Financial Market report for September 7, 2011

1) … World stocks, ACWI, World Small Cap Stocks, VSS, European shares, VGK, rose, with Small Cap Energy, PSCE, Semiconductors, Semiconductors, XSD, Banks, KBE, Investment Bankers, KCE, Investment Brokers, IAI, Financials, XLF, Insurance, KIE, Coal, KOL, Steel, SLX, Networking, IGN, Smartphone, FONE, Metal Manufacturing, XME, Engineering And Construction, FLM, Energy Service, OIH, Retail, XRT, Small Cap Technology, PSCT, Biotech, XBI, Copper Mining, COPX, Russell 2000, IWM, and Small Cap Industrial, PSCI, leading today’s rally on the German Supreme Court Decision.

Open Europe reports “The German Constitutional Court this morning ruled against the claims that the eurozone bailouts are illegal, providing relief for German Chancellor Angela Merkel and causing markets to rebound slightly. However, the Court stressed that the verdict “should not be misinterpreted as a constitutional blank-cheque for further aid-packages”. The Court also ruled that, in order to conform to the constitution, “the Federal Government is in principle obliged to always obtain prior approval by the [Bundestag] Budget Committee before giving guarantees.” This means that the German parliamentary budget committee will have to agree to any future bailout packages or use of the EFSF, the eurozone’s bailout fund.”

“The ruling looks set to impose further restrictions on Eurobonds or debt mutualisation in the eurozone. The press release states that, “The Bundestag, as the legislature, is also prohibited from establishing permanent mechanisms…which result in an assumption of liability for other states’ voluntary decisions, especially if they have consequences whose impact is difficult to calculate.” … “This seems to suggest that any move towards Eurobonds would be unconstitutional, even with agreement from the Bundestag, though the ruling also hints that greater German control over the fiscal policies of other states that could circumvent such legal restrictions.”

“During a hearing before the House of Commons’ Liaison Committee yesterday, David Cameron said that the eurozone needed to pursue the “logical” step of more fiscal integration to deal with fears over the future of the single currency. When pressed by MPs Cameron did admit that the UK could use any EU treaty change aimed at solving the eurozone crisis, to seek repatriation of EU powers back to the UK. However, Chancellor George Osborne yesterday said, “There’s no immediate prospect of a major treaty negotiation.” Cameron also ruled out the possibility of an in/out referendum on the EU, saying “I don’t actually think that is the question most people in Britain want answering. It is about what sort of Europe. I believe we should deliver the sort of Europe people want.” George Eustice, one of the MPs forming a new parliamentary group pushing for a revised EU-UK relationship, is quoted in the Times, saying that MPs would be “disappointed but not necessarily surprised” by Mr Cameron’s message. A leader in the Times argues that greater fiscal and political integration is looking likely in the eurozone, meaning that the UK will need to clarify its position in Europe, and this should involve “a new constitutional settlement with Brussels that enshrines the principle of British national sovereignty.” Times Mirror Mail Times: Leader

“Die Welt reports that German Chancellor Angela Merkel has suggested that there may need to be a change in EU Treaties to ensure fiscal discipline in the eurozone. She said, “There is no rule so far to force the countries to comply with the Stability and Growth Pact. Therefore, treaty changes must not be a taboo in order to achieve more commitment.” Merkel also reiterated her stance against Eurobonds.”

“The Italian Senate will today vote on the new set of austerity measures proposed by the Italian government to meet the zero deficit target by 2013. In a U-turn from its previous declarations, the Italian government yesterday announced that the package will be put to a vote of confidence, meaning that Senators will not be allowed to amend it. The latest version of the austerity package unveiled yesterday by the Italian government envisages a VAT rise from 20% to 21%, a 3% levy on incomes higher than €300,000 and a gradual increase in retirement age for women working in the private sector, starting from 2014.”

“The Spanish Senate is today expected to give the green light to the introduction of deficit and debt limits in the Spanish constitution. However, El País reports that pro-referendum groups are working to rally the 35 Deputies or 26 Senators needed to require a referendum on the constitutional amendments. Meanwhile, thousands of protesters took to the street yesterday in various Spanish cities, calling for a referendum on the constitutional reform.”

