Financial Market Report for March 9, 2010

1) … Failure of Neoliberalism’s seigniorage continues as stocks and commodities turned lower again. This week marks the two-year anniversary of the start of the former quantitative easing bull market; and marks the third week of failed seigniorage of the neoliberal Milton Friedman Free To Choose floating currency regime, whose moneyness is underwritten by Yen Carry Trade Investing, and US Sovereign Debt coupled with distressed securities owned by the US Federal Reserve.

Back on March 9 two years ago, investors encouraged by the seigniorage of quantitative easing, provided by the US Federal Reserve, began to go long the markets with their funds as well as with funds obtained on margin from brokerages, and with carry trade loans from Austria, Switzerland and Japan.

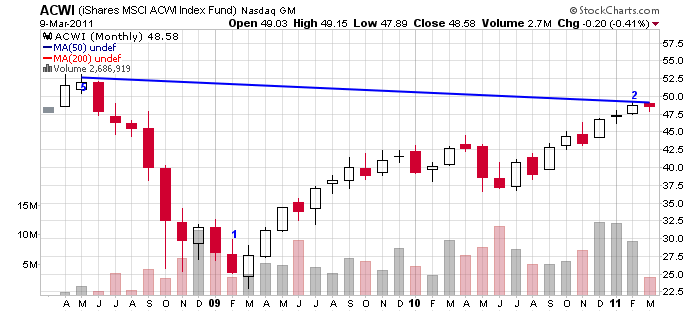

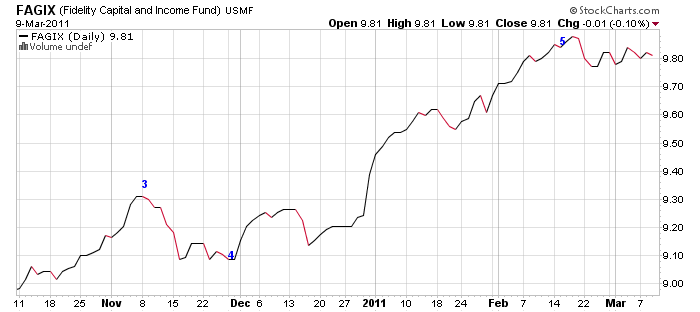

But on April 22, 2011, the seigniorage of quantitative easing failed as the value of the distressed securities owned by the US Federal Reserve, and approximated by Fidelity Mutual Fund FAGIX turned lower, which turned world stocks, ACWI, lower. It was at this time that an Elliott Wave 3 down commenced in both World Stocks, ACWI, and the S&P, SPY, as is seen in World Stocks Monthly, ACWI Monthly, and in the S&P Weekly, SPY Weekly.

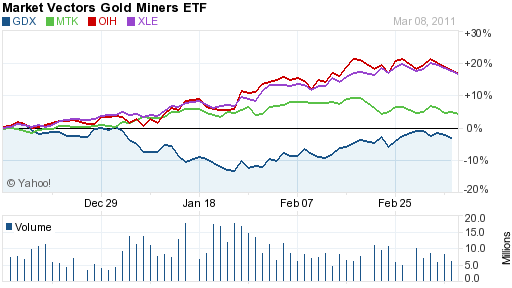

The failure of seigniorage is seen in the chart of the gold mining, GDX, stocks together with the technology, MTK, energy service, OIH, and energy, XLE, stocks … GDX MTK, OIH, XLE.

Faith in the investment seigniorage of Neoliberalism is now waining.

And Jennifer Ablan reports PIMCO Total Return has given up faith in U.S. government related debt. “The world’s biggest bond fund, has dumped all U.S. government-related securities, including Treasuries and agency debt, a source familiar with the fund’s holdings said on Wednesday. In January, Pacific Investment Management Co.’s $236.9 billion Total Return fund slashed its U.S. government related debt holdings to the lowest level in at least two years and increased cash and debt holdings from other developed nations.”

Ths basic material sector, XLB and agriculture sector, MOO, are at the forefront of quantitative easing exhaustion; the fall in these stocks is now turning base metals, DBB, and agricultural, JJU, commodity prices down.

Basic Materials, XLB, -1.6%

Copper Miners, COPX, -2.4%

US Basic Materials, IYM, -1.6%

Metal Manufacturing, XME, -2.2%

Coal, KOL, -0.9%

Steel, SLX, -1.0%

Agriculture, MOO, -1.1%

Technology stocks continue to trade lower today, establishing a failure of the seigniorage, that is the moneyness, of the Apple Ecosystem.

Faith in the financialization of Apple technology is now failing, as investor’s risk appetite has turned risk aversion, resulting in deleveraging and disinvestment out of semiconductor, networking and communication stocks.

