Financial Market Report for February 25, 2011

1) … A Framework Agreement … Is A Framework Agreement, Olli Rehn relates.

Open Europe reports daily briefing Fine Gael Could See First Ever Outright Majority In Irish Elections: “As Irish citizens head to the polls today, the FT notes that the opposition Fine Gael party is set to win its first-ever outright majority, in what would be the first defeat for a eurozone government since the beginning of the debt crisis. The new government is expected to try to re-negotiate the terms of the €85bn EU/IMF bail-out. However, the Irish Times quotes a spokesperson for EU Economic and Monetary Affairs Commissioner Olli Rehn saying, “This agreement, it’s an agreement between the EU and the Republic of Ireland. It’s not an agreement between an institution and a particular government. It’s on the basis of a negotiated programme which was approved with the government of Ireland and which in its main outline has to be applied.”

“An article in the Independent notes, “Worries abound that [Fine Gael leader Enda] Kenny lacks the charisma, economic savvy and plain old guts to dig the nation out from under a mountain of debt and renegotiate the IMF and European Union bail-out.” In the Times, Julian Gough argues, “Fine Gael also mistook the bubble for prosperity, also voted for the disastrous bank guarantee and doesn’t seem to have any idea how to renegotiate the terms of the IMF/EU bailout in any meaningful way.” A leader in the Telegraph argues that a change of government would not be a sufficient solution to Ireland’s problems, noting: “The Irish have preferred to vent their anger at the polls rather than on the streets. But while they remain in the euro, a new government will make little difference to their predicament.” FT Guardian Times: Gough Telegraph: editorial Irish Times: editorial Irish Times Independent Independent 2 EUobserver BBC: Today

Olli Rehn, EU Economic and Monetary Affairs Commissioner, in communicating the week ending February 25, 2011 that “This agreement, it’s an agreement between the EU and the Republic of Ireland. It’s not an agreement between an institution and a particular government. It’s on the basis of a negotiated programme which was approved with the government of Ireland and which in its main outline has to be applied,” announced an important truth: the Irish Bailout Agreement between Ireland, the EU and the UK is a Eurozone Framework Agreement that established European economic governance and provided resolution to Ireland’s debt issues. The leaders in announcing the framework agreement waived national sovereignty, and strengthened a region of global governance, that was established by the previous bailout agreement with Greece. These two framework agreements, plus the one that established vetting of national budgets before they are presented to national legislatures, established the Eurozone as one of ten regions of global governance as called for by the Club of Rome in 1974. The people of Ireland, and the whole world, if they do not know already, will come to know that there will be no voting on the issue of Ireland’s debt. They are going to learn very shortly that there are not sovereign, rather the leaders, their word, will and way are sovereign. Welcome to the age of global governance manifesting in regional economic governance.

Bruno Waterfield in the Telegraph article Ireland’s New Government On A Collision Course With EU

reports: “Enda Kenny, Fine Gael’s leader, will later on Sunday, start to form a new government, almost certainly with Labour, after full election results under Ireland’s complicated PR system come through.”

“Both Mr Kenny and Eamonn Gilmore, Labour’s leader, have promised Irish voters that they will renegotiate the EU-IMF austerity programme to reduce the burden for taxpayers and to force financial investors to shoulder some of the bank debts currently paid out of the public purse.”

“At a summit of centre-right EU leaders in Helsinki next Friday, Mr Kenny will use his position as Ireland’s new Prime Minister to beg the German Chancellor, Angela Merkel, and French President, Nicolas Sarkozy, for concessions ahead of an emergency March 11 Brussels summit to restructure the euro zone.”

“But neither the two European leaders nor the European Central Bank or EU will permit any substantial changes, despite the huge popular Irish revolt against the bailout.”

“Chancellor Merkel will tell Mr Kenny that if he wants to reduce the high, punitive 5.8 per cent interest rate charged on EU loans then Ireland will have to give up its low corporate tax rates – a measure regarded as vital to Ireland’s recovery and one of the few economic policies it has not yet handed over to Brussels or Frankfurt.”

“The new Irish premier will also be warned that there is no question of forcing privately-owned financial institutions to assume Ireland’s £85 billion bank debts because the resulting market panic would spread to Germany and France, tearing the euro single currency apart.”

“As Irish voters headed for the polling booths on Friday, the European Commission bluntly declared that the terms of the EU-IMF bailout “must be applied” whatever the will of Ireland’s people or regardless of any change of government.”

“It’s an agreement between the EU and the Republic of Ireland, it’s not an agreement between an institution and a particular government,” said a Brussels spokesman.”

“A European diplomat, from a large eurozone country, told The Sunday Telegraph that “the more the Irish make a big deal about renegotiation in public, the more attitudes will harden”.

“It is not even take it or leave it. It’s done. Ireland’s only role in this now is to implement the programme agreed with the EU, IMF and European Central Bank. Irish voters are not a party in this process, whatever they have been told,” said the diplomat.”

Shaun Richards writes Election Day In Ireland: “This morning voters in the Irish Republic will take to the ballot box and cast their votes in a general election. After the economic “perfect storm” that has hit their country they do need a change and I hope that it will show that the ballot box as well as the gun and revolution can lead to fundamental change. As we stand in spite of the “rescue” from the EU/ECB/IMF then Ireland looks insolvent as she goes forward. Her government bond market has if anything deteriorated since the date the “rescue” was announced. As I type this her ten-year government bond yield is 9.46% which we can compare with seriously troubled but unrescued Portugal at 7.64% or the UK at 3.72%. If you compare the relative situations then it is plainly unfair that Ireland has a rate 6% higher than that of the UK as there are as many similarities as differences. Regular readers will be aware that I often argue that the shorter end of the maturity spectrum also gives us insight into a country’s finances and here we find a bond maturing in April 2013 which yields 8.03% which to my mind has even worse implications than the ten-year yield. For those to whom this is unfamiliar you can learn a lot from what is called a yield curve but my point here is that the revealing part is the gap between the official central bank rate (1%) and a yield of 8.03%. Thus in two years the gap is over 7%!”

“What does this mean for the Euro zones concept of a rescue? It means that the “rescue” is not far off an utter failure. If we look again we see that to April 2013 investors want a yield of 8.03% when repayment is in effect guaranteed by the rescue plan. Behind the rescue plan we have the European Central Bank, the European Union and the International Monetary Fund. As they are willing to loan money to Ireland at around 6% (it was announced at 5.8% but rates have risen since then) I am surprised that more commentators have not raised this point. If it was perceived to be a success then Irish government bond yields should have headed towards 6%. In fact they have headed away from it!”

