is peaking out.

Junk Bonds, HYG, is continuing upward.

The daily chart of high yield municipal bonds HYD Daily shows an awesome rise in high yield municipal bonds since April 26, 2010 … the weekly chart of HYD weekly shows that strong gains have been developing for a long time as investors have sought refuge from debt deflation destroying stock values.

The debt deflation which has been coming to stocks, will be coming to bonds as credit deteriorates. Very soon municipalities and states will be an epicenter of debt deflation, literally wiping out the value of HYD as the yield on HYD rises. Yes, higher interest rates will come to this investment vehicle as credit ratings by the rating agencies drop, and as more and more cities and municipalities fail to make interest and debt payments because of revenue shortfalls.

Soon, municipalities will find themselves unable to borrow because interest rates will either be too high or the municipal bond market place will be closed because the US Treasury bonds will fail to auction. It is as Nassim Taleb relates: ”We Are Going To Have, At Some Point, A Failed Auction”.

Government employees with their high pay and high pension funded jobs have multiplied in municipal, state and federal government, creating a pay disparity between private and public sectors as documented by MyBudget360.com

Andy Fixmer and Christopher Palmeri of Bloomberg report on July 23, 2010: “U.S. cities and states may need more than $1 trillion of federal assistance in the next three years to stave off financial failure, former Los Angeles Mayor Richard Riordan said. Local governments are in a ‘race to the bottom’ and U.S. taxpayers will inevitably be called on to bail them out, Riordan said … The federal government should make pension, health-care and school reform a condition of receiving the aid, he said. ‘It’s not just L.A., it’s not just California, it’s all over the country, you’re going to see all these entities become totally insolvent,’ Riordan said. ‘I think the federal government has to come in and have a list of what the states have to do to be saved.’”

I see no chance, repeat no chance whatsoever, that the US Federal Government will come to the aid of municipalities or states. The money simply is not there, nor will it be there. We will soon see the end of entitlements — entitlement programs, with the exception of food stamps, entitlements will be cut off.

The only monies flowing will be for strategic purposes. Austere sacrifices will be required for committment to President Obama’s International Order, that is the policy of global order of security and defense. GlobalResearch.ca reports the Xinhau news of July 17, 2010 that Canada is onboard for this endeavor as it plans to buy Buy 65 F-35 Lightning II Joint Strike Fighters.

Interest rates are going higher soon for a number of reasons. One primary reason will be Treasury Auction failures. Soon, the interest rate will be out of the government’s control, and they will no longer be subsidizing mortgage rates. Freddie Mac and Fannie Mae will not be funded as liquidity evaporates. Mortgages will not be offered by the GSEs or the banks.

If the lenders write down the mortgage debt to reach market values it will decapitalize them so severely that they will go out of business and the FDIC will not be able to close banks fast enough to keep up with the failures. Therefore, I see foreclosures (simply to get the people physically out of the house) and then the banks, Freddie Mac, Fannie Mae, and the US Federal Reserve leasing to someone who will pay rent. If the banks are smart they will line up renters before they foreclose. Perhaps there will be many people living in one property, that is multiple families, in violation of rules now existing in many better neighborhoods.

I envision, that out of the coming credit crisis, where there will be no credit available, a Financial Regulator will exercise Discretionary Governance, and announce a Home Leasing Program administered by the banks on their REO properties and those of Freddie Mac, Fannie Mae and the US Federal Reserve.

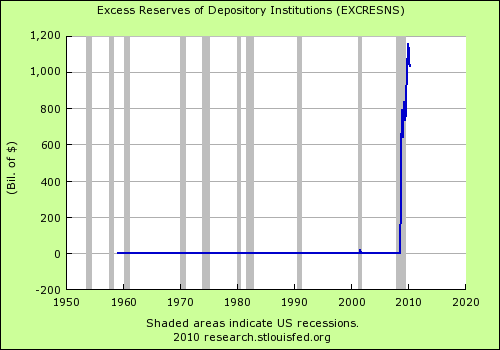

As credit deteriorates, the value of excess reserves will rapidly decrease as well. Dr. Housing Bubble in article Japan Iwato And Heisei Stock And Housing Bubbles presents a chart of Excess Reserves totalling over $1 Trillion at the current time. These are largely the US Treasuries that the Federal Reserve swapped out to recapitalize the banks through its QE TARP Facility. The so-called excess reserves are residing at the US Treasury. As the value of US government bonds, IEF, and TLT, and ZROZ, falls lower, the value of the excess reserves will shrink dramatically in value, as either the banks pull them and sell to stay capitalized or simply “rot on the vine” so as to speak.