Networking, IGN -3.8%

Semiconductor, XSD, -3.2%

Smartphone Index, FONE; -1.8%,

Small Cap Information Technology, XLKS, -1.3%

Nasdaq 1000, QTEC, -1.4%

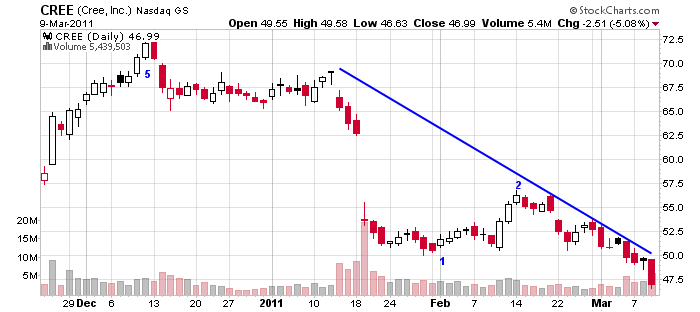

Confidence in the ability of clean energy to provide investment returns has failed. Clean Energy, QCLN, trade 1.3% lower. Investing in clean energy technology will quickly lead to one’s financial ruin, as is communicated the chart of LED Manufacturer, CREE Inc, CREE

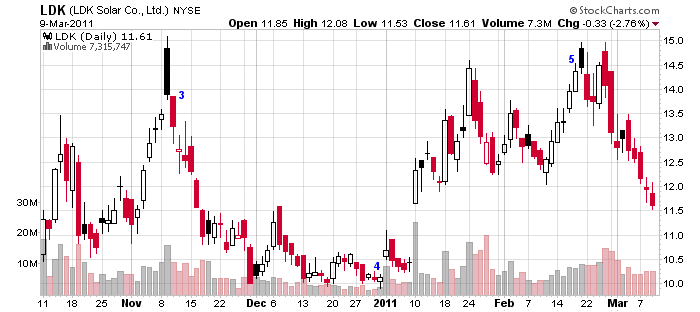

Disinvestment from solar stocks is sharp and ongoing as is seen as well as by the chart of LDK Solar, LDK.

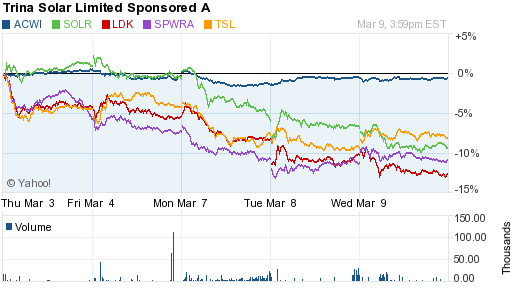

Recently, I gave strong warning about the solar stocks, KWT, GT Solar International Inc, SOLR, LDK Solar, LDK, SunPower Corp, SPWRA, Trina Solar, TSL; these have been the great fallers since the failure of seigniorage on February 22, 2011 as is seen in the chart of ACWI, SOLR, LDK, SPWRA, and TSL.

2) … The world is transitioning from the Age of Leverage, that came by quantitative easing and carry trade lending …. and into the Age of Deleveraging, which is introducing inflation destruction and debt deflation, as is seen in the fall of data storage, printed circuit board, communication, networking, semiconductor and basic material stocks today.

Data Storage Manufacturer, Sandisk, SNDK

Dram Chip Manufacturer, Micron, MU

Printed Circuit Board Manufacturers, Jabil Circuits, JBL, Diodes, DIOD, TTM Technologies, TTMI, Vishay Intertech, VSH,

Semiconductor Equipment Manufacturers, Teradyne, TER, Kulicke and Soffa Industries, KLIC,

Semiconductor Manufacturers, Lattice Semiconductor, LSCC, Atmel, ATML, Entegris, ENTG, Cypress, CY, Cirrus Logic, CRUS, NetLogic Microsystems, NETL, and Cavium Networks, CAVM,

Networking Companies, Alltera Corp, ALTR, and Juniper Networks, JNPR,

Cement Manufacturer, James Hardie Industries, JHX,

Freeport McMoRan Copper & Gold, FCX,

Silver Mining Stocks, SIL, Silver Mining Exploration Stocks, SSRI, and the gold mining stocks, GDX, were the great swing trade leading up to and into QE 2, their upward swing came on a rising US Sovereign Debt Leverage Curve, $TYX:$TNX, which is the inverse of the the 10 30 Yield Curve, $TNX:$TYX.

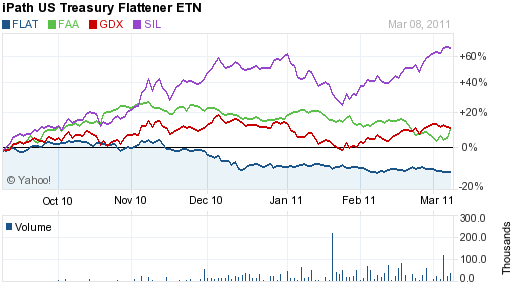

The world began to pivot from the leveraging into deleveraging when QE 2 was first announced at Jackson Hole in August. And the age of leverage became more discerned, when Ben Bernanke announced QE 2 on November 8, 2010. It was at this time that the Flattner ETF, FLAT traded lower from 52.85 reflecting a steeping yield curve, and disinvestment strongly out of US Treasuries. Formal announcement of QE 2 gave seigniorage, that is moneyness, to oil, USO. Its inflation, caused delveraging and disinvestment out of the airline stocks, FAA as is seen in the chart of FLAT, FAA, GDX and SIL.

The chart of the Morgan Stanley Cyclical Index relative to30 Year US Government Bonds, $CYC:EDV, communicates that the growth stocks have leveraged all they can on growth stocks.