“We are back to the theme that you cannot solve a solvency problem with liquidity and until Europe’s leaders cotton onto this point there will be little improvement in Ireland’s fortunes. Also please remember that these higher bond yields for Ireland come in spite of the fact that the European Central Bank has been willing to buy these bonds to support the market and could do so again. Accordingly we do not know what the fair market price is and we can put another chalk mark on the scoreboard of false markets created by central banks. I regularly argue that such intervention is mostly beyond their abilities and skills and yet again we can see that in the words of the song there are “more questions than answers”. Sadly we seem likely to get more of this type of intervention rather than less as many central bankers appear unaware of the damage they are doing. When I read the speech of David Miles who is on the UK Monetary Policy Committee I was struck by the image of a man who felt that events happened to him and yet in terms of UK history the Bank of England has been extraordinarily interventionist. I doubt whether he appreciates the irony of this or the fact that the events he feels he is suffering from may be “feedback” from his wn actions, if we look for a song for central bankers may I suggest the lyric, “Reality was once a friend of mine”.”

Martin Wolf in Financial Times writes in article Ireland Needs Help With Its Debt: This is not one, but three, crises: an economic collapse; a financial implosion; and a fiscal disaster. On the first, given the fall in demand and the need for fiscal contraction, prospects for recovery depend heavily on exports. On the second, the direct costs of recapitalising the system are set to be around 36 per cent of GDP, according to Goodbody stockbrokers. On the last, according to the IMF, general government debt could be 123 per cent of GDP by 2014. A little over a third of this increase in the public debt ratio would then be a direct result of recapitalising the banks.

Such a crisis is beyond the ability of Ireland to manage without financial collapse and sovereign default.

Apart from the Armageddon of a sovereign default, two partial escapes exist. The more torivial would be a reduction in the rate of interest on Ireland’s borrowing: a 1 per cent reduction in the rate of interest would save the state 0.4 per cent of GDP a year. That would be a small help, at least. A more valuable possibility would be a writedown of existing subordinated and senior bank debt, which currently amounts to €21.4bn (14 per cent of GDP).

The ECB and the other members of the European Union have vetoed this idea, fearful of contagion. Indeed, the assistance package was partly to prevent just such an outcome. Yet the idea that taxpayers should bail out senior creditors of massively insolvent banks at such risk to the solvency of their state is both unfair and unreasonable. If the rest of the EU is determined to protect senior creditors, it should surely share in the cost of doing so. Why should the taxpayers of the borrowing country pay all? The new Irish government should make this point firmly.

2) … Germany breaks out in open revolt against the European Bailout

EuroIntelligence reports subscription article Germany In Open Revolt Against European Bailout. Academics and businesses are joining Bundestag and Bundestag in protests against proposed extension of the eurozone’s rescue mechanism. This is a very serious situation in our view, on the verge of getting out of control. The conservative establishment is in open rebellion against a weak government about to face a string of electoral defeats. Frankfurter Allgemeine Zeitung, published a Petition of 189 German economists which called on the German government to refuse any extension of the EFSF, and to force highly indebted countries into an insolvency procedure. They include some of the best known German economists – Hans Werner Sinn, Jürgen von Hagen, Manfred Neumann, Michael Burda and Volker Wieland. They make the following points:

1. A permanent credit guarantee for insolvent countries would provide “massive incentives” to repeat the mistakes of the past. The reforms of the stability pact, and the newly discussed pact for competitiveness, are too weak to counteract this.

2. A long-term strategy against debt crises requires the possibility of a sovereign insolvency.

3. Credits to countries should be possible, but only after debt restructuring.

4. The fact of state insolvency should be determined not by the country itself, but by an international institution, such as the IMF.

5. The ECB must not provide unlimited support of insolvent countries through bond purchases.

6. Of the three solutions to a national debt crisis – debt reduction through growth, insolvency, and bailout-the latter would imply higher taxes, and/or higher inflation.

Holger Stelzner, the openly anti-European editorialist of Frankfurter Allgemeine Zeitung, writes that the eurozone is drowning in its debt, which has turned the ECB into a bad bank. The approach of policy makers everywhere is to solve a debt crisis through more debt. The increase in the ECB’s balance sheet from €900bn to €1800bn of mostly low quality debt was immensely risky. The ECB is no longer an independent institution, but an interested party.

Papandreou tells Bild that Greece will not sell its islands. In today’s Bild there is an interview with George Papandreou, who promised to pay back every cent and emphasised that this is a loan, not a transfer: “These are loans and we are paying interest on it, these are not gifts.” When asked about whether Greece would be ready to sell its islands, he responded: “You΄ve simply got to understand how important these islands are for Greece and Greek history. We΄ve spent enormous sums in defence budgets to secure the islands near the Turkish coast.” (Hat tip from “Keep talking Greece”, a Greek blog in English covering the crisis).

3) … The US Dollar reaches a crossroads as world currencies manifest dramatic candlesticks.

The US Dollar, $USD. closed at 77.23. at the edge of support at the edge of a massive head and shoulders pattern.

The US Dollar may continue to bounce up February 28, 2010; and a large number of the world’s currencies, seen in this chart of FXY, FXF, SZR, FXE, FXB, FXS ,ICN, FXA, BZF, BNZ, FXM, FXC ,BZF, and CEW, may fall lower, as FX currency traders renew their global currency war against the world central bankers, in a new round of competitive currency devaluations, that is competitive currency deflation. One can use this Finviz Screener to create a portfolio of currencies to track currencies.

The other scenario will be for the US Dollar, to collapse through its current base of 77; but I really think the US Dollar will continue to bounce higher before doing so.

The US Dollar, $USD, is traded by the 200% ETF, UUP, which shows a death cross on February 18, 2011, as well as the start of an Elliott Wave 2 Down on January 10, 2011, as FX currency traders have successfully sold off the dollar illustrating the principle that monetization of debt, that came by QE 2, debases the US Currency.

The Australian Dollar, FXA, and the Canadian Dollar, FXC, are most strong currency. Do I foresee a fall? Anywhere close to the June 2010 fall? I have no idea. I do expect a fall in the US Dollar, as monetization of debt eventually leads to currency destruction and debasement.