Utilities, XLU, have escaped debt deflation so far as dividend payment season approaches. And some utilities are paying exceptional dividends and it can be seen in their stock values soaring well above their April 26, 2010 values. Morris News Service reports that Southern Companies, SO, announced it is declaring a dividend of 45.5 cents per share, continuing an unbroken string of quarterly dividend payouts for more than 62 years. In April, Southern’s board of directors boosted the dividend rate 4 percent, the ninth year of steady increases. Southern’s dividend yield, the rate at which investors get a return on their money, is 5.14 percent. That compares to an average for the 15 companies in the Dow Jones Utilities Index of 4.4 percent.

The chart of these selected diversified utilities ED, WEC, NU, NI, WR, PEG, and LNT suggests these are approaching the end of their rise. The chart of ED shows a pop with lollipop hanging man candlestick. The chart of WEC shows an ascending wedge pattern. The chart of NU and NI and WR and LNT and PEG all show a double or triple top.

Institutional investors may want to consider investing in the Proshares 200% inverse of the utility stocks, SDP.

It is entirely possible, even likely, that stocks, ACWI, will fall lower as bonds, AGG, lose value. Institutional investors should consider the Morningstar report that The Profunds UKPSX, 200% short Japan, and the Direxion DXRSX, 200% Small Caps have been a consistently good performing bear mutual fund.

II … The Report Shadow Banking, By Zoltan Poszar, Reveals Credit Deflation In The Shadow Liability System And Implies Systemic Risk

A) …. Like forever, the Landesbanks, starved for yield in low-yield Germany, had been buying US home mortgages. Then with the repeal of Glass Steagall Act, both Wall Street and the Landesbanks began securitizing mortgage loans, that is packaging them in CDOs and offering them as highly leveraged investment vehicles. These had spectacular reception which were gobbled up by the German state banks as the rating agencies gave the CDOs and the underlying loans the very best of ratings. Then came the subprime crisis and an explosion of delinquencies on the mortgages followed by a rating downgrade (after the fact) which made the securities impossible to trade. So the Landesbanks took the mortgages off balance sheet and placed them in SIVs; and now are declining to publish details of their investments, as well as the details of the stress tests. This obscurity and opaqueness is the equivalent of a financial black hole at a time when transparency would be most helpful. Tyler Durden of ZeroHedge asks a very important question: Will The Record Plunge In Shadow Liabilities Impair Current Account “Shadow” Deficit Funding And Guarantee A Double Dip?

I believe that the plunge in Shadow Liabilities will be the major contributing factor in a bond market collapse led by US Treasury bonds failing at auction. It is as Nassim Taleb relates: ”We Are Going To Have, At Some Point, A Failed Auction.

Yes, a the pas plunge and continuing plunges in the Shadow Banking Liabilities will result in a liquidity evaporation propelling the world quickly into an age of zero credit, an age where seigniorage for credit will come from a combine of government and financial institutions, which I call Government Finance where only food stamps and strategic needs, such as military operations, will be issued credit.

Mr. Durden writes: “Hot on the heels of our earlier disclosure that the Landesbank stress test passage is either a joke or a scam, comes the knowledge that 6 out of the 14 tested German banks, including Landesbanks, have decide against posting their stress test details, specifically withholding the breakdown of their sovereign debt holdings.

As even the New York Fed acknowledges in its recent paper “Shadow Banking”, by Zoltan Poszar, in which there is a whole section on the critical Landesbank function in the shadow economy, “As major investors of term structured credits “manufactured” in the U.S., European banks, and their shadow bank offshoots were an important part of the “funding infrastructure” that financed the U.S. current account deficit,” the proper functioning of the Landesbanks is crucial to maintaining a stable and efficient market funding structure.