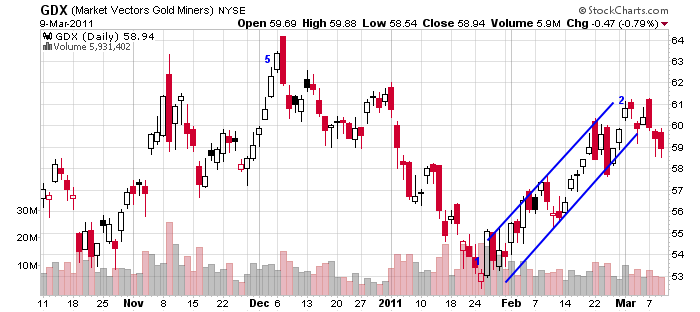

Disinvestment in gold mining stocks that came with the failure of European Leaders to resolve the sovereign crisis recommenced today. The above chart shows disinvestment came out of gold mining stocks, GDX, with the failure of the European Leaders to address the European sovereign debt crisis in mid December.

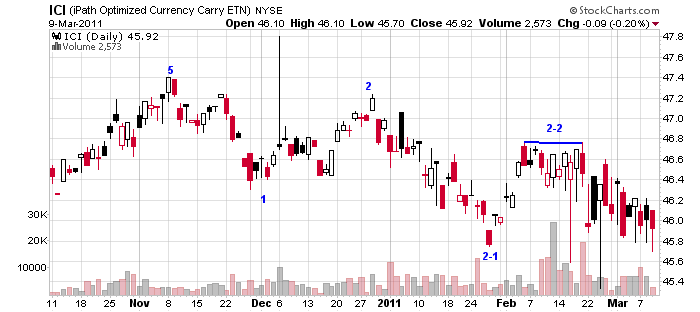

It was anticipation of sovereign debt default that has caused the rise in the gold and silver mining stocks over the years. This was the great inflation trade which came from dollar liquidity and US Central Bank and Bank of Japan credit liquidity; the chart of the Optimized Carry ETN, ICI, communicates that carry trade investing for investing long ceased with the announcement of QE 2 in November.

Now that the reality of sovereign crisis is growing more stark, the precious metal mining stocks, GDX, are leading the way lower into the Age of Deleveraging as investors take profits and “sell the swing”

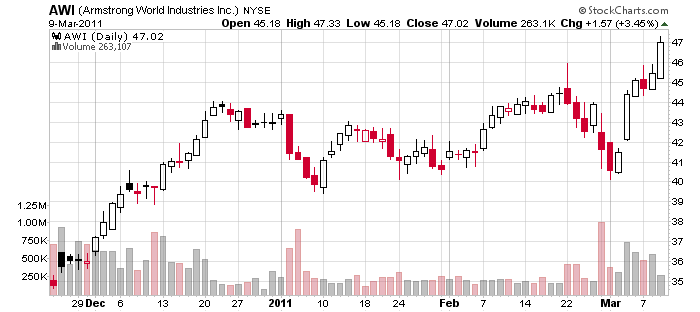

Some stocks are just now completing their cycle; such include Armstrong World Industries, AWI,

3) … The twin spigots of liquidity, these being quantitative easing and carry trade lending have run dry and are now turning toxic, as inflation destruction and currency deflation, are taking their toll … A Dollar Liquidity Crisis is on the way

Urban Dictionary defines inflation destruction as the fall in investment value that accompanies derisking and deleveraging out of investments that were formerly inflated by money flows to, and carry trade investing in, high interest paying financial institutions, profitable natural resource companies, and high growth companies.

The paradigm, construct and matrix of Neoliberalism and its seigniorage having failed, is seen in the value of distressed securities, like those in Fidelity Mutual Fund FAGIX.

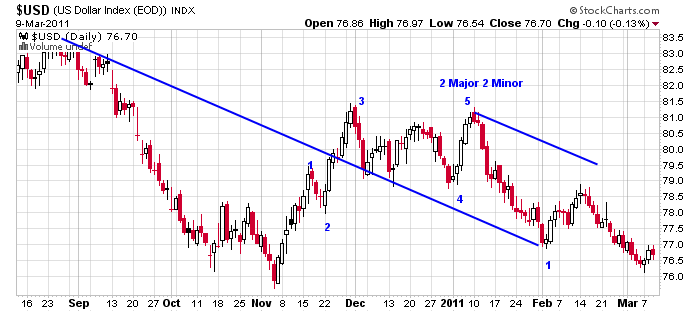

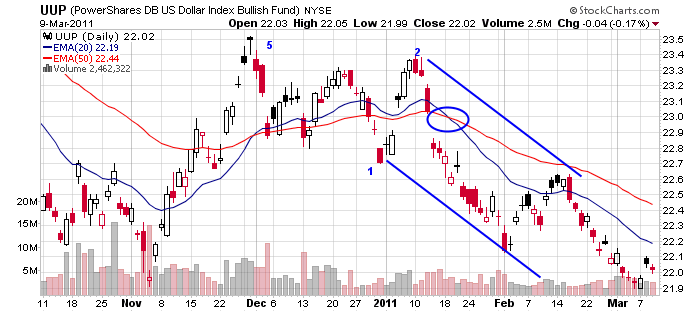

This failure of seigniorage commenced a dollar liquidity crisis on March 8, 2011, as is seen in the US Dollar, $USD, and its 200% ETF, UUP, rising in value. A rising dollar evidences the termination of the seigniorage of Neoliberalism

The dollar denominated global economic construct is coming to an end.

The chart of the $USD, shows the dollar depreciating effect of QE 2, as investors went massively short, knowing that Ben’s printing of dollars, not only destroys the value of sovereign debt, but debases the currency as well. The US Dollar was sacrificed so that assumedly, a deflationary collapse could be prevented. A deflationary collapse could not be avoided, it could only be held in abeyance. The deflationary collapse will now be coming as a dollar liquidity crisis, as assets and currencies, are sold to cover a shortage of dollars.