4) … The bear market of all bear market commenced on February 22, 2011.

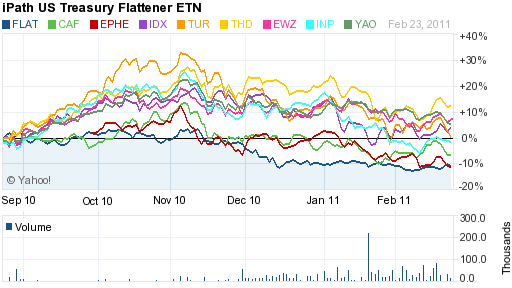

Printing of money out of thing air by a central bank for what reason, always results in not only the currency being destroyed but also the stock market assets of that country being destroyed. Quantitative easing quickly and awesome drove up investment in the Philippines, EPHE, EPHE, China, YAO, India, INP, Indonesia, IDX, Turkey, TUR, Thailand, THD and Brazil, EWZ. But the first announcement of QE2 at Jackson Hole, inflation destruction commenced and destabilized all highly inflationary countries, as is seen in the chart of EPHE, YAO, INP, IDX, TUR, THD, and EWZ. According to Urban Dictionary, inflation destruction is the fall in investment value that accompanies derisking and deleveraging out of investments that were formerly inflated by money flows to, and carry trade investing in, high interest paying financial institutions, profitable natural resource companies, and high growth companies.

Coal miners, KOL, have lost more investment value than copper miners, COPX, with Arch Coal, ACI, and ANR Resources, ANR, being prime examples. Other QE exhausted investments include Pharmaceuticals, XPH, Nasdaq Biotechnology, IBB, S&P Biotechnology, XBI, Las Vegas Sands, LVS, Brazil Financials, BRAF, Airlines, FAA, Shipping,SEA, and Manufactured Housing, CVCO as is seen in the chart of CVCO, FAA, SEA, XPH, XBI, IBB and KOL.

Risk appetite turned to risk avoidance in the emerging market countries as quantitative easing exhausted and money flowed out of these formerly hot markets.

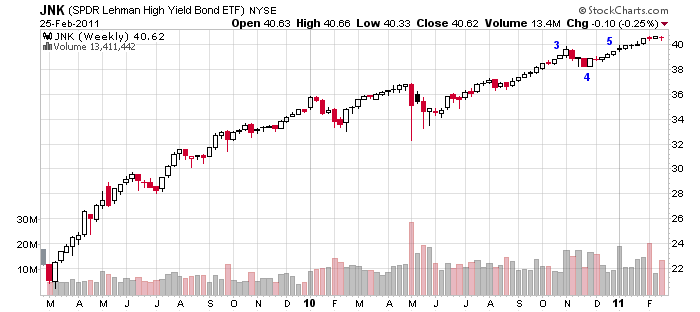

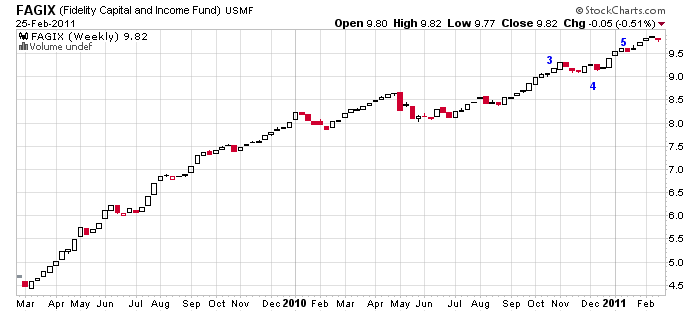

Volatility continued to decrease as the value of Ben Bernanke’s seigniorage, that is distressed securities, FAGIX, and junk bonds, JNK, rose in value.

While these early beneficiaries of quantitative easing deflated, the seigniorage of QE2 continued strong in major countries such as the US, IWO, Germany, EWG, South Korea, EWY, and Taiwan, EWT, as is seen in the chart of EEM, IWM, EWG, EWY, and EWT. But recently as the chart shows, the Asian Tigers are starting to experience inflation destruction. And this despite the Chinmei Sung Bloomberg report: “Taiwan’s industrial production rose for a 17th straight month in January, supporting the case for policy makers to raise borrowing costs further next month. Output advanced 17.19% from a year earlier, after gaining a revised 18.93% in December”.

And while the early beneficiaries of quantitative easing deflated, the moneyness of QE2 continued strong in the Small Cap Pure Value, RZV, the consumer discretionary, XLYS, the Nasdaq 100, QTEC, the Russell 2000 Growth, IWO, the Internet Retailers, HHH, Semiconductors, XSD, the Metal Manufacturers, XME, the Dow Energy Service, IEZ, and the Small Cap Energy Shares, XLES, as is seen in the chart of EEM, RZV, XLYS, QTEC, IWO, HHH, XSD, XME, IEZ, XLES.

But seigniorage failed February 22, 2011 as World Stocks, ACWI, World Currencies, DBV, and Emerging Market Currencies, CEW, turned lower, as quantitative easing exhausted.

Failure of seigniorage comes from the fall lower in distressed investments, like those in mutual fund, FAGIX, which constitute a large part of the US Federal Reserve’s balance sheet, and which trade like Junk Bonds, JNK, served to underwrite the recovery of the last two years.

Weekly Chart of Junk Bonds, JNK, shows a rise from 22 to 40 since Ben Bernanke established his global seigniorage.

Weekly Chart of distressed investments, FAGIX, shows a rise from 4.5 to 9.5 since Ben Bernanke established QE2. The current monetary order has been built upon one man’s seigniorage of distressed investments.

Also the turn lower in junk bonds, JNK, from its recent high, and a topping out in world government bonds, BWX, serves as evidence to the end of US central bank seigniorage. Failure of seigniorage is also sen in the ratio of US Stocks, VTI:TLT, relative to US Government Note, and in the ratio of world stocks relative to world government bonds, VT:BWX, both turning lower. Without seigniorage world stocks, ACWI, will fall precipitously world wide. And economic expansion will turn to economic contraction.