This is actually extremely important, as for years most economists and pundits have considered only the non-shadow banking funding aspect of the massive US current account deficit (a topic most critical now that even the US is embarking on fiscal austerity, and the government sector will be unable to further fund the multi-trillion deleveraging ongoing in the private sector, thus pushing the topic of the current account to the forefront as Goldman did recently). Generically, everyone has always looked at China and Japan as those parties responsible for funding the US Current account deficit. Alas, that is only (less than) half the truth. As the New York Fed suggests, the shadow banking system is likely a more important economic funding factor than even China and Japan combined when it comes to the CA. Which is why the all time record decline of over $1.3 trillion in shadow banking liabilities should be a far greater warning sign than any month to month change in China’s UST purchasing patterns.

Some parts of the “internal” shadow banking sub-system specialized in certain steps of the shadow credit intermediation process. These included primarily undiversified European banks, whose involvement in shadow credit intermediation was limited to loan warehousing, ABS warehousing and ABS intermediation, but not origination, structuring, syndication and trading.

The European banks’ involvement in shadow banking was dominated by German Landesbanks (and their off-balance sheet shadow banks—securities arbitrage conduits and SIVs), although banks from all major European economies and Japan were active investors. The prominence of European banks as high-grade structured credit investors goes to the incentives that their capital charge regime (Basel II) introduced for holding AAA ABS, and especially AAA ABS CDOs. As major investors of term structured credits “manufactured” in the U.S., European banks, and their shadow bank offshoots were an important part of the “funding infrastructure” that financed the U.S. current account deficit.

Similar to other shadow banks, the liabilities of European banks’ shadow banking activities were not insured explicitly, only implicitly: some liabilities issued by European shadow banks— namely, German Landesbanks-affiliated SIVs and securities arbitrage conduits—benefited from the implicit guarantee of German federal states’ insurance.

Of course, none of this should come as a surprise to anyone who has followed the Goldman Abacus scandal in depth: the primary dumb money recepticle of all toxic ABS and CDO exposure was long ago decided to be the German banks, which due to a regulatory arbitrage deriving from Basel II exemptions, and for other various reasons, discussed in the Fed paper, and on which we as well will touch upon in the future, were eager to gobble up any and every piece of structured debt biohazard to be kept on their “shadow” SIVs. After all they are off balance sheet – why worry? Speaking of, we wonder if Europe tested the tens of trillions in underwater assets held by Landesbanks on off-balance sheet vehicles – actually that is rhetorical.

But the issue here is much more nuanced. In essence, the Landesbanks, due to their very explosive holdings, are the German equivalent of our own bankrupt multi-trillion shadow bank extraordinaire: the GSEs – Fannie and Freddie.

Just like our own GSEs warehouse around $7 trillion in “shadow” loans – implicitly guaranteed, but not “really” debt – just ask Larry Summers and Ben Bernanke, with an implicit but not explicit guarantee from the government, so the Landesbanks are in precisely the same position. Yet some could argue that the Landesbanks potentially have a far greater impact on the US economy due to their marginal impact as provider of current account deficit funding, than the GSEs, whose recent function has been merely to house hundreds of billions in securitized delinquent mortgage loans, and thus keep mortgage rates low, preventing an all out collapse of the US economy.

All of this must be kept in mind when considering that according to the most recent Z.1, the collapse in the US shadow economy in the quarter ended March 31, was unprecedented … The decline in shadow banking liabilities (defined as the total shares outstanding in money market mutual funds, the total liabilities of GSEs, total pool securities in the GSE mortgage pool, the total liabilities of ABS issuers, the total amount of securities loaned by funding corporations, the total liabilities of Repo markets, and total outstanding Open Market Paper: all of these can be found in the Z.1) between December 2009 and March 2010 amounted to $1.33 trillion!

The full detail of the collapse in the shadow banking system is presented in the charts below (see article for charts).

The real question one should be asking, instead of the asinine debate over whether the Landesbanks are solvent or not (for the immediate answer, look no further than our own GSEs), is just how much of an impact on US current account funding will the massive deleveraging that is occurring in Germany have?