4) … Seigniorage is based on credit ….. seigniorage is based on trust and that is fleeting.

Two years ago, investors placed their trust in Ben Bernanke, and in his monetary policy of quantitative easing, which was based upon trading out money good US Treasuries for the distressed securities owned by banks world wide. Mr. Bernanke became banker of the world, as he took in toxic debt from global corporations, such as GE, European Financial Institutions, EUFN, and Emerging Market Financial Institutions, EMFN, These placed their US Treasuries back with the Fed in Excess Reserves.

And the global inflation trade, that is a dollar liquidity trade, invigorated investment world wide.

Then came the announcement of QE 2, and with it, and there was an explosion in the Russell 2000 Growth shares, IWO, as well as the Small Cap Energy Shares, XLES.

Apple’s Steve Jobs created the Apple ecosystem which gave seigniorage, that is moneyness to networking, communication and semiconductor stocks as well as the Asian Tigers, Taiwan, EWT, and South Korea, EWY.

Now inflation destruction and quantitative easing exhaustion is causing investment distrust; and there is a disinvestment out of the inflation trade, with investors now taking profit on their short positions in the US Dollar, causing the Dollar to rise.

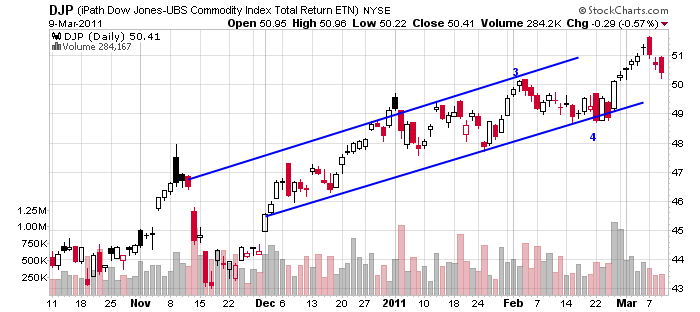

The credit value of distressed securities like those in distressed investments mutual fund, FAGIX, as well as junk bonds, JNK, are falling in value. Lacking trust in credit, investments both in stocks, ACWI, and commodities, DJP, are falling value. Base Metal Commodities, DBB, are turning lower on falling Aluminum, JJU, Copper, JJC, Nickel, JJN, and Tin, JJT, prices. Other commodities are turning lower as well; these include Agriculture, JJA, Grains, JJU, Corn, CORN and Food, FUD.

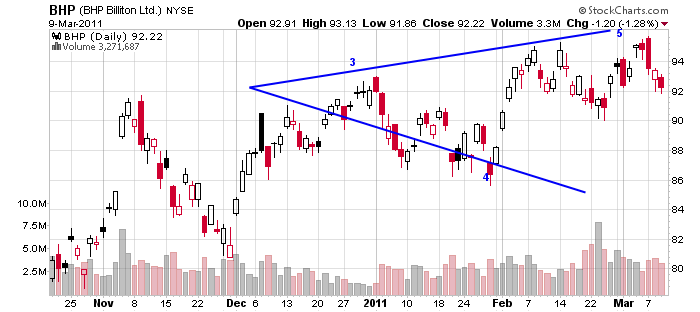

Falling base metal prices and falling metal manufacturing stock prices such as those seen in BHP Billiton, BHP, will give rise to the FX currency traders to start competitive currency devaluations, in commodity currencies, CCX, such as the Australian Dollar, FXA.

Debt deflation, that is currency deflation is coming to stocks as well as currencies. As emerging market currencies, CEW, turn down, look for emerging market bonds, EMB, to turn lower as well.

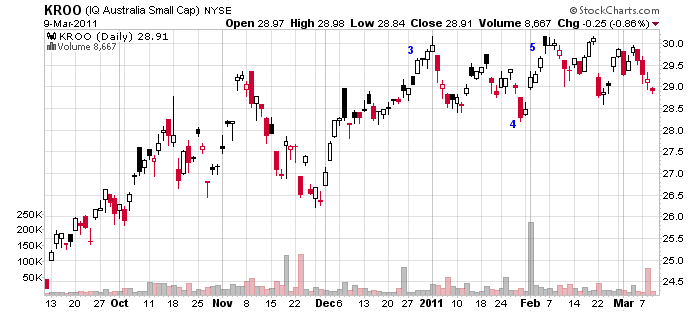

Inflation destruction caused a 1% disinvestment out of the Australian Small Caps, KROO, today.

The Currency Leverage Curve RZV:RZG, rose today, as the value of the small cap pure value shares rose more than the small cap pure growth shares on strengthening currencies such as the Mexico Peso, FXM, the Canadian Dollar, FXC, the Swedish Krona, FXS, and the Swiss Franc, FXF, and the South African Rand, SZR. I expect soon that the Currency Leverage Curve will fall, taking small cap revenue, RWJ, shares lower and the world’s major currencies, DBV, and the emerging market currencies, CEW, lower. Look for stocks like Dollar Financial, DLLR, to quickly fall lower. The credit dependent Russell 2000 companies, IWM, will fall like leaves in a fall wind storm.