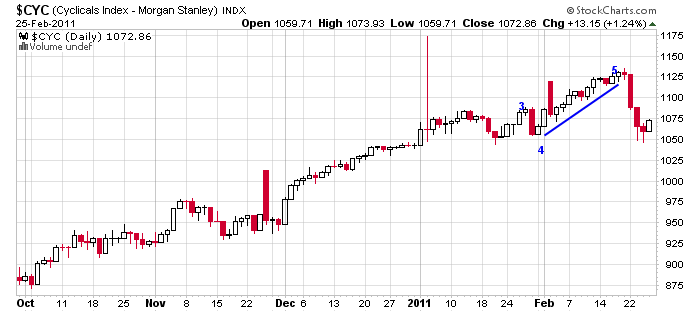

The Morgan Stanley Cyclical Index, $CYC, fell lower; its fall communicates an end to the current growth cycle. Given that this growth cycle, and the rise in the Morgan Stanley Cyclical Index, came via the extreme use of the seigniorage of QE, its reasonable to believe that there will be a dramatic fall lower in stock value, and very soon a downturn in economic reports such as Capitol Goods Orders, Industrial Production, Exports, and Bloomberg Financial Conditions Index, as quantitative easing continues to exhaust, effecting deleveraging both in stock market value and in economic activity as well.

The fall lower in the Industrial stocks, IYJ, comes at the same time as the fall lower in the Transportation stocks, IYT, and communicates the Dow Theory principle that a bear market has commenced — as industrial stocks and transportation stocks make market turns together.

This bear market will be the bear market of all bear markets, as the seigniorage of the long enduring Milton Friedman Free To Choose Currency Regime developed over the last forty years has failed.

The where-with-all since the last financial collapse, that is the subprime collapse, has come via quantitative easing 1 and quantitative easing 2. The seigniorage, that is the moneyness, came via an asset swap, where Ben Bernanke, traded out money good US Treasuries for distressed securities, like those traded by mutual fund FAGIX. For the most part, then the banks placed the US Treasuries into Excess Reserve with the US Federal Reserve. The distressed investments, and the Excess Reserves have been the great springboard of investment growth, but now stocks globally have failed.

The snap declines in leading sectors document that a bear market has commenced.

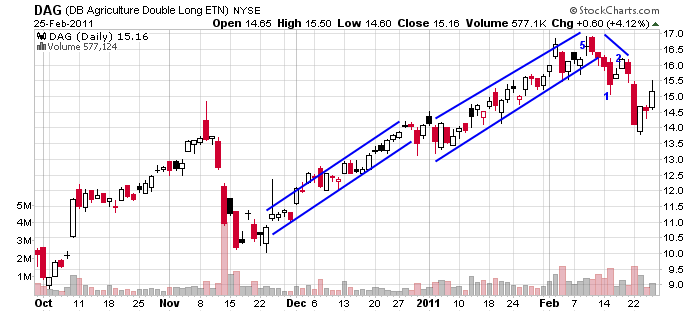

Furthermore, the dynamics in the charts of the 200% ETNs, and ETFs, give clear, cogent, and convincing evidence that a market turn has occurred: Agriculture, DAG, Russell 2000, URTY, Utilities, UPW, and Semiconductors, USD.

The chart of Base Metals, DBB, clearly shows a turn lower; turning global industrial metal miners, such as Companhia Vale do Rio Doce, VALE,

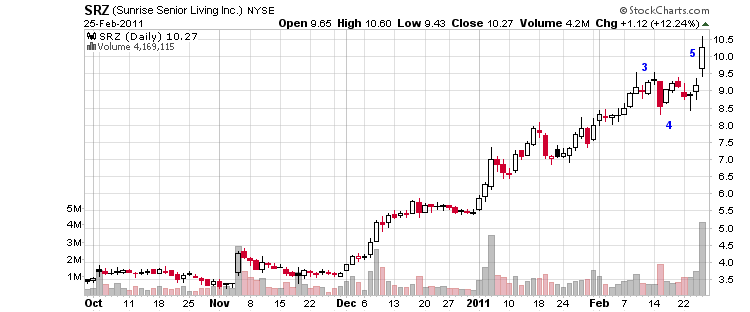

The chart of Sunrise Living, SRZ, gives a finale salute to the Age of Leverage that came through US Central Bank Seigniorage as well as Yen Carry Trade Investing courtesy of the Bank of Japan.

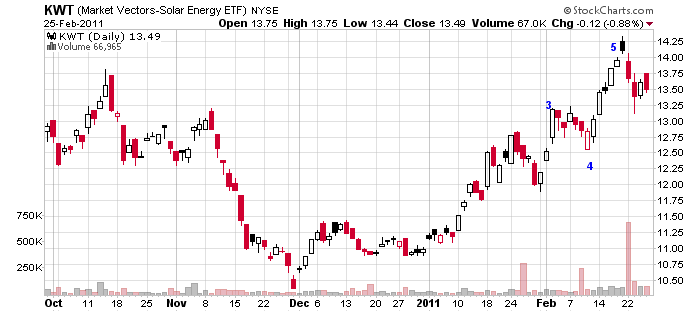

On a day when most stocks rallied, Solar Stocks, KWT, fell lower. All of following solar stocks will be fast fallers in the Age of Deleveraging: Trina Solar, TSL, SunPower Corp, SPWRA, GT Solar, SOLR, LDK Solar, LDK.

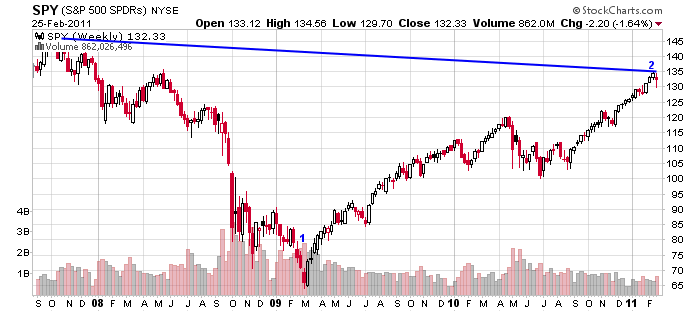

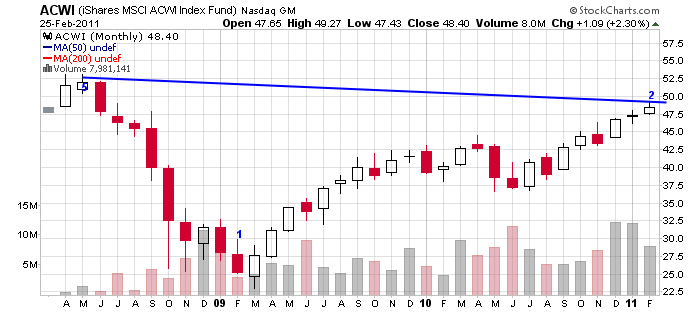

The chart of the S&P Weekly, SPY Weekly, as well as World Stocks Weekly, ACWI Weekly, both show that an Elliott Wave 3 Down has commenced in each; with the S&P, SPY, falling to 130.93 and the World Stocks, ACWI, falling to 48.97.