From its peak of $20.9 trillion in liabilities in Q1 2008, shadow banking has lost $3.8 trillion in liabilities in just the past two years. Indeed, over the same time period, liabilities of commercial banks have increased by $2 trillion. Which means that the Fed has been responsible for plugging the hole: curiously enough, the amount of securities purchased as part of the non-Treasury portion of QE amounts to roughly $1.7ish trillion. Merely a coincidence? In other words, with commercial banks unwilling to ramp up lending activity, and the shadow system vomiting risk each quarter, with a stunning $1.3 trillion flowing out in Q1 alone.”

B) …. Annaly Salvos in SeekingAlpha article NY Fed’s Paper On The Shadow Banking System Of Vast Importance writes:

(Annaly Capital Management, NLY, is a successful financial REIT, providing a valuable financial service)

“For those who missed it (and we had, until we were tipped by James Aitken, thank you very much), a vital paper was posted to the New York Fed’s website in the beginning of the month. “Shadow Banking,” a staff report authored by Zoltan Pozsar, Tobias Adrian, Adam Ashcraft and Hayley Boesky, attempts to explain the so-called “shadow banking” system that developed over the last two decades. The shadow banking system is the financing system that developed in parallel to the traditional banking system.”

“If you are a thinker about such things (and you should be), it is a paper of vast importance. To pick just three reasons why it is valuable: First of all, it puts a number on the size of the shadow banking system (about $20 trillion at its peak in March 2008, but now down to about $15 trillion) and compares it to the size of the traditional banking system (about $13 trillion). It is a market that would be missed if it disappeared. Second, the paper points out that this critical source of credit has no access to the usual governmental backstops like the discount window or federal deposit insurance, and the Fed had to resort to emergency facilities to prop them up. It begs the question of whether the Fed should make these emergency facilities a permanent feature. Third, it is terrifically reassuring that the Fed has the people and the resources dedicated to understanding this feature of the market.”

“But another question remains: What is the Fed doing with this information? To quote Mr. Aitken: “The shadow banking system has contracted by an estimated $5 trillion, and yet the Federal Reserve’s balance sheet has, so far, only increased by $1.2 trillion in response. It is any wonder we still have no credit traction.”

I find the following Annaly Salvos’ article statements insightful: “Over the past decade, the shadow banking system provided sources of inexpensive funding for credit by converting opaque, risky, long-term assets into money-like and seemingly riskless short-term liabilities.” … “The shadow banking system is the financing system that developed in parallel to the traditional banking system.” My comment is that: The shadow banking system in creating credit, that is money, has co existed alongside the sovereign debt central banking system to effect seigniorage. The plunge as seen in the Annaly Salvos’s chart of the shadow banking liabilities vs traditional banking liabilities communicates the end of its seigniorage, and an end of credit, that is money, in the shadow banking system.

Zoltan Pozsar’s Fed Paper is the basis of Tyler Durden’s article Will The Record Plunge In Shadow Liabilities Impair Current Account “Shadow” Deficit Funding And Guarantee A Double Dip?. Mr. Durden writes on the critical Landesbank function in the shadow economy stating: “As major investors of term structured credits “manufactured” in the U.S., European banks, and their shadow bank offshoots were an important part of the “funding infrastructure” that financed the U.S. current account deficit,” the proper functioning of the Landesbanks is crucial to maintaining a stable and efficient market funding structure.”

Like forever, the Landesbanks, starved for yield in low-yield Germany, had been buying US home mortgages. Then with the repeal of Glass Steagall Act, Wall Street began securitizing mortgage loans, that is packaging them in CDOs and offering them as highly leveraged investment vehicles. These had spectacular reception which were gobbled up by the Landesbanks as the rating agencies gave them and the underlying loans the very best of ratings. Then came the subprime crisis and an explosion of delinquencies on the mortgages followed by a rating downgrade (after the fact) which made the securities impossible to trade. So the Landesbanks took the mortgages off balance sheet and placed them in SIVs; and now are declining to publish details of their investments, as well as the details of the stress tests. This obscurity and opaqueness is the equivalent of a financial black hole at a time when transparency would be most helpful. Tyler Durden of ZeroHedge asks a very important question: Will The Record Plunge In Shadow Liabilities Impair Current Account “Shadow” Deficit Funding And Guarantee A Double Dip?