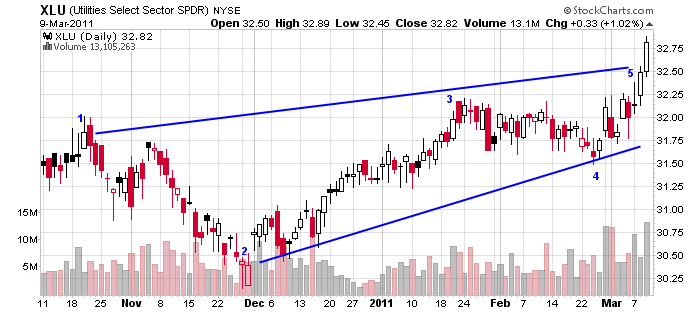

Utilities, XLU, rose to a new high today.

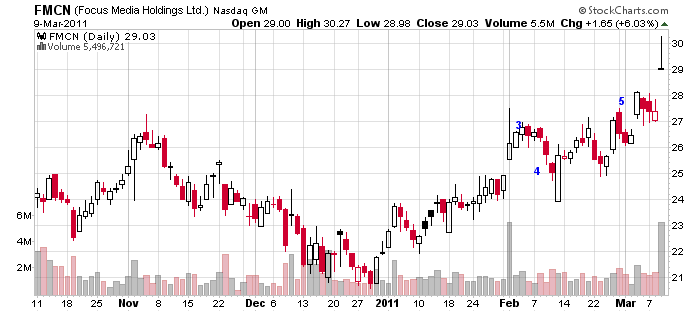

Chinese Small Caps company Focus Media Holding, FMCN, manifested a shooting star.

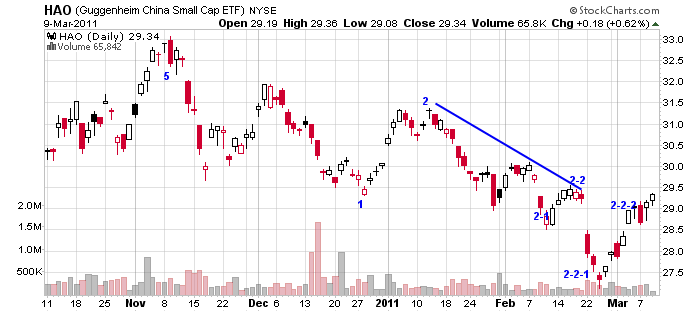

The rally in the Chinese Small Caps, HAO, appears to be ending.

5) … EuroIntelligence reports the European sovereign debt crisis is back as trust in debtors to pay and Leaders to resolve a debt and banking crisis is decreasing.

The Eurozone sovereign debt crisis is back

Greek 10-year yield reached a eurozone record, of 12.9%, as the markets are now overwhelming expecting a debt restructuring, following Moody’s three notch downgrade. Greece yesterday managed to raise €1.6bn in six month Treasury Bills at a yield of 4.75%, up from 4.64% in February. The proportion of foreign investors was one third, which is a lower proportion than last time.

After Moody’s, S&P is also pondering further downgrades for Greece and peripheral countries. Moritz Kraemer, head of sovereign credit ratings for Europe at S&P’s, told Reuters Insider Television (see full Reuters interview) that the outcome of the March 24/25 European Council in respect of the operating rules of the ESM will be critical in the futher ratings process. “We have two main concerns. The first is the preferred creditor status of the ESM … and second is the conditionality the ESM can impose to restructure debt. If both materialise, S&P would consider downgrading Greece. The same goes for Portugal,” Kraemer said.

(It is worth watching that interview in full. According to what we know, the senior status of the ESM is a done deal aimed at underlying Berlin’s wish for an investor bail-in. Senior status is very likely to have the effect Kraemer mentioned. Existing bondholders will automatically become junior in this case.)

The FT reports that the debt agency PDMA quadrupled the size of this month’s six-month bond issue to help meet a jump in debt repayments this month. Greece is set to pay back a total of €12bn of debt that matures during March. Wall Street Journal reports that the Greek government plans to sell up to $3 billion of so-called diaspora bonds to U.S. retail investors.

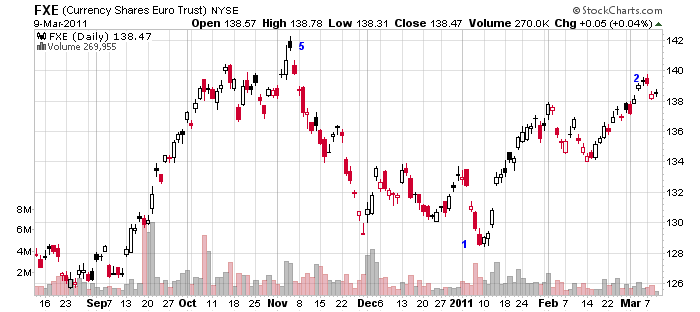

Note also that the euro fell back by a cent to under $1.3891, as a result of these latest market jitters. The forex markets are clearly torn between the eurozone crisis – which exerts downward pressure on the currency – and the transatlantic monetary policy gap, which exerts upward pressure.

Stress tests a joke

The FT leads today with a story that the stress tests are considered a “joke” among analysts, who say that some of the criteria have actually weakened since he last stress tests, such as the fall in equity prices in a negative scenario, while most of the other criteria were left unchanged. The paper quotes a senior bank analyst as saying: “There is nothing in what has emerged to change the market’s views about this process. It was a joke last time. Why is it not going to be a fudge this time?” The only criterion that is toughen is the inclusion of a 1.25pp increase in funding costs. The stress tests will this time not be a simple pass-fail mechanism, and there will be a requirement on banks to increase their capital if the fail, or narrowly pass.