The chart of world stocks daily, ACWI, is most telling; it shows the three white soldiers patten rise to a value of 49.24, suggesting a reversal of rally is at hand.

The chart of world stocks monthly, ACWI, shows February 2011’s 2.3% gain cresting up into an Elliott Wave 2 High and ready to enter into an Elliott Wave 3 Down. The 3 Waves are the most dramatic and sweeping of all; they build the bulk of the wealth on the way up and destroy practically all the wealth on the way down. What is coming is total destruction of all fiat wealth. The world entered into Kondratieff Winter on February 22, 2011.

5) Bonds rose as stocks topped out and turned lower, giving confirmation that a bear market has commenced.

For the last eleven trading days, the notational value of Bonds, BND, rose as world stocks, ACWI, topped out and turned lower.

This as Sapna Maheshwari and Ashley Lutz of Bloomberg report: “U.S. company bond sales tumbled 74% this week to the lowest in 2011 as growing tensions in the Middle East shook markets. McKesson … led companies selling $5.69 billion of debt, the least since the week ended Dec. 31 … That compares with $21.8 billion of issuance in the five days ended Feb. 18.”

Allan Swanoski writes in Top News: “After mounting for the last four months, the 2-10-year yield curve has been flattening for most of the month. The curve was currently at two hundred and seventy three basis points, the flattest since Jan. 13.”

The chart of Bonds, BND, shows a crest up into an Elliott Wave 2 Completion and ready to commence into an Elliott Wave 3 Down. Similar wave structure is found in most all bonds: BND, LQD, BLV, PICB, BWX, EDV, TLT, IEI, JNK, MUB, CMF, MBB, SHY, BAB, BABS, IEF, TIP, ZROZ, MINT,

Failure of seigniorage means that both bonds, BND, and stocks, ACWI, will be falling lower together. I fully expect the 30 10 Leverage Curve, $TYX:$TNX, which is the inverse of the 10 30 Yield Curve, which has steepened since the beginning of the February 2011, to now begin to flatten once again, deleveraging investments even more out of the longer duration US Government bonds.

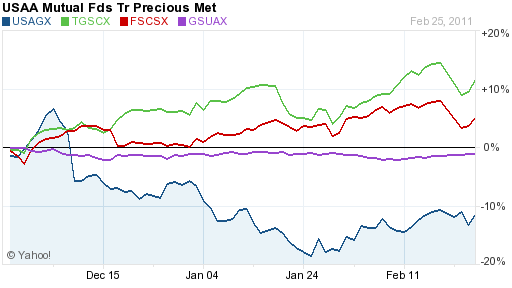

The chart of the 30 10 Leverage Curve Monthly, $TYX;$TNX Monthly, shows the dramatic leverage that has come to investors in stock mutual funds and bond mutual funds, like GSUAX, since the War On Terror was declared and since Alan Greenspan, the czar of credit liquidity, lowered interest rates.

It was the HUI Precious Metal, ^HUI, investors who rode the leverage curve up in mutual funds such as USAA Precious Metals, USAGX. But now even the best of breed mutual funds such as TCW Small Cap Growth TGSCX, and Fidelity Select Software and Computer, FSCSX, are coming under inflation destruction as Quantitative Easing has failed as is seen in the USAGX, TGSCX, and FSCSX

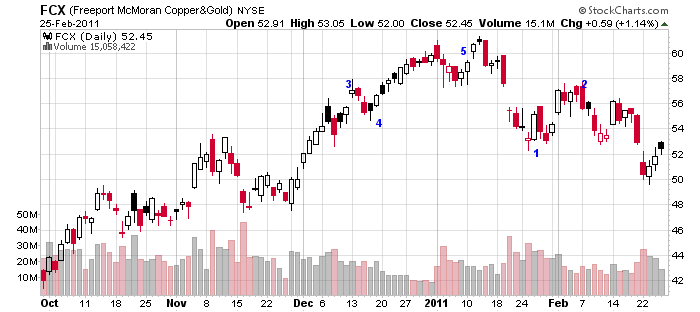

The chart of the gold mining stocks relative to gold, GDX:GLD, shows that gold mining stocks disconnected from the price of gold and fell lower with other stocks this week. The age of profitably investing long in gold mining stocks, GDX, and the junior gold mining stocks, GDXJ, as well as exploratory silver mining stocks, such as Silver Standard Mining Resources, SSRI, is done and over. Tremendous amounts of yen carry trade lending, obtained at 0.25% to 0.50% interest from the Bank of Japan and its lending partners on Wall Street and in London’s Financial District drove Silver Standard Mining Resources, seen in this chart, up over the years. But now, the chart of the Optimized Carry Trade ETN, ICI, shows it too has turned lower in an Elliott Wave 3 Down. Lacking support from US Central Bank seigniorage as well as carry trade lending from the bank of japan, the great growth stocks such as Freeport McMoran Copper and Gold, FCX, as well the copper mining stocks, COPX, as well as BHP Billiton, BHP, are doomed to fall lower and lower. The chart of FCX shows that it has risen to the middle of a broadening top pattern.

The Senators who approved the repeal of the Glass Steagall Act, and The Fed Chief Ben Bernanke remind me so much of The Cat In The Hat, come alive, that is the Dr. Seuss Character who wearing a tall, red and white-striped hat and red bow tie, who led the children in a riotous party. Will the character in today’s real life story, be able to put our economic house in order, as the bond vigilantes and the currency traders make further inroads?

6) … Canada And US Leaders announce a framework agreement for perimeter security and economic competitiveness.

On February 4, 2011, The Prime Minister of Canada website released the Declaration by the Prime Minister of Canada and the President of the United States of America of a framework agreement for Perimeter Security and Economic Competitiveness.

And also on February 4, 2011, The Prime Minister of Canada website released the the announcement of another framework agreement establishing The Bilateral Regulatory Cooperation Council, RCC.