Euro Intellgence in its for fee newsletter reports “Silvio Berlusconi caves in to Mario Draghi with the The Italian cabinet deciding for further austerity measures, most notably an increase in VAT from 20% to 21%, and a 3% surcharge on incomes over €500,000. Reuters reports that the Giulio Tremonti has long resisted a rise in VAT, fearing it would hit consumer demand. Before the ruling by the German constitutional court on ruling on the legality of the EFSF, Süddeutsche.de has an interview with Joachim Starbatty, one of the plaintiffs. The former economics professor refuses to be labelled as an undertaker of the euro, saying the real undertakers are “Mr Trichet and the politicians” because they “always spend money to save countries that are impossible to save”. Starbatty hopes that today’s ruling will erect a wall against all “financial automaticity”. But he says he does not have any illusions about his chances to see the judges declare the EFSF as unconstitutional because the Karlsruhe judges, in his opinion, “are no heroes”.”

2) … Bible Prophecy reveals there are no heroes, only the 1974 Call of the Club of Rome, which serves as basis for the rise of the Beast System of Neoauthoritarianism to rule mankind in its seven institutions and ten world regions.

Nothing has changed because of the German Supreme Court Ruling.

In 1974, the Club of Rome, issued a Clarion Call for a Ten Toed Kingdom of regional economic government as foretold in Daniel 2:27-43. Its Call, in addition to be clear, ringing, and distinctive, carries with it a compelling Authoritarian Imperative for an Authoritarian Regime to replace the Milton Friedman Free To Choose Regime, at a time when the engines of delveraging are decapitalizing banks and destabilizing government. The world in the May through August 2011, passed through an inflection point, and transitioned from Age of Leverage into the Age of Deleveraging, triggering the Club of Rome’s Call.

Bible prophecy of Revelation 13:5-10 foretells that soon out of a global economic collapse, a European Chancellor, that is an Iron Chancellor, will rise to power in the Eurozone. He is seen in Daniel 7:8 as the Little Horn and in 2 Thessalonians 2:8-12 as the Lawless One. He will be accompanied by a European Banker as seen in Revelation 13:11-18. In a new era of bank decapitalization and failed national Treasury Debt Auctions, sovereign debt, seen in the trading of the ETF BWX, will no longer be the basis of seigniorage, that is moneyness. European leaders will announce framework agreements that will waive national sovereignty and establish a fiscal union, with fiscal rules that come with Austerity Measures in an attempt to deal with sovereign crisis.

Throughout history great leaders have emerged. This include Nebuchadnezzar ruling Babylon; Cyrus and Cyrus and Darius ruling Merdo Persia; Charlemagne ruling Rome; Tony Blair ruling Great Britain, and George Bush, The Decider, ruling America with Unilateral Authority. Soon ten kings will come to rule, each in his own regional power base. The coming President of the EU will be one knowledgeable with the scheme of framework agreements. A leading individual for this position is Herman Van Rompuy, as he orchestrated the original Greek bailout.

Out of the soon coming global sovereign debt and banking crisis, a new European Super Government will arise; it will be like a revived roman empire, with the iron of authoritarian diktat replacing the clay of socialist democracy. A new moneyness, will come from the word, will, and way of both the Sovereign and His Seignior. The people will be amazed by this new seigniorage, and follow after the Beast Regime of Neoauthoritarianism, giving it their allegiance, as it rules in all seven of mankind’s institutions and the world’s ten regions as foretold in Revelation 13:1-4. One can read more in Revelation Commentary.

The former Beneficial Regime of Neoliberalism experienced a death rattle in May 2011 when world stocks, ACWI, fell lower, and died when world currencies, DBV, and emerging market currencies, CEW, and commodity currencies, CCX, turned lower in August 2011, and when Angela Merkel and Nicolas Sarkozy effected a bloodless coup d etat, with their Communique a “true European economic government” in August 2011.