Weber said he agreed with 1.75% year-end rates assessment

This is clearly now coming from an outsider. Axel Weber missed the last ECB’s council meeting because he was busy negotiating the terms for his next job. Yesterday, according to Frankfurter Allgemeine, he said that he would not disagree with market assessments of a 1.75% year end interest rate (though we should be careful about this statement. The ECB has not decided on a rate trajectory. 1.75% as plausible as 2%, or 1.5%, and which way it turns out will depend greatly on future developments.) He also predicted an increase in German economic growth to 2.5%, and announced that he would spend a year at the University of Chicago, before going back to Cologne. (so this looks like a continuation of his academic career after all, rather than a move to Deutsche Bank.) And he also announced that there will be no surprises in the stress tests (that does not surprise us one bit. Europe’s cynical regulators have fixed the tests so that this won’t happen.)

European Parliament votes to tighten short-sale rules

Last night, the economic affairs committee of the European Parliament voted to tighten short sale rules, and went significantly above the Commission’s proposal. The parliament has reduced the number of days for delivery in a naked short sale from four to one (end of day), according to Frankfurter Allgemeine. A naked short sale is one where the short seller is not borrowing the security prior to selling, but borrowing after the sale. The parliament is also banning naked credit default swaps – the purchase of credit derivates without ownership of an underlying security, or a security with a high correlation to the underlying security. The aim is to prevent pure speculation in insurance products.

Socrates effectively ties his political survival to a “No” bailout

Portuguese Prime Minister Jose Socrates insisted that if his country would turn to the IMF and the EU for a bailout rescue, it would lose its prestige and dignity as a country that can solve its own problems, Jornal de Negocios reports. “There are limits to everything, because at the moment, I believe that the responsibility of any political leader is to have confidence in the Portuguese people, confidence in his country,” he added, accusing opposition leaders of acting irresponsible and opportunistic when they say that the bailout comes sooner or later.

Wolfgang Münchau argues that Germany must either accept bailout or default, but is currently trying to prevent both

In his FTD column, Wolfgang Münchau argues that Germany cannot have it both ways: saying no to an increase in the EFSF’s remit, and saying No to government capital injections into the domestic banking sector. If Germany decides against bailout – a case which can be made – that it has prepare the grounds for a default of Greece, Portugal and Ireland, which would have significant consequences for the German banking system. Münchau argues that a disorderly default is a very risky solution. His preference would be for a process managed by the EFSF, which would include a combination of default, bailout, and reform.

Martin Wolf on why the eurozone will survive

In his FT column, Martin Wolf offers an uncharacteristically optimistic view of the future of the eurozone. The eurozone will definitely survive – even though the crisis may get worse. He offers three fundamental reasons. “First, the eurozone is backed by a profound political commitment; second, the long-term interests of participating countries are behind it; and, finally, the members can afford it. In short, the eurozone has the will and the wherewithal to keep the euro experiment afloat.” He lists three policy priorities: halt the banking crisis; help the countries in trouble regain economic health, and prevent the re-occurance of such a crisis in the future.

Bond spreads, bilateral exchange rates, and inflation expectations

Peripheral spreads continue to rise amid heightened nervousness ahead of Friday’s eurozone council meeting; euro falls sharply against the dollar; while inflation expectations jumped upwards once again

6) … Ambrose Evans Pritchard writes Political paralysis in Brussels and monetary tightening by the European Central Bank has set off a fresh spasm of the eurozone bond crisis, pushing spreads on Portuguese, Irish and Greek bonds to post-EMU records.

“The EU will do too little, too late: the markets will dictate the solution,” said Louis Gargour from LNG Capital, speaking at a Euromoney bond forum. He said Greece is already in the grip of an unstoppable debt spiral, spending 14.3pc of tax revenue on interest costs. He expects 50pc ‘haircuts’ on the debt, perhaps along the lines of the Brady Plan following Latin America’s debt crisis.

The Greek crisis is going to from bad to worse. Ten-year yields spiked to 12.78pc yesterday and unemployment jumped sharply to 14.8pc in December, a reminder that the social trauma of austerity has yet to hit.

Greece is undergoing the harshest fiscal squeeze ever tried by a modern Western economy, yet public debt will end above 150pc of GDP by 2013 even if it complies with EU-IMF terms. “We should default and return to the Drachma to punish foreign loan sharks who have bled us dry,” said Avriani, a paper linked to the ruling PASOK party.

There was similar anger in Ireland yesterday where Socialist MP Joe Higgins denounced “the poisonous cocktail of austerity concocted by the witchdoctors in Brussels and in Frankfurt”.

EU leaders have the final say on the terms of the rescue machinery, and they are answering to their own angry electorates. The eurozone remains a collection of sovereign states. That is the nub of the matter.

7) … Out of an investment collapse, a Chancellor, and a Banker, will arise to provide a new seigniorage … and the world will follow these.

One definition of money is trust, another definition of money is credit. The question is often raised, “Who are you going to trust?”

The economic and political construct of Neoliberalism will be replaced by rule of the sovereigns. And the seigniorage of Neoliberalism will be replaced by the seigniorage of the sovereigns; and that will provide security and prosperity for corporations; there will be democratic democratic deficit and austerity for all persons.