The Canadian Civil Liberties Association relates that on February 4th, 2011, Canada and the US issued the “Declaration on a Shared Vision for Perimeter Security and Economic Competitiveness”. The Declaration commits both countries to create a North American Security Perimeter – where borders will be kept “open” to legitimate travelers and trade, and “closed” to criminals and “terrorist elements.” Four key areas will be pursued: (1) addressing threats early, (2) economic growth and jobs, (3) integrated cross-border law enforcement, and (4) critical infrastructure and cyber-security. Prime Minister Harper stated that “shared information, joint planning, compatible procedures and inspection technology will all be key tools”. Economic gains are supposed to be realized by removing regulatory barriers, harmonizing rules and reducing border congestion for manufacturers.

Luiza Ch. Savage of The Bilateralist provides the Text Of Obama-Harper Border Declaration

The North American Continent was announced as a region of global governance at Baylor Baptist University by the leaders, Vincent Fox, Paul Martin and George Bush, with the Security and Prosperity Partnership of North America on March 23, 2005, with documentation as follows: ..…. Baylor TV Coverage Of The Trilateral Summit News Conference …… President Meets With President Fox and Prime Minister Martin At Baylor University Waco, Texas …… Baylor Has a Proven Record of Hosting White House Events.

Thus, Baylor served as host for President Bush’s historic “Security and Prosperity Partnership for North America” meeting with Mexican President Vicente Fox and Canadian Prime Minister Paul Martin. The Armstrong Browning Library was the venue for the leaders’ meeting, which was followed by a news conference in the Bill Daniel Student Center’s Barfield Drawing Room.

Andrew Gavin Marshall writes in Global Research.ca article Security and Prosperity Partnership of North America (SPP): Security and prosperity for whom? “A new task force, called the “Independent Task Force on the Future of North America” in conjunction with the Mexican Council on Foreign Relations and the U.S.’s most powerful think tank, the Council on Foreign Relations (CFR), founded by the Rockefeller and Morgan families in 1921.”

“This task force released a statement on March 14, 2005 entitled, “Trinational call for a North American economic and security community by 2010.” In the Trinational Call, it was recommended that the North America nations create “a community defined by a common external tariff and an outer security perimeter,” and to “harmonize” the areas of energy, security, education, military, immigration, resources, and the economy.”

“Nine days after this recommendation was issued, Bush, Martin, and Fox signed the Security and Prosperity Partnership of North America (SPP), and in the joint statement explained it would, “implement common border security and bioprotection [enhanced surveillance] strategies, enhance critical infrastructure protection, implement a common approach to emergency response, implement improvements in aviation and maritime security, combat transnational threats, enhance intelligence partnerships, promote sectoral collaboration in energy, transportation, financial services, technology, and other areas to facilitate business, [and] reduce the costs of trade.” The SPP agreement oversees the creation of SPP “working groups” in each country, which have a mandate of overseeing “harmonization,” or “integration,” in over 300 policy areas.”

“In January of 2006, the Council of the Americas and the North American Business Council issued a report titled, “Findings of the Public/Private Sector Dialogue on the Security and Prosperity Partnership of North America,” which called for the establishment of a “North American competitiveness council” to advise governments on the implementation of ‘deep integration.’ The press release (which can be found at spp.gov, “Report to Leaders August 2006”) announced the formation of the North American Competitiveness Council (NACC), which “provides a voice and a formal role for the private sector” whose job is to advise the SPP ministers in their respective governments. Current Canadian SPP ministers are Maxime Bernier (Foreign Affairs), Jim Prentice (Industry) and Stockwell Day.”

“The NACC is run out of the U.S. Chamber of Commerce and with the Council of the Americas, and is made up of corporate leaders from each of the three countries. “

“On September 12 to 14, 2006, business and government representatives from the three North American countries met in secret, with no media coverage, at the Banff Springs Hotel and convened the North American Forum. Judicial Watch, a U.S. public watchdog group got declassified government documents through a Freedom of Information Act request and made the documents available on their website. These documents reveal the discussions and membership in the secret meetings. The Canadian co-chair of the meeting was former Alberta premier Peter Lougheed, and Canadian participants included Day, D’Aquino (also a member of the NACC), all NACC corporate representatives, and John Manley.”

“The SPP is not about “security” or “prosperity” (except for the very few over the many), but is rather about forming a North American Union. When Vicente Fox recently appeared on The Daily Show, Jon Stewart asked him about NAFTA, of which Fox stated, “NAFTA’s been good. As a matter of fact we should have a new vision, go further, integrating,” and Fox went on to discuss the “solidarity” of the European Union. When asked if he wanted a North American Union, and if it would include Canada, Fox said, “Long term, yes.” On May 16, 2002 Fox spoke at Club 21 in Madrid, and stated, “Eventually, our long-range objective is to establish with the United States, but also with Canada, our other regional partner, an ensemble of connections and institutions similar to those created by the European Union.””

And now Keith Jones in WSWS.org article Canada And US Launch Continental Security Perimeter Talks documents how Canada’s Prime Minister and the United States’ President have further waived national sovereignty of their respective nations, by announcement of a Framework Agreement, at the North American Security Perimeter talks in early February 2011; and relates they have appointed two bodies of stakeholders, that is task groups, to effect their integration plans, the Beyond the Border Working Group, and the United States Canada Regulatory Cooperation Council.

Thus, clearly a region of global governance has formed in North America, where state corporatism, that is statism rules. Here sovereignty is not vested in people, or in sovereign nations, but in a regional collective governed by a President and two Premiers, and overseen by stakeholders out of government, industry, commerce, investment and banking. Global governance, in the form of global corporatism, supersedes and replaces democracy, constitutional law, as well as any and all traditional forms of the rule of law.

7) … We will see stagflation regardless of oil.

By Jeff Harding, writes in the Daily Capitalist: “We will see stagflation regardless of oil.”

“As I pointed out in “A Note on Inflation: It’s Here,” the forces of inflation are already in motion and its effects are starting to show up, one of which is price inflation.”

“Again, we need to be mindful of what is “inflation:” it is always an increase in money supply. One of the effects of inflation is price increases. Other effects, even more serious, include the destruction of real capital (that is, capital saved from production or labor, not from printing fiat money). The destruction of real capital accompanying inflation is the only explanation for stagflation.”