Mario Daghi is just one of many dignitaries of this new age. He is an ambassador of the Ten Toed Kingdom of regional economic government. He said in Liz Alderman and James Kanter NYT article European Bankers Urge Leaders To Move Quickly On Debt Crisis, “Europe needs to “make a quantum leap in economic and political integration.” Mr. Draghi’s call goes to the heart of what politicians now acknowledge is a root cause of Europe’s crisis, but that few seem ready to change: the lack of a federal fiscal union that would make the euro zone look more like the United States. The idea is something that Germany and others are wary of because it could undermine their national authority. In Brussels, meanwhile, an unusual gathering of former European leaders, academics and industrialists urged politicians to recognize that part of the answer to Europe’s ills was to give up some sovereignty to keep the euro alive. “It has become clear that a monetary union without some form of fiscal federalism and coordinated economic policy will not work,” the group said in a statement. Its members include a former German chancellor, Gerhard Schröder; a former Finnish prime minister, Matti Vanhanen; and Nouriel Roubini, a New York University economist. “Either the Europeans move forward,” Mr. Roubini said, or face “a situation of potential breakup or disintegration.”

Neoliberalism was characterized by prosperity, privilege, patronage and pork. But, Neoauthoritarianism is characterized by austerity measures. Associated Press Mich. governor signs law capping welfare benefits to 48 months. Love will grow cold in the Age of Deleveraging. For the last ten years, I have been getting around by using the local bus. It is used by the low income, disabled, mentally ill, elderly and infirm. So I see an ongoing daily picture of poverty. Yesterday, I saw a pregnant teenage girl in the “comforting” arms of a teenage boy. I feel genuinely sorry for the young woman. Now is not the time to be with child. This is especially the case for the poor; it takes two to manage the demands of child rearing: especially on the bus, one to carry packages, and the other to manage the stroller. Under Neoliberalism, an envelope from the government provided charity; but under Neoauthoritarianism, a club from sovereign leaders provides austerity and enforces debt servitude.

3) … Will The 1.5 Trillion In Excess Reserve serve to fund integration of the banks with the US Federal Reserve? … Has the world seen the end of a great super credit cycle?

“The September Contrary Investor in article It’s A Long Hard Road relates Monetary Policy Useless In Deleveraging Cycles. Although it appears obvious conceptually, we’re not so sure the markets yet fully appreciate the fact that in true generational deleveraging cycles, monetary policy is powerless to influence credit expansion. Again, our near myopic focus on credit is driven by the fact that credit is the cornerstone of modern economic development and balance, and certainly not just in the US. The character, availability and price of credit regulate the ongoing tone of aggregate demand, so monitoring credit is simply crucial. If credit cannot expand, then neither can aggregate demand. A simple yet key truism, especially in our current circumstances. As you can see below, we’ve seen literally unprecedented monetary expansion so far in the current cycle, yet private sector credit creation (as is exemplified by the bank loans and leases outstanding) remains wildly subdued at best. The whole pushing on a string thesis? Exactly.

The bottom clip of the chart above has been adjusted for the $450 billion of off balance sheet bank loans that were mandated to arrive back on bank balance sheets as per FASB dictates in April of last year. As is clear, bank loans and leases out since early 2009 have declined significantly. The bulls have trumpeted the growth over the last three months. You can decide for yourself whether this minor uptick is deserving of trumpeting, if you will. To ourselves the message appears absolutely crystal clear. In generational deleveraging cycles, Fed monetary policy is simply a non-event. Rather monetary extravagence finds its way into inflation hedge assets and can be used simply to speculate. Remember, as per Fed monetary largesse, the banks are sitting on $1.5 trillion of excess reserves as we speak.

Excess reserves can be used as collateral for derivative and futures trading. You already know trading profits have been a crucial piece of bank earnings since 2009. As of now, monetary policy has been completely ineffective in the current cycle in creating credit – the lifeblood of economic activity and growth – except in one instance. And that instance lies below. Of course we are referring to Government debt.

In typical recessionary periods past, the Fed has been able to lower interest rates and stimulate demand for credit. Demand for credit ultimately stimulates broad economic activity via an increase in aggregate demand. But in deleveraging cycles as opposed to typical business cycles, interest rates can fall to zero and still not positively influence demand for credit. This is exactly what has occurred in the current cycle. You may remember from our discussions over the years we asked one question again and again, “is this a business cycle or a credit cycle?” The only borrower of substance in the current cycle has been the Federal Government, yet we are currently reaching the limits of Government balance sheet expansion tolerance, as clearly witnessed by the debt ceiling melodrama. This has only served to weaken the US as a credit. Again, the inability to generate demand for credit by almost any means (and in our present circumstance historic means) is simply a classic fingerprint of a generational deleveraging cycle.