Out of a soon coming Götterdämmerung, that is an investment flameout, and a new economic and monetary paradigm, construct and matrix will arise to replace Neoliberalism. It will be characterized by Leaders announcing framework agreements, which waive national sovereignty and establish regional economic governance. A United States of Europe will soon be a reality. A Chancellor, that is a Soveign, and a Banker, that is a Sovereign, meaning top dog banker who takes a cut, will establish fiscal sovereignty, as well as a new seigniorage, and institute unified regulation of banking globally, as called for by Timothy Geithner and reported by James Politi and Gillian Tett in the Financial Times. Business leaders and government ministers will promote the interests Global Corporatism. The word, will and way of the Sovereigns will rule. The rule of the Sovereigns will replace constitutional and historic rule of law. The people of the world will follow after these — the world will put their trust in these.

There will be no jamboree Tea Party political conventions, such as the one sponsored by the Iowa Faith and Freedom Coalition, covered by Tom Bevan of Real Clear Politics, where Tim Pawlenty, the former governor of neighboring Minnesota, touted his accomplishments as a “blue” state chief executive who managed to both balance a budget and focus on faith. “We need to remember this and always remember this,” Pawlenty said. “The Constitution was designed to protect people of faith from government, not to protect government from people of faith.” And Herman Cain, the former CEO of Godfather’s Pizza, roused the crowd by proclaiming the “the United State of America will not turn into the United States of Europe. Not on our watch.”

8) … In today’s news

A) … Chris Kahn, AP Energy Writer relates Exxon CEO says oil prices not hurting economy, yet

B) … John Mauldin writes in Debt, Inflation and Global Economy Systemic Risks, The ZIRP Trap: This letter outlines the major systemic fault lines which we believe all investors should consider. Specifically, we address the following: Who Is Mixing the Kool-Aid? (Know Your Central Bankers), The Zero-Interest-Rate-Policy Trap, The Keynesian Endpoint – Where Deficit Spending and Fiscal Stimulus Break Down, Japan – What Other Macro Players Have Missed and the Coming of “X-Day”, Will Germany Go All-In, or Is the Price Too High?, An Update on Iceland and Greece.

In the end the mathematics of the debt situation in Greece are inescapable – there is more than €350bn of Greek sovereign debt and at least €200 billion of it needs to be forgiven to allow the debt to be serviceable given current yields and the growth prospects of the Greek government’s revenues. This loss has to be borne by someone – either bondholders or non-Greek taxpayers. The current policy prescription that has Greece borrowing its way out of debt is pure folly. That is the reality of a solvency crisis as opposed to the liquidity crisis that the Eurozone has assumed to be the problem since late 2008.

Until a workable plan is created that shares the burden of these losses and then formalizes a recapitalization plan, it will continue to fester and spread discord in the rest of the Eurozone. In fact, it is clear from the price and volume action in peripheral bonds that there is an effective institutional buyer strike, and it is only the money printing by the ECB that is keeping these yields from entering stratospheric levels – yet still they grind higher. Some of this move in peripheral European bond yields has been driven by broader moves higher in rates, but putting these spreads aside, it is the absolute yield levels that govern serviceability for these states and both Spain and Portugal are current financing at unsustainably high levels.

Absent a serious restructuring plan, the Eurozone will continue to reel from one mini crisis to the next hoping to put out spot fires until the banking edifice finally comes crashing down under its own weight. In our view, it will severely affect a few states considered to be in the “core” of Europe as well

C) … CNBC reports Europe debt crisis may boil to surface this week. Euro Zone leaders are seen struggling to resolve what the Germans obliquely call their “Competitiveness Pact,” investors could book profits on their Europe trades, at the very least. Traders say the Euro’s, FXE, recent strength has all been about dollar weakness and the ECB signaling higher rates next month. More than a big re-sensitization to the Euro Zone’s problems, today’s loses for the single currency seem more about profit-taking on a fantastic run. But red flags are going up elsewhere. For about a month, the cost of insuring against government default across the periphery of the Euro Zone has been rising. Similarly, the extra yield the market demands to hold Portuguese government debt over benchmark German bunds is also heading towards the 4.5 percent thumb rule point of no return.

But the “poster boy” in Europe remains Greece. Yesterday, Moody’s cut Athens’ credit rating by three notches and left it on negative watch. Today, the extra the market demands to hold Greek government debt over Bunds today rocketed past 9.6 percent and towards levels we’ve not seen since the peak of the crisis last spring.

D) … Scott Baker of the Associated Press reports from Madison WI that Democrat Tony Barca sided with Republicans to enable Republicans in the Wisconsin Senate to vote Wednesday night to strip nearly all collective bargaining rights from public workers after discovering a way to bypass the chamber’s missing Democrats.

“All 14 Senate Democrats fled to Illinois nearly three weeks ago, preventing the chamber from having enough members present to consider Gov. Scott Walker’s so-called “budget repair bill” — a proposal introduced to plug a $137 million budget shortfall. The Senate requires a quorum to take up any measures that spend money. But Republicans on Wednesday split from the legislation the proposal to curtail union rights, which spends no money, and a special conference committee of state lawmakers approved the bill a short time later. The lone Democrat present on the conference committee, Rep. Tony Barca, shouted that the surprise meeting was a violation of the state’s open meetings law but Republicans voted over his objections. The Senate then convened within minutes and passed it without discussion or debate. Spectators in the gallery screamed “You are cowards.” Before the sudden votes, Democratic Sens. Bob Jauch said if Republicans “chose to ram this bill through in this fashion, it will be to their political peril. They’re changing the rules. They will inflame a very frustrated public.”