“The result of an oil shock will add to our economic woes, compounding the recessionary side of stagflation.”

“There has been a lot of buzz about stagflation in the mainstream media lately. Most economists pooh-pooh the idea. The reason is that they don’t understand inflation, mostly confusing price increases as a cause of something bad rather than an effect of something bad.”

8) … Some have bet profitably on a rise in inflation.

I am not a wealthy individual; my limited investment wealth is in gold bullion, as I saw the investment demand for gold coming long ago. There be many who are wealthy, and some have bet that inflation will rise; they have profited from investing in inflation swaps such as 2-year inflation swaps, and 5-year inflation swaps.

Shamim Adam of Bloomberg report: “Accelerating inflation from Singapore to Vietnam is set to spur higher interest rates and currency gains in Asian economies. Singapore’s inflation rate rose to a two-year high of 5.5% in January, while prices in Malaysia climbed at the fastest pace since mid-2009 … Vietnam’s consumer prices gained the most in 24 months in February.”

The bond vigilantes seized control of the interest rate on the 30 Year US Government Bond, $TYX, in September 2010, and the rate on the 10 Year US Government Note, $TNX, deleveraging investors out of the 30 year US Government Bond, EDV, and the US Government Note, TLT as Ben Bernanke’s QE 2 constitutes monetization of debt which resulted in the debasement of the US Dollar, $USD which fell from 83 to 81. And then in early January 2011, the currency traders enlarged their global currency war against the world central banks, of competitive currency devaluations, that is competitive currency devaluations, by calling emerging currencies, CEW, lower, which in turn created inflation destruction and debt deflation in the emerging market stocks, EEM.

9) … The credit crunch continues in Europe

Keith Jenkins of Bloomberg writes: “The European Central Bank’s efforts to stop banks running short of cash are distorting money-market rates as traders try to anticipate when that flow of emergency liquidity might start to dry up. The region’s smaller lenders, ostracized in the interbank market, are reliant on the ECB’s open market operations for funds. Bigger financial institutions, meantime, are parking excess funds back with the … central bank.”

10) ….. At market tops exuberant buyers go all in on margin.

Pragmatic Capitalism reports Buyers lever up on margin as short sellers disappear

11) … Doug Noland writes of (Increasingly Unwieldy) Monetary Disorder.

Doug Noland of Prudent Bear writes of (Increasingly Unwieldy) Monetary Disorder: The Federal Reserve’s balance sheet has expanded almost $225bn over the past 16 weeks. International (global central bank) “reserve assets” have jumped $1.5 TN in 12 months. In just two years, “reserve assets” have ballooned an incredible $2.6 TN, or about 40%, to $9.3 TN (reserves were about $3.0 TN to begin 2004). There’s been nothing comparable to this in the history of central banking – in the history of “money.” The resulting liquidity onslaught has inflated global securities and commodity prices, distorted market perceptions of risk and liquidity, depressed global yields and fomented speculative excess in any market that trades. I have referred to this backdrop as one of “Monetary Disorder.”

Monetary Disorder can certainly fester for some time under the façade of a seemingly healthy environment. As we have witnessed, global equities prices have been a prime beneficiary of global reflationary dynamics. And there is nothing like the tonic of inflating stock prices to bolster confidence and embolden the risk-takers. Ebullient markets, then, lead economic expansion and provide seeming confirmation of the bullish point of view. Yet there is no escaping the instability lurking just beneath the fragile surface.

It is said that hedge fund assets (and leverage!) have returned to pre-crisis levels. Surely, global sovereign wealth funds have grown only more gigantic. And it is worth noting that China’s “reserve assets” have jumped 46% in only two years to an incredible $2.847 TN. The world is awash in liquidity/”purchasing power” like never before. This is all worth keeping in mind as we contemplate the likelihood of ongoing unrest in the Middle East and potential supply and price shocks. The Goldman Sachs Commodities Index ended the day at the highest level since August 2008.

The global liquidity and speculation backdrop ensures that any important commodity facing potential supply constraint enjoys a propensity for spectacular price inflation – a dynamic now appreciated by companies, speculators and policymakers alike. This inflationary manifestation was really taking hold back in 2008 before the onset of the global Credit crisis. Of late, it has returned with a vengeance throughout the agriculture commodities and food complex. Yet, with stock markets booming and confidence running high, most have been content to disregard this troubling inflation dynamic. The markets this week abruptly turned somewhat less complacent (at least for a few sessions).

The Middle East crisis took a decided turn for the worst this week with the eruption of violence and chaos throughout Libya. The markets now confront great uncertainty as to how developments will unfold throughout the region. Recent events certainly increase the probability for potentially problematic energy supply disruptions and resulting price shocks. A fragile global recovery and inflated markets create a susceptible backdrop, especially with optimism and speculative zeal having become so prominent throughout global markets.

With crude (West Texas Intermediate) surpassing $100 this week – and with prospects high that Middle East instability won’t be dissipating anytime soon – analysts are scurrying to fashion views as to the impact surging energy prices will have on corporate profits, consumer spending, inflation and global growth. To say that unfolding circumstances create extreme uncertainty is no overstatement.

This week, Saudi Arabia’s King Abdullah announced plans to increase social spending by $36bn, including a 15% pay increase for government employees and $10bn for low-income housing. At the top of the list of oil exporters (and with $440bn of international reserves), Saudi Arabia enjoys unusual capacity to ameliorate its underclass. The markets are watching Saudi Arabia with keen interest, at this point confident that the kingdom has the capacity both to hold social unrest at bay and to pump additional barrels.

To be a fly on the wall in Beijing… Chinese policymakers must be intensively analyzing developments throughout the Middle East. I’ll assume they are taking great interest in the House of Saud’s approach to placating the masses. And while China is definitely no Saudi Arabia or Egypt, there is simmering social tension that provides authorities constant worry. China may not have a huge unemployed youth problem, yet inflation and Bubble Economy Dynamics have engendered huge wealth disparities and attendant social instability.

To this point, policy making has been straddling a fence. There has been a certain determination to dampen home price appreciation and other Bubble effects in urban locations, while at the same time moving to significantly increase minimum wages and boost construction of low-income housing. There has been a focus on addressing real estate excesses, with the expectation that adept economic management will allow this “tightening” to be accomplished without sacrificing ongoing strong growth. This is the type of complex economic management that nurtures a high risk of monetary mismanagement.