Never in modern history have we faced the type of domestic labor market circumstances we face today. As we’ve tried to describe, monetary policy is powerless to change this. If Mr. Bernanke was the true student of history he would fully realize exactly the circumstances we’ve described. It’s not that we don’t have precedent. The US in the 1930’s and Japan over the last two decades are the model. Looking at the Depression years and claiming the issue was that the Fed was not loose enough misses the key fingerprint character points of a generational deleveraging cycle completely. Again, the refusal of Bernanke and friends to even acknowledge Austrian or Kondratieff economic constructs has been and will continue to be their policy making downfall. Who knows, maybe all of this will find its way into the economics textbooks of tomorrow. Let’s hope so anyway for future generations. But as the old market saying goes, people don’t repeat the mistakes of their parents, they repeat the mistakes of their grandparents.

Government and Fed policy has been aimed at fostering credit creation up to this point. Fed money printing and Government borrowing has been undertaken in an attempt to stimulate credit creation and likewise spark broad reacceleration in consumption. Certainly Government and Fed actions have also been an offset to the contraction in private sector (think financial sector) credit so far in the current cycle. As of now, unprecedented Fed actions have acted to both devalue the dollar and suppress interest rates. But in a generational deleveraging cycle, the Fed is ultimately impotent in terms of being able to successfully spark private sector credit creation that would lead to expansion in aggregate demand and macro GDP growth.

But what has occurred as a result of Fed and Government “solutions” again is a classic macro deleveraging cycle response – a devalued currency and negative real interest rates has driven investors into inflation hedge assets such as gold, oil, ag assets, etc. at the margin. As opposed to having achieved the stated goal of fostering employment growth, credit creation and raising aggregate demand, etc., Fed QE has essentially succeeded in raising the cost of living in a cycle characterized by generational labor market and direct wage pressure among the middle and lower class wealth demographic. From a broad perspective, has Fed and Government policy actually done more harm than good? It simply depends where one sits amidst the wealth demographic pyramid of life. Policy has been fabulous for Wall Street and the banks, but not so fabulous for the average household. The average household has faced vanishing interest income and negative real wage growth amidst an environment of a meaningfully rising cost of every day living (food and energy prices).

Policy has been counterproductive because policy makers continue to focus on short term outcomes as opposed to longer term structural remedies. Remember, people repeat the mistakes of their grandparents, not their parents. Mr. Bernanke is apparently an “expert” on the actions of “grandparents”, yet he is very much repeating their same mistakes by his implicit refusal to even consider Austrian/Kondratieff like economic ideas. You already know, THE key character point of successful investors over time is flexibility in outlook and behavior. It’s just a shame we can’t clone that character point inside the Fed and Administration at present. But of course that would be counterproductive to the interests of Wall Street and the big banks.”

To their report, I add that the Fed’s ZIRP and quantitative easing policies have stimulated commodity speculation thereby increasing manufacturing costs.

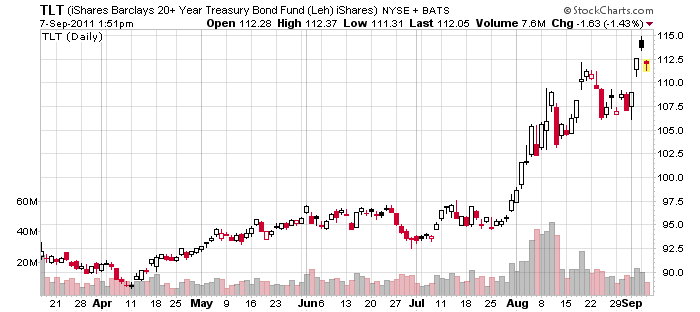

4) … I believe that the increase in the “money supply” is due to the rise in value of US Treasuries, TLT. The likely evening star in the chart of TLT suggests that the world is passing through Peak Credit.