E) … Economist Shaun Richards writes of more woes for Greece There have been increasing rumours that Greece will issue some “diaspora” bonds. These look like they will be offered in US dollars and there have been claims that they may offer as little as 4% yield. The original plan was to issue around US $3 billion of these. The concept is that they would be sold to Greek expatriates of which it is estimated that there are as many as Greece’s actual population. Now to my mind they would really have to love the motherland to allow themselves to be taken advantage of by these proposed terms! Would Sir or Madam prefer 4% to 12%?

The truth is that the Greek government has promised regularly that it will return to issuing bonds in 2011. As conventional issuance at present price and yield levels would confirm Greece’s insolvency there is a clear flaw in such a plan. However they appear not to be bothered by such (petty?) inconveniences such as reality and are trying to come up with something which looks different and presumably will fool people enough that they might buy some of it. This has happened in other countries in one form or another as for example the War Loan stock in the UK has never been repaid. However whilst War Loan turned out to be a type of misrepresentation it was not evident at the time of sale!

Greece does issue bills and issued some yesterday and it did not go particularly well. Just to clear up the difference between a bill and a bond then bills are usually of 12 months lifespan or less and bonds are of longer maturity although paper with a lifespan of between 1 and 2 years can also sometimes be called a bill. As the debt issued yesterday was of 6 months maturity then it was a bill and Greece raised some 1.62 billion Euros. There the good news ended as she had to pay 4.75% rather than the (already inflated) 4.64% she had to pay in February.

The size of the bill issue was increased because Greece has higher debt repayments to make this month and this is an ominous foreboding for her. Apart from the increasing cost of issuance she does have two inflation linked bonds and inflation is over 5% so they are proving expensive too. This is also a problem for the UK as we also have inflation-linked bonds representing more than 20% of our national debt and inflation is high here too. Greece has a much more genuine case for ruing the increase in consumption taxes such as VAT as she has had several goes at it and they will have impacted on her inflation rate.

The net result of this was that Greek ten-year government bond yields rose to close at 12.85%. At times her government bond market has got so frenzied and confused it has been hard to tell exact yields but this is about as bad as it has got and this now includes the period running up to her “rescue” although some reports had the yield over 13% briefly. If we put this another way and go back one calendar year then Greek ten-year government bond yields are 6.82% higher now than they were then.

There is a worse problem as her two-year yields are now 16.25% which is some 10.83% higher than a calendar year ago! Now the official European Central Bank interest rate is 1% and I use the difference between official rates and short-term bond yields as a yardstick. For example to illustrate the point even after last weeks rises in yield after the ECB announced it is considered an interest-rate rise German two-year bond yields 1.73%. So the gap between her and Greece is some 14.52%.

Now here comes the rub as two-years is well within the scope of the “rescue” programme. So the return of the money is in effect guaranteed by the European Central Bank the International Monetary Fund and the European Union. However at a price of 79.8 for a bond on which you should accordingly get 100 in only two years sends its own message as to the credibility of this “rescue”. This is my message to those prone to hyperbole in support of the “rescue”, how much of this bond do you hold?

Greek finances: tax revenue disappoint again

The Greek newspaper Kathimerini reported this yesterday about Greek budget revenues. Compared with the first two months of 2010, revenues declined this year by 9.2 percent he shortfall exceeding 870 million euros after the February goal was missed by 595 million.

This reinforced a point made in the downgrade issued by Moody’s (point two from my update from Monday the 7th of March) . It also reminds me of the furious sounding rebuttal of the downgrade issued by the Greek Finance Ministry.

Furthermore, Moody’s announcement refers to the delay in the rebounding of budget revenues, yet does not take into account the increase in revenues.

Whilst they are talking about 2010 they must have known their own figures for 2011…..

If you look at the Kathimerini article some things look awfully familiar to followers of the Greek crisis. The emphasis is mine for a bit I considered rather extraordinary (isn’t Greece supposed to be checking more not less?).

It appears that the revenue problems arose due to poor calculations by the Finance Ministry while drafting the budget, a reduction in checks and the go-slow tactics of some tax officers in protest at recent salary cuts.

Much of this is familiar at a time when we are supposed to believe that this is in effect the new improved Greece. As figures emerge they are contradicting the official story more and more. Looking at the detail of the figures the VAT take has in fact improved by 7.1% this year but this only means that other taxes must have fallen even further than the headline number suggests. I write this sadly but with the latest annualised economic growth figures showing a fall of 6.6% these tax revenue figures are not a surprise and I worry that things could get even worse.

Keywords: unifiedregulation, Götterdämmerung, Neoliberalism, Age of Deflation, Rule of the Sovereigns, The Sovereign, The Seignior, European Sovereign Debt Crisis, Sovereign Debt Crisis, Dollar Liquidity Crisis, Liquidity Crisis, Seigniorage, Seigniorage, Seigniorage of Quantitative Easing, Seigniorage of The Sovereigns, Rule of the Sovereigns, Apple Ecosystem, Age of Deleveraging, Inflation Destruction, Morgan Stanley Cyclical Index, Carry Trade Investing, Deflationary Collapse, Inflation Trade, Quantitative Easing Exhaustion, Currency Leverage Curve, Investment Leverage Curve, Unified Regulation of Banking Globally Global Corporatism, United State of Europe,

Leave a comment