Today from Bloomberg News: “China may slow the pace of tightening ‘significantly’ in coming months as policy makers are likely to need time to access the impact of the ‘intensive and aggressive tightening’ measures introduced the past five months, Daiwa Securities Capital Markets Co. said… The political turmoil in some African countries and increased uncertainty about the global economy should make China ‘more cautious’ about implementing further tightening measures, according to the report by Mingchun Sun, analyst at Daiwa.”

First of all, the notion of what amounts to “intensive and aggressive tightening” has evolved considerably since Paul Volcker manned the helm of the Federal Reserve. With borrowing rates about 6% and January bank loan growth of $180bn, China remains some distance away from tight “money.” At the same time, the view that recent events might provide the impetus for Chinese authorities to take a more cautious approach to further “tightening” does resonate.

From the perspective of my analytical framework, China is in the midst of its “terminal phase” of Credit Bubble excess. I have posited that China, with the extraordinary dimensions of its population, its underdeveloped north, and the nation’s $2.8 TN hoard of reserves, has perhaps a unique capacity to prolong its historic boom. I have also noted that it is generally typical for policymakers to turn increasingly timid as the risks of bursting Bubbles compound. China has reached the point where it must move forcefully in order to rein in excess or risk things running completely out of control. I have feared that policymakers would along the way find reason to lose their nerve.

The recent surge in food and energy prices comes at a critical juncture for global policymakers. The inflationary backdrop beckons for meaningful synchronized monetary tightening. The seriousness of unfolding inflationary risks is becoming difficult to downplay. Yet the Federal Reserve, the guardian of the world’s reserve currency, won’t even slow its pace of quantitative easing, let alone reverse course and tighten. Incredibly, global inflationary dynamics do not factor into the Fed’s policy framework. The Europeans have begun to prepare the markets for an increase in rates, although when this does occur it will hardly qualify as monetary restraint. The Bank of Japan won’t be raising rates anytime soon, and I wouldn’t be surprised if other Asian central banks actually step back a bit from their baby-step approach to rate hikes.

The People’s Bank of China – “guardian” of the world’s largest population, most robust economy, most imposing Credit Bubble and most gluttonous appetite for all things food, energy and commodities – was poised to play a pivotal role in global finance; it appeared on the brink of providing a source of monetary restraint. Recent developments could change everything. Instead of potential restraint, China might adjust course and become an even greater source of global demand.

First, if China turns cautious on its tightening program, this will most likely lead to another year of stronger-than-expected economic growth (how long until China reaches 25 million annual vehicle sales?). Second, surging food and energy prices may induce the Chinese (along with others) to move more aggressively toward building “strategic stockpiles” of everything necessary to sustain strong growth and buoy social spirits. Third, the authorities may view the popularity of global protests and the Facebook phenomenon as cause to approach their objective of bolstering incomes and consumption for its enormous poor underclass even more aggressively. The potential to unleash additional purchasing power is enormous.

In a world with some semblance of normality, one would look at surging energy prices as portending restraints on growth. Global bond markets would fret at breathtaking surges in commodities prices – along with the specter of hoarding and inflation psychology becoming firmly entrenched. But these are the most abnormal of times. It is not beyond the realm of possibility that a booming Asia might actually relax and further monetize higher food and energy prices. Global bond markets – that in the past could be counted on to help dampen incipient inflation through the imposition of higher yields – remain these days fixated on the likelihood that the Fed and global central bankers will for an extended period ignore inflation and stick with ultra-loose money.

The current backdrop creates extraordinary uncertainty.

From an analytical perspective, things can go in many different directions from here.

There is no alternative than to follow developments diligently, keeping an open mind and re-evaluating often. But the makings for a serious inflation problem seem to become more cohesive by the week. Global central bankers are determined to bring new meaning to the term “behind the curve,” which connotes eventual “hard landings.” To be sure, US “CPI” these days provides an especially poor gauge of monetary conditions and the appropriateness of policy.

And when writing of an “inflation problem,” I am thinking more in terms of the global market, economic, social and political havoc fomented from an extended period of (increasingly unwieldy) Monetary Disorder.

12) The Automatic Earth reports on exporting speculative debt.

The Automatic Earth relates: The connection between the Fed, commodity price increases and social turmoil may have entered the mainstream dialogue, but it is exactly when the mainstream recognizes a financial trend that it soon reverses. Investors amassed on one side of a trade will be forced to quickly shift to the other side, and the “inflation” exported by the Fed will be revealed to be just another speculative romp crafted for the benefit of those who made out like bandits during the last one. As The Automatic Earth has repeatedly stressed, however, a deflationary price collapse will make necessary commodities even less affordable for the average person, due to a dramatic reduction in private revenues and public benefits. So while the superficial financial trend may change, the social turmoil will continue on, and next time Egypt’s revolution may not be so “peaceful.

13) A Chancellor and a Banker will arise out of crisis to provide order and a new seigniorage.

Given the extent of and unwieldy character of the current monetary disorder, gotterdammerung, an investment flameout, is inevitable. Soon out of the ensuing chaos a global Chancellor, that is a Sovereign, and a global Banker, that is a Seignior, will arise to establish a new global order, a new and universal seigniorage, with austerity for all.

14) … Keywords and symbols

The Sovereign, The Seignior, inflation destruction, monetization of debt, currency debasement, debases currency, monetizes debt, Ireland Bailout Agreement, Irish Bailout Agreement, national sovereignty, economic governance, global governance, Club of Rome, state corporatism, statism, EFSF, default mechanism, eurozone default mechanism, SPP, Security and Prosperity Partnership, Perimeter Security, Perimeter Security and Economic Competitiveness, framework agreements, inflation swaps, investment demand for gold, European Bailout, Ireland Bailout, Stagflation, Monetary Disorder, Inflation Swaps, Morgan Stanley Cyclical Index, Leverage Curve

FXE, UUP, FXC, FXA, SPY, ACWI, EEM, BND, LQD, BLV, PICB, BWX, EDV, TLT, IEI, JNK, MUB, CMF, MBB, SHY, BAB, BABS, IEF, TIP, ZROZ, MINT, GDX, GLD, KWT, SSRI, FCX, VALE, DBB, DAG, URTY, UPW, COPX, USD, EWY, EWT, ICI, SRZ, BHP, SPWRA, TSL, SOLR, LDK,

Leave a comment