I believe that the plunge in Shadow Liabilities will be the major contributing factor in a bond market collapse led by US Treasury bonds failing at auction. It is as Nassim Taleb relates: ”We Are Going To Have, At Some Point, A Failed Auction.

This will result in a liquidity evaporation propelling the world quickly into an age of zero credit, an age where seigniorage for credit comes from a combine of government and financial institutions, which I call Government Finance where only food stamps and strategic needs, such as military operations, will be issued money to operate.

I think Greenspan had full knowledge of the shadow banking system. Ben Bernanke came along and appraised the situation and seeing the plunge both in the shadow banking system liabilities and the traditional banking systems liabilities, decided to integrate the US banks, KBE, and the too-big-to-fail-banks, RWW, into the central bank via the Fed’s QE TARP Facility. This constituted a financial/banking coup. This “nationalized” the banks, and in the process of capitalizing them with 1.2 Trillion of US government bonds, which now reside as “excess reserves” at the Fed, privatized the nation’s wealth into the hands of the bankers, and socialized the losses of the bank’s toxic debt to the taxpayers.

III … Conclusion

The Irish Times notes that six of the 14 German banks tested – Deutsche Bank, Postbank, Hypo Real Estate, mutual groups DZ and WGZ, and Landesbank Berlin – did not publish the expected detailed breakdown of sovereign debt holdings, fuelling suspicion they had something to hide. Arnoud Vossen, Secretary-General of the CEBS, said it had agreed with all supervisory authorities and with the banks in the exercise that there would be a bank-by-bank disclosure of sovereign risks but officials from the German regulatory authorities – Bafin and the Bundesbank – said local law meant they could not force banks to publish such details.

The Landesbanks are a group of state-owned banks unique to Germany. They are regionally organised and their business is predominantly wholesale banking. They are also the head banking institution of the local and regional bases.

What they are hiding is the great size and plummeting fall of the shadow banking system, that is, the once lucrative seigniorage money creation system, that sprung up from financial deregulation that accompanied the repeal of the Glass Steagall Act, and operated in parallel with the traditional central bank sovereign debt seigniorage system.

The debt deflation of the shadow liabilities, that is those assets kept off balance sheet in SIVs, creates systemic risk as they impair traditional current account deficit funding. The plunge in shadow liabilities that has recently accelerated, will likely be the major contributing factor in a bond market collapse led by US Treasury bonds failing at auction as Nassim Taleb relates, ”We Are Going To Have, At Some Point, A Failed Auction”.

It is the credit deflation of the shadow liability system, identified in “Shadow Banking,” a staff report authored by Zoltan Pozsar, Tobias Adrian, Adam Ashcraft and Hayley Boesky, that could easily make the day of the failed auction come very soon, and the economic dislocation be more severe.

Ezra Klein of the Washington Post in article 5 places To Look For The Next Financial Crisis writes: The Great Depression was visually arresting: long lines of desperate families trying to get their money in hand before the bank collapsed. The financial crisis started out similarly severe, but aside from some despondent-looking traders, there was little to look at. That’s because this bank run wasn’t started by families. It was started by banks.

Regular folks didn’t pull their money out of the banks, because our deposits are insured. But large investors — pension funds, banks, corporations and others — aren’t insured. They use the “repo market,” a short-term lending market in which they park their money with other big institutions in exchange for collateral, such as mortgage-backed securities. This is the “shadow banking system” — it’s a real banking system, but it’s young, and until now largely unregulated. As such, it’s been vulnerable to the sort of problems we ironed out of the traditional banking system decades ago.

When institutional investors hear that their deposits are endangered, they run to get their money back. And when everyone panics at once, it’s like an old-fashioned bank run: The banks can’t pay off everyone immediately, so they unload all their assets to get capital. The assets become worthless because everyone is trying to sell them at the same time, and the banks collapse.