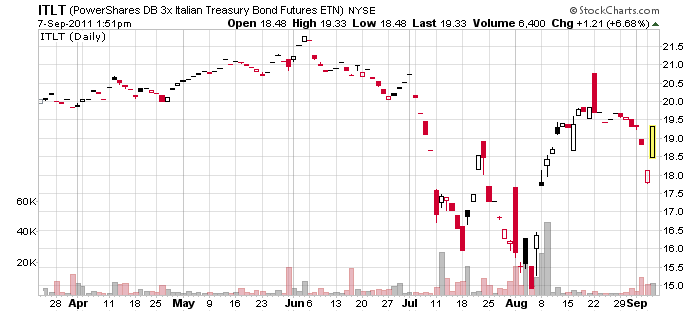

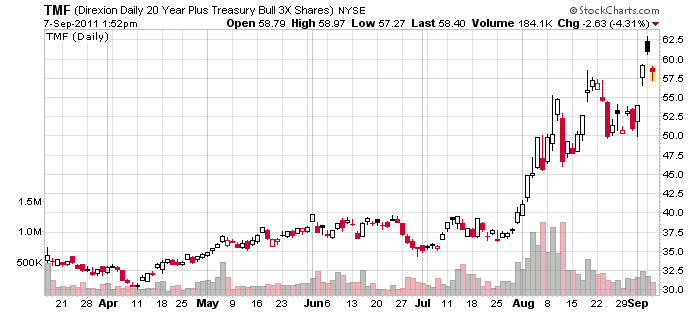

5) … ITLT is an investment that is going to be more quickly deleveraged than TMF.

Chart of TMF

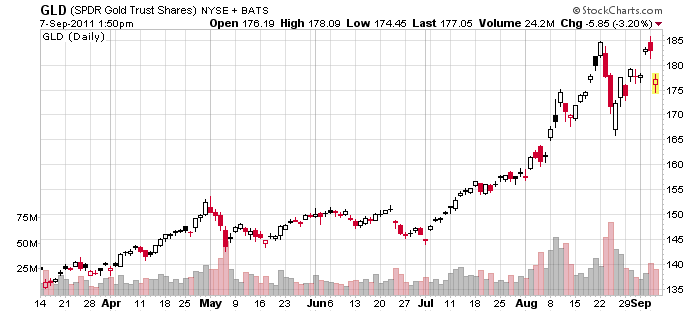

6) … Gold is a currency; it fell lower today, in sympathy with the fall of other currencies and the rise of the US Dollar. It still has a long way to rise in value.

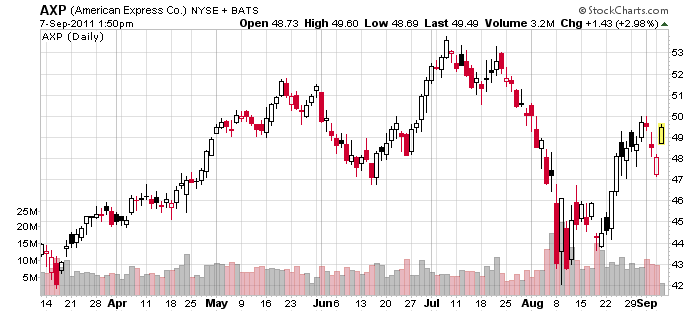

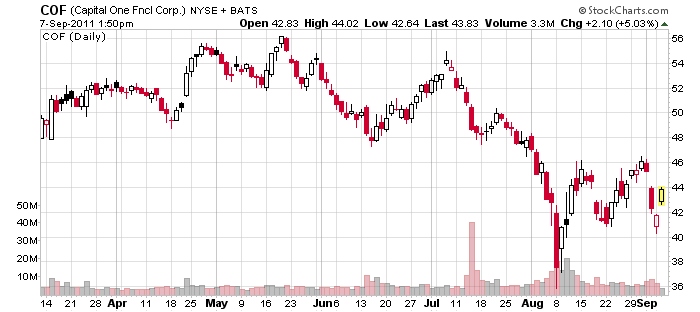

7) … Under Neoauthoritarianism, with the exception of payday lenders, not only will banks be integrated with the government, but credit suppliers, such as American Express, AXP, and Capitol One Finance, COF, will be as well.

Chart of AXP; it rose today to the middle of a broadening top pattern; as Street Authority communicates, when you see the broadening top, the market will eventually drop.

Chart of COF

8) A Global Eurasia War is coming

Business Insider reports UN Security Council Finds Iran is Violating The Nuclear Weapons Program Ban.

Leave a comment