“This is an inherent problem of privately created money,” says Gary Gorton, an economist at Princeton University. “It is vulnerable to these kinds of runs. It took us from 1857, which was the first panic really about deposits, to 1934 to come up with deposit insurance.”

This year, we’re bringing this shadow banking system under the control of regulators and giving them all sorts of information on it and power over it, but we’re not creating anything like deposit insurance, where we simply made the deposits safe so that runs became a thing of the past.

IV … Suggested Reading

Tyler Durden, ZeroHedge article Will The Record Plunge In Shadow Liabilities Impair Current Account “Shadow” Deficit Funding And Guarantee A Double Dip? … and

Ezra Klein of the Washington Post article 5 Places To Look For the Next Financial Crisis … and

Annaly Salvos, SeekingAlpha article NY Fed’s Paper On The Shadow Banking System Of Vast Importance … and

Possner Pinch Minyanville article Liquidity in Economy Never Higher, Yet Banks Growing More Illiquid relates: “Liquidity in the overall economy has never been higher, yet banks are growing more illiquid as they reach for yield. Loans aren’t liquid. Hedge fund investments aren’t liquid. CRE holdings aren’t either. Which leads to some interesting questions. If, as David Merkel suggests (rightly, in my view) that in this day and age monetary policy is synonymous with credit policy, how much looser can policy get? And given the implosion in lending that has happened in this economy, will anyone care?” …. I care because I am concerned the liquidity squeeze could like to liquidity evaporation thereby creating systemic risk ….. and

Andrian Ash, Daily Reckoning article Credit Deflation Lands In Britain relates how the UK is going to recapitalize and re-liquify its financial institutions: “UK banks will soon be able to post raw loans – rather than securitized loans that have been bundled into asset-backed bonds – as collateral against short-term liquidity aid from the Bank of England. This will mean lending central-bank cash against the commercial banks’ major assets. securitization of UK consumer, mortgage and business debt has all but collapsed. Net-net, there haven’t been any sizeable securitizations of UK bank lending for six months running – the longest period since 1998.

The two months before that actually saw securitizations paid back, and at the fastest pace on record, down by £26 billion. Which is a pity for the UK’s formerly go-go-crazy-bones credit bonanza.

In the 10 years ending Dec. 2009, securitization added £325 billion to the growth in UK bank lending, expanding new credit by more than 20%. And why not? Securitizing bank loans, by parceling them up and then selling the debt to investors both foreign and domestic, gave banks the chance to lend the same Pound twice, skimming a profit both times. It also gave insurance and pension funds the chance to invest in Britain’s record debt bubble…a boom which ended with more people working more hours to service more debt than ever before in history.

That bout of collective insanity has now got the DTs. Because second, and as a result of securitization’s collapse (or so we guess here at BullionVault), private-sector UK loan growth overall last quarter did what it’s never done before (not since records began in June 1963, at least) and actually turned negative.

The Bank of England’s decision thus looks timely, if ineffective against the credit deflation already underway.

To repeat: UK bank lending to the private sector has never previously shrunk, not in the 47 years of available data. And lending cash to commercial banks Walter Bagehot-style – albeit by accepting their debtors in turn as collateral, and not charging that “high rate” the 19th-century economist recommended either – is what central bankers are for, after all.

Unlike the Bank’s failed attempt to inject cash into the UK economy via Quantitative Easing, this latest wheeze to underwrite the credit-supply will at least keep the Old Lady’s cash onshore. Because the raw loan’s end-borrower “must be UK-based.” Which should stop the tabloids screaming about “foreigners stealing” this particular chunk of Britain’s monetary easing when it begins.

Whether it stems the UK’s credit deflation remains to be seen. And whether that deflation ever gets to stem the ongoing inflation in prices still awaits history’s verdict, too. Because while private net lending shrank between April and July, quarterly consumer-price inflation meantime rose to 1.3%, knocking 3.3 pence off the purchasing power of each Pound Sterling compared with 12 months prior.

Deflation in credit but inflation in prices? With the fastest GDP growth in four years coming in at 1.1% at market (i.e. unadjusted) prices across the quarter?”

{kind=link}

{kind=link}

Leave a comment